What if you could support a cause you love and generate a steady income stream for yourself at the same time? That’s the core idea behind a Charitable Remainder Trust (CRT). This guide on charitable remainder trust explained will show you how this powerful and sophisticated strategy bridges the gap between smart financial planning and meaningful philanthropic giving.

How a CRT Actually Works

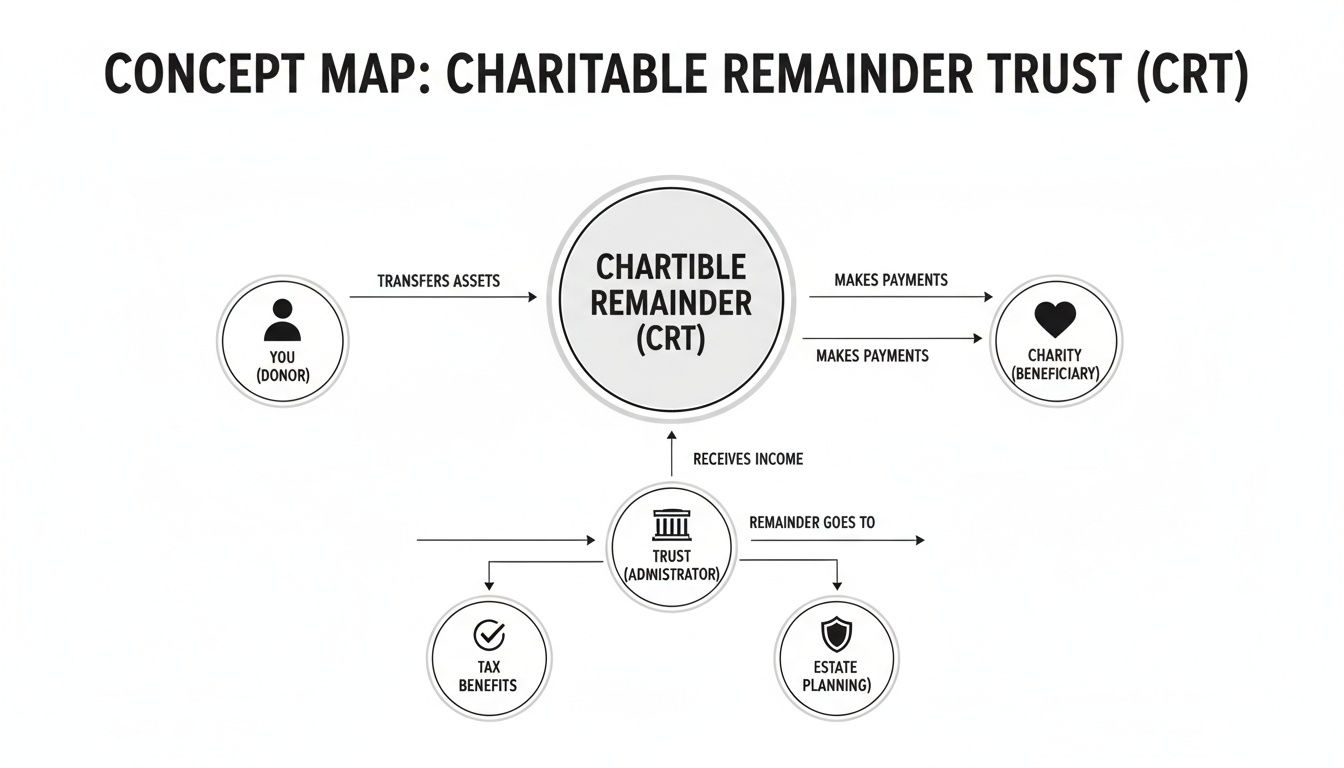

A Charitable Remainder Trust is what's known as a "split-interest" trust. It’s a special kind of legal setup that lets you provide for two very different groups: individual beneficiaries (like you or your family) and a charitable organization you care about.

Think of it as a philanthropic retirement account, but one specifically designed for assets that have shot up in value.

Here's the typical flow: You, the donor, place a highly appreciated asset—maybe stocks you've held for years, a piece of real estate, or even an interest in your business—into the trust. Once inside, the trust (which is its own legal entity) can sell that asset. The magic here is that this sale doesn't trigger an immediate, and often massive, capital gains tax bill. That's one of its biggest draws.

The trustee then takes the cash from the sale and reinvests it. From there, the trust starts making regular payments to you or other people you name as income beneficiaries. These payments can last for the rest of your life, the lives of several people, or a fixed term of up to 20 years.

The Two Sides of a CRT Coin

The structure elegantly splits the trust's value into two distinct pieces:

- The Income Interest: This is the portion that belongs to the non-charitable beneficiaries—the people receiving payments while the trust is active.

- The Remainder Interest: This is simply what’s left in the trust after all the income payments have been made. This "remainder" then goes directly to the charity you named at the beginning.

This flow chart gives a great visual of how assets move through the CRT, from you to the trust, then back to you as income, and finally to the charity.

It’s crucial to understand that a CRT is an irrevocable trust. Once you put assets into it, you can't take them back or change the fundamental rules you've set up. Grasping this level of commitment is a critical step and puts the strategy into its broader financial planning context.

Key Takeaway: A CRT lets you turn a highly appreciated asset into an income stream for yourself, get an immediate tax deduction, and leave a significant legacy for a cause you believe in—all while sidestepping a huge upfront capital gains tax hit.

Alright, once you've decided a charitable remainder trust is the right move, you hit your first major fork in the road. This decision will dictate how your income stream actually works for years, and it’s a big one. Not all CRTs are the same—they break down into two main types.

The choice between a Charitable Remainder Annuity Trust (CRAT) and a Charitable Remainder Unitrust (CRUT) is about more than just a different letter in the acronym. It fundamentally shapes your payment stability, the trust's growth potential, and whether you can add to it later on. This isn't just a technical detail; it’s about aligning the trust with your real-world financial goals.

The CRAT: Built for Predictability

Think of the Charitable Remainder Annuity Trust, or CRAT, as the embodiment of stability. It’s designed to pay you a fixed dollar amount every single year. That amount is set in stone when you create the trust, calculated as a percentage (at least 5%) of the initial value of the assets you put in.

So, let's say you fund a CRAT with $1 million and set the payout at 5%. You will get a check for exactly $50,000 every year for the life of the trust. Period. It doesn’t matter if the trust’s investments shoot for the moon or take a nosedive—your payment stays the same.

This structure is fantastic for anyone who values a reliable, steady income stream, like retirees who need to nail down their budget. But that rock-solid stability comes with one major string attached: you can never add more money to a CRAT after it's funded.

A CRAT is like a fixed pension payment. You know precisely what you'll get, which is perfect for planning, but it offers no protection against inflation and no opportunity to add more funds down the road.

That inflexibility is a dealbreaker for some. If you’re expecting another major asset down the line—say, from a business sale or an inheritance—and you want to add it to your trust, a CRAT simply won't work.

The CRUT: Designed for Flexibility and Growth

On the other side of the coin is the Charitable Remainder Unitrust (CRUT), which is all about flexibility and adapting to the future. Instead of a fixed dollar amount, a CRUT pays out a fixed percentage of the trust's value, which gets recalculated every year.

Let’s use the same numbers: you fund a 5% CRUT with $1 million. If the investments do well and the trust grows to $1.1 million by the next year, your payout for that year bumps up to $55,000.

This gives the CRUT a powerful advantage: your income can grow right alongside the trust's investments. It acts as a natural hedge against inflation, helping your payments keep their purchasing power over time. Of course, the reverse is also true. If the trust’s value dips, so will your income for that year.

Another huge difference is that you can make additional contributions to a CRUT. This is a game-changer for people who anticipate future windfalls and want to add them to the trust. It makes the CRUT a much more dynamic tool for long-term financial and philanthropic planning. It’s no surprise that CRUTs are far more common than CRATs; their structure is just better suited for navigating a changing world.

CRAT vs CRUT Key Differences at a Glance

Choosing between a CRAT and a CRUT really boils down to your personal priorities: stability or flexibility. To make it even clearer, here's a side-by-side breakdown of the key features.

Ultimately, there's no single "best" choice—only the one that's best for you. Your decision will hinge on your risk tolerance, your need for a predictable income, and whether you plan to contribute more assets in the future.

Of course, the idea of getting an income stream while supporting a cause you love is a powerful one. But let's be honest—it's the massive tax advantages that often make a charitable remainder trust a true powerhouse in high-level financial planning.

These aren't just minor tweaks to your tax bill. A CRT can fundamentally reshape your financial reality, starting the very year you set it up. Think of it as a three-pronged strategy to protect your wealth, slash your taxes, and amplify your philanthropic legacy.

The minute you fund a CRT, you get a powerful reward: an immediate, and often very large, income tax deduction. This isn't just a ballpark figure; it's a specific calculation of the present-day value of the gift your chosen charity will eventually receive.

The Immediate Charitable Deduction

This upfront deduction is easily one of the most compelling parts of a CRT. How big is it? That depends on a few moving parts:

- The Trust Term: This can be your lifetime, the lifetimes of you and other beneficiaries, or a set period of up to 20 years.

- The Payout Rate: The percentage of the trust's value you'll receive as income each year.

- The Section 7520 Rate: A key interest rate the IRS publishes monthly that’s used to value these future gifts.

It’s a bit of a balancing act. A higher payout rate or a longer term means you're getting more money over time, so the leftover "remainder" for charity is smaller. That results in a smaller deduction today. On the flip side, a lower payout or a shorter term beefs up the charity's future gift, giving you a bigger tax break right now.

This is where the real strategy comes in. Picture this: you fund a CRT with $1 million in 2025 when the Section 7520 rate is a favorable 5.4%. If you’re 60 and set up a CRAT that pays you a fixed $50,000 a year for life, the IRS calculates the value of your income stream at $609,305. The rest? That’s an immediate $390,695 charitable deduction you can use to offset your income. And if you can't use it all in one year, you can carry it forward for up to five more.

Avoiding Capital Gains on Appreciated Assets

Beyond the income tax break, a CRT offers an elegant solution to one of the biggest headaches for any successful investor: capital gains.

Imagine you're sitting on a stock portfolio you bought for $100,000 that’s now worth a cool $1 million. If you sell it, you’re looking at a hefty tax bill on that $900,000 gain—we're talking hundreds of thousands of dollars vanishing before you ever see it.

But what if you move that same stock into a CRT first? The entire game changes. Because the trust itself is a tax-exempt entity, your trustee can sell the stock for its full $1 million market value without triggering a single dollar of immediate capital gains tax.

Key Takeaway: By selling the asset inside the trust, you get to reinvest 100% of the proceeds, not just what's left after taxes. This creates a much larger engine to generate your income and, eventually, a bigger gift for charity.

This is an absolute game-changer if you have a lot of wealth tied up in one highly appreciated asset. Instead of feeling trapped by the tax hit, you can unlock the full value, diversify into a balanced portfolio, lower your risk, and create a reliable income stream all at once. For more on how giving and taxes work together, you might find our guide on the donation tax deduction helpful.

Reducing Your Taxable Estate

Finally, no explanation of a charitable remainder trust is complete without touching on estate planning. When you move assets into a CRT, they are officially and permanently removed from your taxable estate.

For families whose net worth pushes them past the federal or state estate tax exemption limits, this is huge. You're effectively shrinking the portion of your estate that will be subject to taxes when you pass away.

This move achieves two critical goals at the same time. First, it helps ensure more of your wealth goes to your heirs instead of the IRS. Second, it lets you carve out a lasting charitable legacy that truly reflects your values. It’s a powerful way to make sure your money goes to the people and causes that matter most to you.

How a CRT Works in the Real World

This is where the rubber meets the road. It’s one thing to talk about trusts in theory, but seeing them in action shows just how powerful a tool a charitable remainder trust can be. These aren't just dusty legal documents; they're creative solutions for real people navigating some of life's biggest financial crossroads.

Let's walk through a few common scenarios where a CRT can be a complete game-changer. Each story starts with a different problem but ends with a smart financial and philanthropic outcome.

The Tech Founder with Concentrated Stock

Picture a tech founder who's thinking about retirement. Most of her net worth—we're talking millions—is tied up in the company stock she’s held since the beginning. It's appreciated like crazy. She knows she needs to diversify to lower her risk and start creating an income stream, but selling the stock would trigger a staggering capital gains tax bill, wiping out a huge chunk of her life's work.

This is a classic dilemma for successful entrepreneurs. Instead of just selling and taking the tax hit, she moves the stock into a Charitable Remainder Unitrust (CRUT).

- The Problem: All her eggs are in one basket (a single, highly appreciated stock) with a massive tax liability lurking.

- The CRT Solution: The trust can then sell that stock, and here’s the key: it does so completely tax-free. This keeps the full, pre-tax value of her shares working for her, ready to be reinvested into a properly diversified portfolio.

- The Result: Suddenly, she has a diversified investment portfolio generating a significant annual income. She's sidestepped a huge tax bill, secured her retirement income, and reduced her risk overnight.

Unlocking Value from Non-Income Producing Assets

Now, think about an art collector. He owns a painting worth a fortune, but it just hangs on the wall. It’s beautiful, but it doesn't pay the bills or fund the retirement travels he dreams about. Selling it would mean a painful check to the IRS.

A CRT is the perfect tool to turn this static asset into a dynamic one. He contributes the painting to a trust, and the trustee works with an expert to sell it at its full value.

By placing the painting in a CRT, the collector essentially transforms an illiquid passion asset into a liquid, income-generating portfolio. The full proceeds from the sale are now invested to support his financial goals.

This strategy isn't just for art, either. It’s just as effective for other valuable but non-income-producing assets like raw land, a classic car collection, or other high-value collectibles. It’s a brilliant way to unlock the value trapped in your possessions.

The Real Estate Investor’s Smart Exit

Finally, let's look at a real estate investor. She bought a commercial building decades ago for a song, and now it's worth a fortune. She’s ready to hang it up and stop being a landlord, but the capital gains taxes on a straight sale are daunting.

She can accomplish all her goals by placing the property into a CRT. The trust sells the building, completely bypassing the immediate capital gains tax. This leaves a much larger pot of money to be invested for her retirement.

For instance, a high-net-worth individual might have $5 million in stock from a successful career in the sports industry. Selling it could trigger a combined federal and state capital gains tax approaching 30% of the gain. Instead, they transfer it to a CRT. The trust sells the stock tax-free, reinvests the full $5 million, and pays them a 6% annual income. That's $300,000 in steady income every year for retirement, all while teeing up a major gift for their favorite charity down the road. To see more examples of these powerful financial structures, you can explore detailed insights on Charitable Remainder Trusts.

As you can see, a CRT is so much more than a simple way to give to charity. It’s a sophisticated planning tool that can solve very real tax problems, create reliable income, and ultimately help you leave the legacy you envision.

The Step-by-Step Process to Set Up Your CRT

Putting a Charitable Remainder Trust together isn't a single event; it's a carefully sequenced process. While it definitely involves some precise legal and financial footwork, thinking of it as a clear roadmap can make the journey feel much more manageable.

Each stage builds on the last, ensuring your trust is constructed on a solid foundation that perfectly aligns with your financial and philanthropic goals. This is how a powerful concept becomes a tangible reality.

Assemble Your Professional Team

First things first: you need to get your advisory team in place. This is probably the most critical step. A CRT sits right at the intersection of law, finance, and taxes, so you need a team of experts who can see the complete picture from every angle.

This is absolutely not a DIY project. Professional guidance is essential to navigate the complexities and sidestep what could be very costly mistakes.

Your core team should include:

- An Estate Planning Attorney: This is the legal expert who will actually draft the official trust document, making sure it complies with all IRS regulations and, most importantly, reflects your exact wishes.

- A Certified Public Accountant (CPA): Your CPA is your go-to for all things tax-related. They’ll handle everything from calculating your initial charitable deduction to managing the trust's annual tax filings down the road.

- A Wealth Advisor: This is the person who helps you select the right assets to fund the trust in the first place. They’ll then manage that investment portfolio to generate the income stream you're counting on.

Define Your Goals and Key Terms

With your team in place, the next stage is all about making the core decisions that will define your trust. This is where your vision truly starts to take shape. You’ll need to clearly outline your objectives and nail down the specific terms of the trust agreement.

Key decisions you'll make at this point include:

- Choosing the Charity: Which qualified 501(c)(3) organization will ultimately receive the remainder of the trust?

- Naming Income Beneficiaries: Who will receive the income payments? This could be yourself, your spouse, your children, or another individual.

- Setting the Trust Term: Will the trust last for the lifetime of the beneficiaries, or will it be for a fixed term of up to 20 years?

- Determining the Payout Rate: You'll need to choose a percentage (it must be at least 5%) that balances your personal income needs with the goal of leaving a meaningful gift to charity.

Draft the Trust Document

Once your goals are crystal clear, your attorney gets to work translating them into a formal legal document. This is the official blueprint for your CRT, and it will spell out everything in detail—from the payout structure and the trustee's responsibilities to the identity of the final charitable beneficiary.

This document is the absolute cornerstone of your trust. It has to be drafted with incredible precision to ensure it qualifies for all the intended tax benefits and functions exactly as you envision for years, or even decades, to come.

A well-drafted trust agreement is your ultimate instruction manual. It provides total legal clarity and ensures every single party—from the trustee to the charity—understands their role and your intentions perfectly.

Fund the Trust and Appoint a Trustee

After the document is signed and notarized, it's time to bring the trust to life by officially funding it. This involves formally transferring the assets you’ve chosen into the trust's name. The mechanics will depend on the asset—it could mean retitling real estate, changing the ownership of a stock portfolio, or legally assigning other property.

Finally, you need to appoint a trustee to manage the whole thing. This could be an institution like a bank or trust company, a trusted friend or family member, or even yourself. The trustee is legally on the hook for administering the trust, managing its investments, and making sure distributions happen according to the terms you’ve laid out.

While we're focused on CRTs here, you can find great resources on the general process, like this guide on how to set up a trust in Texas, to get a broader perspective.

The Fine Print: Risks and Key Considerations

While a charitable remainder trust can be a fantastic tool for both your financial and philanthropic goals, it’s not a decision to take lightly. This is a serious, long-term commitment, and it's essential to go in with your eyes wide open to the commitments and potential downsides.

The single most important thing to wrap your head around is that a CRT is irrevocable. Once you sign the papers and transfer your assets into the trust, that’s it. There’s no undo button. You can't reclaim the assets, tweak the trust's core rules, or change your mind if life throws you a curveball. You are permanently trading direct control over that principal for the income stream and the tax perks.

The Financial Realities

Beyond the permanence, there are real-world financial risks and costs to think about. At its core, a CRT's success rides on how well its investments perform. The trust’s portfolio has to work hard enough to generate your income payments for the entire term—which could easily be decades—while still keeping the principal intact for the charity at the end. A prolonged bear market could seriously challenge those goals.

And this isn’t a “set it and forget it” strategy. A CRT comes with its own administrative baggage and ongoing expenses.

- Setup and Legal Fees: You’ll need a specialized estate planning attorney to draft the trust document correctly, and that comes with upfront legal costs.

- Accounting and Tax Filings: The trust is its own entity and has to file an annual tax return, which means bringing a CPA into the mix.

- Trustee Fees: Whether you name a bank or a trusted individual to manage the trust, they are entitled to get paid for their work.

You have to honestly weigh these cumulative costs against the tax savings and income you expect to receive. For some people, the complexity and recurring fees just don't add up, pushing them toward simpler ways to give.

Looking at Simpler Alternatives

If a CRT starts to feel a bit too complicated, it’s good to know you have other options. For many people, a Donor-Advised Fund (DAF) is a much more straightforward path for charitable giving. With a DAF, you contribute cash or assets, get your tax deduction immediately, and then you can recommend grants to your favorite charities whenever you like.

Now, a DAF won't send an income check back to you, but it’s far simpler and cheaper to manage. To get a better sense of how these different tools stack up, you can explore the key differences between a donor-advised fund vs a private foundation and see where a CRT fits into the broader giving landscape. The right choice always comes down to your personal financial picture, your need for income, and what you hope to achieve with your philanthropy.

Your Top Questions About CRTs, Answered

As we wrap up, let's tackle some of the most common questions people have when they start seriously considering a charitable remainder trust. Think of this as the practical, "how does this actually work?" part of the conversation.

Can I Change the Charity I’ve Named in My CRT?

Yes, you almost always can. Even though the trust itself is irrevocable once it's set up, you typically hold onto the power to change which charity ultimately receives the funds.

This flexibility is a huge plus. It means your philanthropic vision can evolve over the years. If a new cause captures your heart or you want to support a different organization down the road, you can make that switch without disrupting the income stream you've arranged for your beneficiaries.

How Is the Income I Get From a CRT Taxed?

This is a great question, and the answer isn't as simple as "it's taxed like regular income." The IRS has a specific four-tier system that dictates how your payments are taxed, and it all depends on what kind of earnings the trust has generated.

Think of it like a set of buckets that have to be emptied in order:

- Ordinary Income: First, any distributions are considered ordinary income and taxed at your personal rate.

- Capital Gains: Once that bucket is empty, payments are then classified as capital gains.

- Tax-Exempt Income: Next up is any tax-free income the trust might have earned, like from municipal bonds.

- Return of Principal: Finally, if all the earnings have been paid out, you start receiving your original contribution back, which is tax-free.

What’s the Minimum Amount Needed to Set Up a CRT?

Legally, there's no set minimum. But practically speaking, you need to think about the costs involved. Because you'll have legal, accounting, and administrative fees, most advisors will tell you that a CRT starts to make sense with a contribution of $250,000 to $500,000.

If you go much lower than that, you risk the setup and annual upkeep costs eating away at the tax and income benefits you were hoping to achieve. You want to make sure the strategy is truly cost-effective.

A Charitable Remainder Trust is a sophisticated financial tool. It’s critical that the initial contribution is large enough to make the administrative overhead worthwhile for the strategy to be a long-term success.

Can My Kids Get Income from the CRT?

Absolutely. You can design the trust to pay an income to your children or other loved ones. They can be the only income beneficiaries, or they can receive payments right alongside you.

This is what makes a CRT such a fantastic tool for multi-generational planning. You can set up an income stream that lasts for their entire lives or for a fixed period of up to 20 years. It's a powerful way to provide them with reliable financial support while still creating the charitable legacy you envision.

Navigating the world of wealth management and high-impact philanthropy takes a skilled guide. The team at Commons Capital specializes in creating personalized financial strategies for high-net-worth individuals and families, helping you hit both your personal financial goals and your charitable objectives. If you're ready to see how a charitable remainder trust could fit into your bigger picture, visit us at https://www.commonsllc.com.