For high-net-worth individuals, the decision to convert a 401(k) to a Roth IRA is a powerful move, shaping tax diversification and legacy planning for years to come. It’s a strategy that creates a hugely valuable source of tax-free growth and, crucially, tax-free withdrawals in retirement. This guide on converting your 401k to a Roth IRA explains how you can seize control of your financial future.

Why High Earners Convert a 401k to a Roth IRA

For affluent investors, business owners, and families with substantial assets, converting a traditional 401(k) to a Roth IRA isn't just a transaction—it's a forward-thinking wealth management strategy.

The core idea is simple yet profound: pay taxes on your retirement savings now, at today's known rates. In exchange, you create a pool of money that can grow and be withdrawn completely tax-free down the road. This single move can reshape a retirement and estate plan.

The main appeal is locking in current tax rates to shield your wealth from potential future tax hikes. By converting, you effectively remove the nagging uncertainty of what tax brackets will look like 10, 20, or even 30 years from now.

Gain Tax-Free Growth and Withdrawals

The single most significant benefit is the promise of tax-free qualified distributions in retirement. It’s the holy grail of financial planning. Once the funds are inside a Roth IRA and the rules are met, every dollar—both the original converted amount and all its future earnings—can be withdrawn without owing a dime in federal income tax.

This provides incredible financial certainty. For an entertainer with fluctuating income or a business owner planning their exit, knowing a substantial portion of their nest egg is immune to future tax bills is invaluable. It transforms retirement planning from a game of tax guesswork into a much more predictable and controlled process.

Eliminate Required Minimum Distributions

Traditional 401(k)s and IRAs come with a catch: Required Minimum Distributions (RMDs). Once you hit your 70s, the IRS forces you to start withdrawing a certain percentage of your account balance each year, and you have to pay income tax on those withdrawals whether you need the money or not.

Roth IRAs, however, have no RMDs for the original account owner. This is a massive advantage for high-net-worth individuals who may not need to draw down their retirement funds for living expenses. Your money can continue to grow, tax-free, for your entire lifetime. This flexibility also makes the Roth IRA an exceptional tool for legacy planning, allowing a larger, tax-advantaged asset to pass on to your heirs.

For wealthy investors, skipping RMDs isn't just a convenience—it's a strategic move. It prevents forced, and potentially ill-timed, taxable withdrawals that could push you into a higher tax bracket and increase Medicare premiums.

Hedge Against Future Tax Rate Increases

Many financial professionals believe that tax rates are more likely to go up than down in the future to address national debt and spending. A Roth conversion acts as a powerful hedge against this risk. You are essentially prepaying the tax on your retirement funds based on today's legislative environment.

For instance, analysis from Fidelity highlights how even a minor increase in future tax rates can give Roth accounts a distinct advantage. Their models show that if future tax rates rise from 22% to 24%, a Roth portfolio pulls ahead of a traditional one. When you scale this concept to multi-million-dollar portfolios, the financial gap created by rising taxes can become exponentially larger over time. That makes a Roth conversion a compelling defensive maneuver.

To really see the difference, it helps to put the two account types side-by-side.

Traditional 401k vs Roth IRA At a Glance

Here’s a quick comparison to break down the core features of each account. Understanding these distinctions is the first step in deciding if a conversion makes sense for your financial picture.

Ultimately, the choice hinges on your financial outlook. If you anticipate being in a similar or higher tax bracket in retirement—a common scenario for successful investors—pre-paying the taxes now through a Roth conversion can be a very smart play.

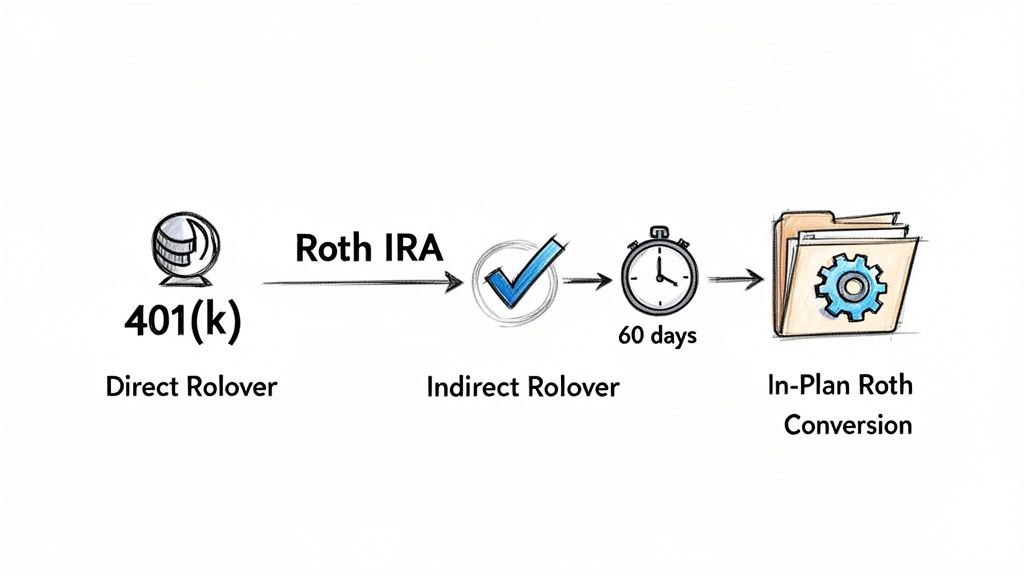

Choosing Your Roth Conversion Method

Okay, so you've decided a Roth conversion makes sense. That's the first big hurdle. Now comes the practical part: how do you actually get the money from your 401(k) into a Roth IRA?

This isn't a one-size-fits-all situation. The path you choose impacts everything from the paperwork involved to potential tax headaches. Let's break down the main ways to get this done so you can pick the right one for you.

The Direct Rollover

This is the cleanest, simplest, and frankly, the method we recommend for almost everyone. With a direct rollover, your 401(k) administrator sends the money straight to your new Roth IRA custodian. You never touch it.

The beauty of this is its simplicity. Because the funds are transferred directly between institutions, there's no mandatory 20% federal tax withholding. The full balance moves over in one clean transaction, dramatically cutting the risk of costly mistakes.

Real-World Example: A Founder's Exit

I worked with a tech founder who had just sold her company. She was sitting on a significant 401(k) from her employee days and wanted to convert it in a year when her other income was relatively low. The direct rollover was a no-brainer. We coordinated the transfer, and her multi-million dollar balance moved electronically from the 401(k) provider to her new Roth IRA. No checks, no withholding, no drama.

The Indirect Rollover

The indirect rollover is the hands-on approach, and with that comes more risk. Here, your 401(k) provider cuts you a check for your balance, but not before withholding a mandatory 20% for federal taxes.

The clock then starts ticking. You have exactly 60 days to deposit the entire original amount into a Roth IRA. That means you have to come up with that withheld 20% from your own pocket to make the deposit whole. If you miss that 60-day deadline or fail to deposit the full amount, the missing portion is treated as a taxable distribution and could get hit with a 10% early withdrawal penalty.

The 60-day rule is ironclad. We’ve seen people miss the deadline by a single day, triggering major tax bills and penalties. It’s an unnecessary risk, which is why high-net-worth clients almost exclusively use the direct rollover method.

The In-Plan Roth Conversion

Some 401(k) plans have a feature that lets you do an in-plan Roth conversion. This is exactly what it sounds like: you convert your pre-tax 401(k) dollars to Roth dollars without ever leaving your current 401(k) plan.

This is a fantastic option if you're happy with your 401(k)'s investment lineup and want to keep all your retirement funds in one place. The tax hit is the same—the converted amount is added to your income for the year—but the logistics are simpler. The catch? Not all employers offer this, so you’ll have to check your plan documents or ask your administrator.

Real-World Example: A Pro Athlete's Bonus

A client of ours, a professional athlete, received a massive signing bonus one year, which shot him into the highest tax bracket. His 401(k) plan allowed for in-plan conversions. We decided to convert a chunk of his pre-tax balance to Roth within the plan. This strategy let him strategically "fill up" that top tax bracket, paying taxes while his income was at a peak. He got a head start on a big bucket of tax-free money for retirement, all without having to open a new account.

While these are the main routes, high-income earners often explore a related strategy called the "Backdoor Roth IRA." It's a different animal, and you can learn more about it in our guide on the backdoor Roth IRA conversion. Ultimately, the best method really depends on your specific financial picture and what your 401(k) plan allows.

Wrapping Your Head Around the Conversion Tax Hit

Let's be blunt: the decision to convert a 401k to a Roth IRA almost always comes down to the tax bill. It’s the biggest mental hurdle for most people, but it’s far from insurmountable. With some smart planning, you can manage the upfront cost and set yourself up for a powerful, tax-free retirement.

The mechanics are pretty simple. Any money you move from a pre-tax 401(k) gets added directly to your taxable income for the year you do the conversion. It’s treated just like your salary, which means it can temporarily bump you into a higher tax bracket.

For instance, say your taxable income is typically $200,000. If you convert $150,000, your taxable income for that one year jumps to $350,000. The trick is to be strategic about that income spike to keep the tax hit as low as possible.

Getting Strategic With Your Tax Liability

Timing is everything. This is your single best tool for controlling the tax impact of a conversion. Instead of pulling the trigger on a massive conversion during a peak earning year, you can be more deliberate.

Look for a window of opportunity when your income is naturally lower. Maybe it’s a year between big contracts, a planned sabbatical, or that sweet spot right after you retire but before you start taking Social Security. Executing the conversion when you're in a lower tax bracket can save you a bundle. When you're figuring out the tax impact, it's crucial to know how this will all look on your tax reporting on your Form 1040.

Another fantastic approach is to break it up. You don't have to convert everything at once. By doing a series of smaller, partial conversions over several years, you can strategically "fill up" your lower tax brackets each year without ever spilling into the highest ones. It’s a great way to smooth out the tax liability over time.

A lot of people think a Roth conversion is an all-or-nothing deal. That's a myth. Partial conversions give you incredible flexibility to basically dial in your tax bill year after year.

The Pro-Rata Rule: A Common Pitfall to Avoid

Now, for one of the most common and costly mistakes I see: the pro-rata rule. This rule is a big deal if you have any existing pre-tax money in traditional, SEP, or SIMPLE IRAs.

Here's the rub: The IRS views all of your traditional IRA accounts as one giant pool. When you do a conversion, it calculates the percentage of that entire pool that's pre-tax versus after-tax (from non-deductible contributions). Your conversion is then considered a proportional mix of the two, which can trigger a much bigger tax bill than you were expecting. For a really deep dive into the nitty-gritty, you can learn more about Roth conversion tax implications in our full guide.

Let’s walk through a real-world scenario to make this crystal clear.

Scenario: A Client with Mixed IRA Funds

Imagine a client, Sarah, wants to convert a $50,000 401(k) into a Roth IRA. She's thinking she'll just owe taxes on that $50,000. Simple enough, right?

Not so fast. Sarah also has an old rollover IRA from a previous job with a $450,000 pre-tax balance sitting in it.

This is where the pro-rata rule kicks in:

- Total Pre-Tax IRA Balance:

$450,000(from her old IRA) +$50,000(from the 401k she's rolling over) =$500,000 - Total After-Tax Balance: We'll assume Sarah has

$0in after-tax contributions. - Total IRA Value:

$500,000 - Pre-Tax Percentage:

$500,000 / $500,000 = 100%

In Sarah's case, because 100% of her total IRA money is pre-tax, any amount she converts will be fully taxable. Even if she only wanted to convert a small portion, it would all be taxed. If she had, say, $50,000 in after-tax money in that pool, her pre-tax percentage would be lower, and part of her conversion would be tax-free.

Understanding this rule is absolutely non-negotiable. If you ignore your other pre-tax IRA balances, you could be in for a nasty surprise come tax time, completely wrecking the benefits of your conversion strategy. This is exactly where working with an advisor can help you navigate the complexity and avoid those costly mistakes.

Advanced Conversion Strategies for Affluent Investors

For high-net-worth investors, the decision to convert a 401k to a Roth IRA is less about if and more about how. Moving beyond a simple, one-time conversion opens up a whole playbook of advanced strategies. This is where you can get tactical to maximize tax efficiency, turning a potentially massive tax hit into a manageable, multi-year plan.

The game plan here is to strategically rip off the tax band-aid now. By paying taxes on your terms, you pave the way for decades of tax-free growth and withdrawals in the future.

Embrace Partial Conversion Sequencing

One of the most powerful tools in the kit is partial conversion sequencing. Instead of converting your entire 401(k) in one fell swoop and triggering a monster tax event, you break it up. You convert smaller chunks over several years.

This method is all about control. It lets you strategically "fill up" lower tax brackets each year without ever tipping yourself into the highest marginal rates. It’s a methodical way to manage your annual tax bill.

This approach is especially timely. Thanks to the 2017 Tax Cuts and Jobs Act (TCJA), today's tax rates—which top out at 37%—are more favorable than the pre-TCJA peak of 39.6%. Those lower rates are set to expire after 2025.

Think about it: a married couple with $180,000 in taxable income has a ton of room in the 24% bracket. They could convert an extra $100,000, stay within that bracket, and pay a predictable $24,000 in federal tax. That’s a calculated move, not a tax surprise.

Case Study: A Multi-Million Dollar Phased Conversion

Let's walk through how this looks in the real world. I worked with an entrepreneur, age 60, who had just sold his business. He was sitting on a $2 million 401(k) and had very little other income projected for the next five years before Social Security kicked in.

- Lump-Sum Conversion: If he converted the full $2 million at once, it would launch him straight into the top federal tax bracket (37%). The estimated federal tax bill? Over $700,000. Ouch.

- Sequenced Conversion: We mapped out a five-year plan instead. Each year, he converts $400,000. This keeps his taxable income within the 32% and 35% brackets, completely avoiding that top rate.

By phasing the conversion over five years, we projected he would save well over $100,000 in federal taxes compared to the all-at-once approach. He’s systematically moving his nest egg into a tax-free vehicle while dramatically cutting the cost to get there.

The power of sequencing lies in its precision. It transforms the tax bill from a blunt force into a surgical instrument, allowing you to carve out tax-free wealth year by year.

Navigating Complex State Tax Laws

Federal taxes are just one piece of the puzzle. State income taxes can completely change the math on a conversion, so they have to be a core part of your strategy.

Some states, like Florida and Texas, have no state income tax, making them ideal places to pull the trigger on a large conversion. Others, however, have high income tax rates that can add a painful layer of cost.

- Timing with a Move: If a move is in your retirement plans, timing is everything. An executive client in California (with a top rate of 13.3%) was planning to retire to Nevada (which has 0% income tax). By waiting to do his $1 million conversion until after he officially established residency in Nevada, he's in line to save over $130,000 in state taxes alone.

- State-Specific Rules: Don't assume all states treat retirement income the same. It's critical to know the specific rules in your current state and any state you're considering for retirement.

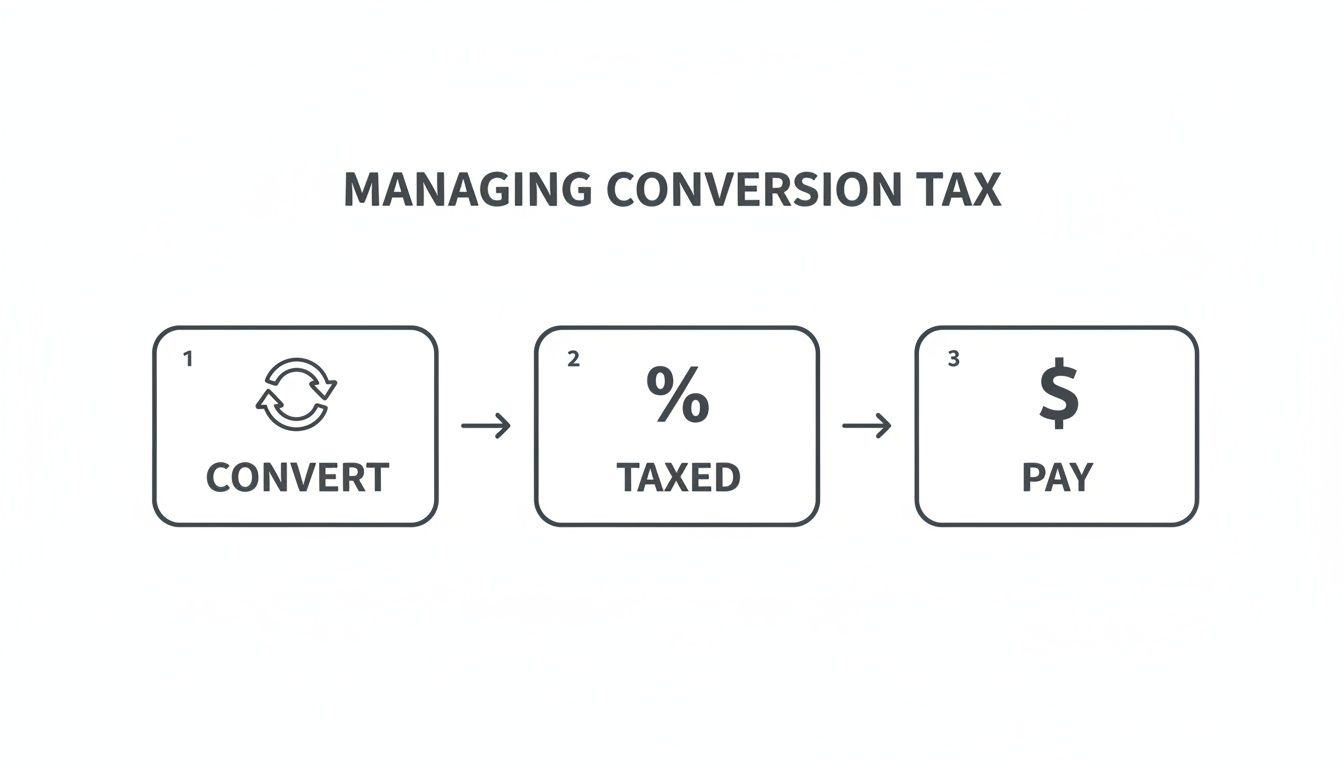

The infographic below gives you a simple visual of how the tax liability flows from a conversion.

This breaks the process down into three fundamental actions: converting the money, figuring out the tax you owe, and paying the bill. These are the core steps to managing the financial impact.

Making Estimated Tax Payments

A large Roth conversion means a big jump in your taxable income for the year. Your regular paycheck withholding almost certainly won't cover it, which puts you at risk for underpayment penalties from the IRS.

To get ahead of this, you’ll need to make estimated tax payments. These are quarterly payments you send directly to the IRS to cover the extra tax liability from your conversion.

You can calculate what you owe and pay online through the IRS Direct Pay system or by mail. A little planning here ensures you cover your obligations throughout the year, preventing a nasty surprise—and unnecessary penalties—come tax time. And while a Roth conversion is a fantastic tool, it’s always wise to explore additional tax saving strategies to round out your financial plan.

Following the Key Rules and Timelines

When you decide to convert a 401(k) to a Roth IRA, you're stepping into a process governed by a set of non-negotiable IRS regulations. Getting these details right is the difference between a savvy, tax-efficient strategy and a costly headache down the road. This isn't just about checking boxes for compliance; it's about making sure you unlock the full power of your tax-free account.

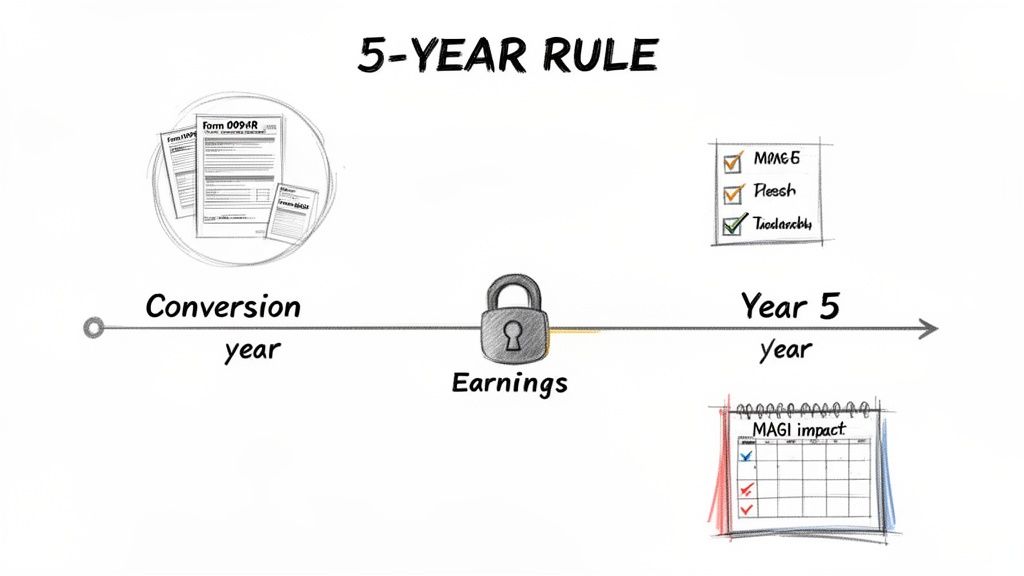

At the heart of it all is the often-misunderstood "5-Year Rule." This isn't just one rule, but actually two distinct clocks that start ticking at different times. Nailing down how they work is absolutely critical, especially if you think there's even a chance you might need to tap into these funds before retirement.

Unpacking the Two 5-Year Clocks

The first 5-year clock applies to all your Roth IRA contributions combined. Its job is to determine whether the earnings in your account are tax-free. This clock kicks off on January 1 of the very first year you contributed to any Roth IRA. Once that five-year window passes (and you're at least age 59½), all the growth your account has generated can be withdrawn completely tax-free.

Now, the second 5-year rule is specifically for conversions. Each and every time you convert funds from a traditional account, a separate five-year clock starts for that specific chunk of money. This rule is all about whether you can withdraw your converted principal before age 59½ without getting hit with a nasty 10% early withdrawal penalty.

Let’s walk through a quick scenario to make it clear.

- Imagine you're 50 years old and convert $100,000 from your old 401(k) into a new Roth IRA.

- Two years later, at age 52, an emergency pops up and you need to pull out $20,000. Because the five-year holding period for that specific conversion hasn't passed, that $20,000 withdrawal would be subject to a 10% penalty—even though it's your own money you already paid taxes on.

The key takeaway here is simple but crucial: each conversion starts its own penalty-avoidance clock. If you decide to do several partial conversions over a few years, you'll have multiple five-year clocks running at the same time.

Managing Deadlines and Documentation

Beyond the timing rules, getting the paperwork right is absolutely essential for a smooth conversion. The IRS needs specific forms to track the money's movement and make sure the right tax liability is recorded. Missing a step here can trigger notices, audits, and a lot of unnecessary stress.

First, you'll get a Form 1099-R from your 401(k) provider, which reports the distribution from the old account. It's then on you to report the conversion properly on Form 8606, "Nondeductible IRAs." This is the form that tells the IRS, "Hey, I didn't just cash this out; I moved it into a Roth."

This reported income gets added to your main tax return, which will increase your Modified Adjusted Gross Income (MAGI). Be mindful that a higher MAGI can create ripple effects, potentially bumping up your Medicare Part B and D premiums or disqualifying you from other tax deductions. This is why timing your conversion is so important. It's also vital to know how this process interacts with other retirement rules; for those approaching that age, you might find our guide on how to calculate Required Minimum Distributions (RMDs) helpful.

Your Roth Conversion Documentation Checklist

To keep everything straight, a simple checklist can be a lifesaver. It ensures you have all the necessary paperwork accounted for before, during, and after you make the move.

Think of this table as your roadmap to staying organized and ensuring every part of your conversion is handled correctly.

Common Questions About Converting a 401k to a Roth IRA

Even the best-laid plans run into practical, real-world questions. When it comes to something as significant as a 401(k) to Roth IRA conversion, those little details can make all the difference.

Let's walk through some of the most common questions we hear from high-net-worth clients who are weighing this decision.

Can I Convert My 401k to a Roth IRA If I Am Still Working?

Yes, you often can, but the final say comes down to your employer’s plan.

Many 401(k) plans include a provision for an "in-service distribution" once you hit a certain age, typically 59½. This is the green light that lets you roll funds over to an IRA while you're still on the payroll.

But not every plan is this flexible. If yours doesn't allow it, you’ll probably have to wait until you leave the company to make your move. Your first step should always be to check the Summary Plan Description or call your plan administrator to get a clear answer.

How Does a Roth Conversion Impact My Estate Plan?

A Roth conversion can be a powerful tool for transferring wealth. The biggest advantage? The original owner of a Roth IRA is not subject to Required Minimum Distributions (RMDs). This means the account can keep growing—completely tax-free—for the rest of your life.

The ripple effect for your heirs is massive. They inherit the assets and can generally withdraw them tax-free, though they'll have their own distribution rules to follow. By converting, you're essentially prepaying the tax bill, passing on a significant asset without saddling your loved ones with a huge tax liability down the road. It’s a highly efficient way to build a legacy.

Think of it this way: you're using your retirement account not just for your own future, but as a tax-advantaged gift for the next generation. You handle the taxes now so they won't have to later.

What If I Need Access to My Converted Roth IRA Funds Early?

The rules here are very specific, but they offer some wiggle room. You can always withdraw the amount you converted (your "basis" or principal) at any time, both tax-free and penalty-free. It makes sense—you already paid the taxes on that money during the conversion.

Where it gets tricky is with the earnings. This is where the 5-year rule comes into play. If you withdraw earnings before you’ve held the account for five years and you’re under age 59½, those earnings will get hit with both income tax and a 10% early withdrawal penalty.

It’s crucial to remember that each conversion you do starts its own separate 5-year clock. Meticulous record-keeping is an absolute must.

Is There an Income Limit for Converting a 401k to a Roth IRA?

No. This is one of the biggest misconceptions out there. There are absolutely no income limits when it comes to converting a traditional 401(k) or traditional IRA to a Roth IRA.

The income restrictions people often hear about only apply to making direct annual contributions to a Roth IRA. This open-door policy on conversions is precisely what makes powerful strategies like the "Backdoor Roth IRA" and other large-scale conversions possible for high-income earners, no matter how much they make.

Navigating the complexities of a Roth conversion requires careful planning and strategic foresight. At Commons Capital, we specialize in helping high-net-worth individuals and families make informed decisions to align their wealth with their long-term goals. If you're ready to explore how a Roth conversion fits into your financial picture, contact us today to start the conversation.