Creating an investment policy statement is the bedrock of any disciplined, long-term financial strategy. It’s a formal document that acts as your roadmap, laying out your investment goals, your comfort level with risk, and the specific rules that will govern your portfolio. Think of it as a pre-commitment to making rational decisions. An investment policy statement is designed specifically to keep you from reacting emotionally when the market inevitably gets choppy.

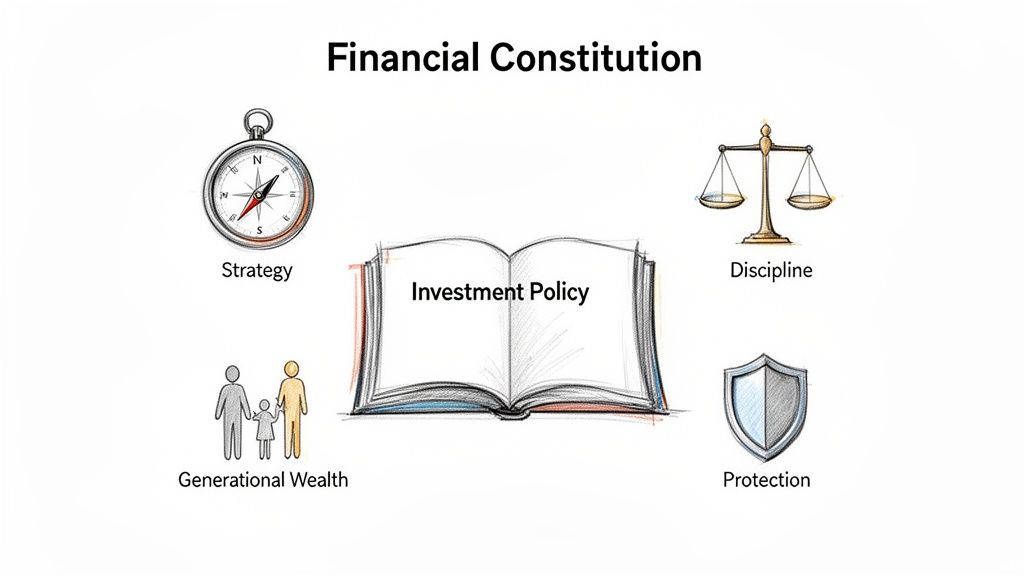

Your Financial Constitution: Why an IPS Is Non-Negotiable

For high-net-worth individuals and families, the biggest threats to preserving wealth are market noise and emotional impulses. We’ve seen it time and again. An Investment Policy Statement (IPS) acts as your financial constitution—a steadfast guide ensuring every decision aligns with your ultimate objectives, no matter what the markets are doing in the short term.

This isn’t just a formality. It’s a strategic framework that goes beyond vague goals and codifies the exact "how" and "why" behind your investment plan. By documenting everything from your time horizon to your need for cash, you create a crystal-clear understanding between you, your family, and your advisory team.

The Modern Case for a Disciplined Framework

The need for a structured approach has never been more critical. The entire investment landscape has shifted, especially after the major recessions of the last two decades reshaped how institutions think about strategy.

While the S&P 500 delivered an incredible 14.7% compounded annual return from March 2009 to July 2022, expectations are now much more grounded. Current forecasts from firms like Morgan Stanley predict a more modest 8.4% annual return for U.S. stocks over the next 20 years. That reality check alone underscores just how necessary a disciplined framework is to navigate what's ahead.

An IPS is the single most effective tool for preventing the two behaviors that destroy wealth: panic selling during downturns and chasing performance during rallies. It anchors your strategy in logic, not emotion.

An Investment Policy Statement is what lays the groundwork for successful Guided Growth strategies. It ensures your portfolio isn't just built for today's market, but for the life you envision decades from now.

Key Benefits of a Formal IPS

A well-crafted IPS brings a level of rigor and professionalism to your personal finances that’s essential for managing significant wealth.

Here’s what it really delivers:

- Enforces Discipline: It provides a clear roadmap to follow during market stress, preventing impulsive and often costly decisions.

- Enhances Communication: The IPS gets all stakeholders—family members, trustees, and financial advisors—on the same page with the same objectives and constraints.

- Creates Accountability: It sets up measurable benchmarks and clear guidelines, allowing for an objective look at your portfolio's performance and your advisor's actions.

- Provides a Long-Term Perspective: By cementing your strategic goals, the document helps you see past short-term volatility and stay focused on what truly matters.

Defining Your Investment Objectives and Constraints

Every solid investment plan starts by turning your life goals into a clear financial road map. This isn't about vague ideas like "I want to grow my wealth." It's about a much deeper conversation—what is this money really for? The answers you uncover become the specific, measurable targets that anchor your entire strategy.

Is the end game to launch a multi-generational philanthropic foundation? Or maybe it's all about structuring a seamless wealth transfer to the next generation, minimizing the tax bite along the way. For others, it might be as simple (and as important) as guaranteeing a certain quality of life in retirement, no compromises.

Each of these goals demands a completely different playbook. Without getting crystal clear on them upfront, an investment strategy is just a random collection of assets adrift without a rudder.

From Vague Goals to Specific Objectives

The best investment objectives are the ones you can actually measure. This clarity is crucial; it ensures you, your family, and your advisor are all pulling in the same direction. The trick is to ask the right questions that turn broad hopes into real financial targets.

Think about the difference here:

- Vague: "I want to leave a legacy."

- Specific: "To grow the portfolio to $15 million over the next 20 years. The goal is to fully fund a charitable remainder trust that will generate $100,000 annually for our chosen charities, forever."

Or another common one:

- Vague: "I need to get ready for retirement."

- Specific: "To generate $400,000 in annual, after-tax income from the portfolio starting in 15 years, with payouts designed to climb by 3% each year to keep up with inflation."

This isn't just a paper exercise. This level of detail dictates everything that comes next, from the returns you need to hit to how much risk you can stomach.

Understanding Your Unique Constraints

Once you know where you're going, you need to map out the terrain. That’s where constraints come in. Think of them not as limitations, but as the essential guardrails that keep your strategy grounded in the real world and aligned with your unique financial life.

For a family office, this could mean navigating complex tax structures or dealing with a massive, concentrated stock position from the family business. For someone who just retired, the biggest constraint might be an ironclad need for predictable, steady income.

Your objectives tell your portfolio where to go. Your constraints define the path it must take to get there. Ignoring constraints is one of the fastest ways to derail a well-intentioned financial plan.

Identifying Key Constraints in Your IPS

A handful of constraints always need to be addressed when you're building out an IPS. Each one adds another layer of resilience and personalization to your plan.

Time Horizon

This is simply how long your money has to work for you. A 30-year-old building a retirement nest egg has a radically different time horizon than a 65-year-old who needs to start taking distributions now. You'll likely have multiple goals, each with its own timeline—like saving for a child's college education (a 15-year horizon) versus funding that multi-generational trust we talked about (a perpetual one).

Liquidity Needs

How much cash do you need to keep accessible, and when? Maybe you're eyeing a major business acquisition in the next two years. Or perhaps you have significant estimated tax payments coming due. Your IPS has to account for these cash calls to make sure you're never forced to sell long-term assets at the worst possible time. For high-net-worth families, liquidity planning is often a cornerstone of the whole strategy.

Legal and Regulatory Factors

This is a huge one for trusts, foundations, and family offices. It covers any legal frameworks, like irrevocable trusts, that dictate how assets must be managed or paid out. It also includes any regulatory rules that might apply, ensuring your investment approach stays fully compliant.

Tax Considerations

Your tax picture is a massive constraint that can't be ignored. A high-income earner living in California or New York is playing a totally different game than someone in a more tax-friendly state. The IPS should spell out the game plan for things like tax-loss harvesting, asset location (putting tax-inefficient assets into tax-sheltered accounts), and managing capital gains to maximize what you actually keep. This is often where a sharp advisor can add tremendous value.

Translating Risk Tolerance Into Asset Allocation

Once you’ve nailed down your objectives and constraints, it's time to connect the dots between your personal risk tolerance and an actual asset allocation strategy. This is where the rubber meets the road—where your gut feelings about risk are translated into the hard numbers of portfolio construction. It’s all about striking the right balance between the growth you’re aiming for and the market volatility you can actually stomach.

Getting a handle on your true risk tolerance means looking at two different things: your financial capacity to take on risk and your psychological willingness to do so. Your capacity is objective; it's based on factors like your time horizon, immediate cash needs, and the overall stability of your finances. Your willingness, though, is purely emotional. It’s how you’d genuinely react when the market takes a significant nosedive.

A well-drafted IPS forces you to be brutally honest about both. It’s one thing to claim a high tolerance for risk when everything is going up, but a real assessment prepares you for the inevitable turbulence.

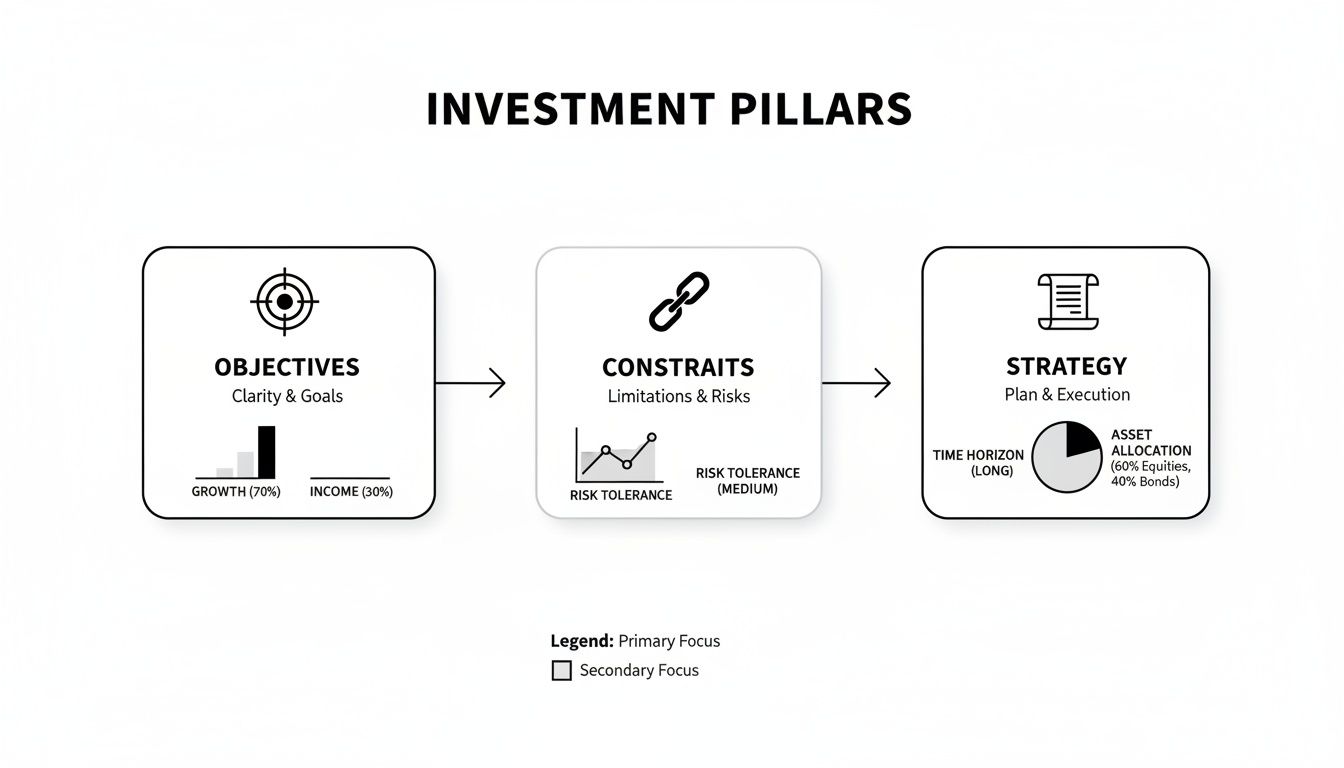

The chart below shows how your goals and limitations serve as the bedrock for your entire investment strategy.

As you can see, a winning strategy is built on a crystal-clear understanding of what you want to achieve and what your boundaries are, which then directly shapes your asset allocation.

From Risk Profile to Portfolio Mix

Here's a core principle of modern portfolio theory that you can take to the bank: asset allocation is the single biggest driver of your portfolio's long-term returns. The specific mix of stocks (equities), bonds (fixed income), and alternatives you settle on will have a much greater impact on your results than trying to pick the next hot stock or perfectly time the market.

The IPS makes this critical decision official. Instead of a fuzzy guideline, it spells out target percentages for each asset class, complete with acceptable ranges. This gives you a strategic anchor while still allowing for some tactical wiggle room.

For example, a moderate-risk profile might call for a 60% target allocation to equities. The IPS would formalize this with an allowable range, maybe 55% to 65%. This empowers your advisor to make small shifts based on market conditions without ever abandoning the core, long-term strategy you've agreed upon.

The Power of Documented Allocation Targets

Putting these targets in writing is a powerful act of discipline. At firms like Commons Capital, we know that asset allocation frameworks within an IPS are responsible for up to 90-95% of a portfolio's performance swings. In the institutional world, this gets incredibly specific. You might see large endowment plans setting targets like 4.0% to 2.5% in emerging market bonds or 23.5% to 24.0% in private equity, all benchmarked against custom indices.

An IPS transforms asset allocation from a theoretical idea into a binding commitment. It's the very mechanism that keeps your portfolio aligned with your risk profile, not the market's mood of the day.

This documented approach is absolutely essential for managing complex portfolios. For a deeper dive, check out our guide on asset allocation strategies for a volatile market.

Sample Asset Allocation Models by Risk Profile

To bring this to life, let’s look at how different risk profiles might translate into specific asset allocation models. Keep in mind, these are just illustrations; your own mix should be tailored specifically to you after a thorough discussion with your advisor.

Each of these models reflects a different trade-off between risk and potential reward.

- A conservative allocation is all about preserving capital and generating income, making it a good fit for someone with a low risk tolerance or a shorter time horizon.

- The moderate approach looks for a healthy balance of growth and stability, a common strategy for investors who have decades ahead of them.

- An aggressive model is built for maximum long-term growth and is really only appropriate for those who can handle significant risk and have plenty of time to recover from any market downturns.

Your IPS will specify which of these models—or a customized version—is the right one for you, ensuring your portfolio is built to match your unique financial DNA. That kind of clarity is the foundation of successful long-term investing.

Putting the Key Pieces of Your IPS on Paper

Once you’ve nailed down your objectives, constraints, and how much risk you’re truly comfortable with, it’s time to start drafting the actual Investment Policy Statement (IPS). This is where all those foundational conversations get translated into specific, actionable guidelines for managing your money. Think of it as framing a house—each component provides structural integrity, making sure your financial plan can hold up under pressure.

A real IPS isn't some generic template you download. It’s a detailed blueprint that brings clarity to every single part of your investment strategy, leaving zero room for guesswork when big decisions need to be made. This document becomes the go-to reference for you, your family, and your entire advisory team.

Roles and Responsibilities

One of the first things to tackle is defining who does what. This is absolutely critical. In complex family or trust situations, you'd be surprised how often overlapping duties lead to confusion, or worse, total inaction. The IPS cuts right through that by clearly assigning every key role.

This section needs to explicitly name the players and outline exactly what they’re responsible for:

- The Client (You/Your Family): Your main job is to keep your team in the loop. That means providing all relevant financial information, flagging any changes in your life or goals, and showing up for review meetings.

- The Investment Advisor/Manager: This is the person or firm executing the strategy. Their duties include implementing the plan, vetting investments, keeping a close eye on performance, and suggesting changes that align with the IPS.

- The Custodian: This is the institution that actually holds your assets. They’re responsible for safekeeping, processing trades, and sending out account statements.

- Trustees or Committee Members: If you have a trust or a family investment committee, their specific oversight duties and responsibilities for ensuring IPS compliance get spelled out here.

By getting this down on paper, you create a clear system of accountability. Everyone knows their lane, which is absolutely essential for things to run smoothly. You might also find our article on understanding investment management fees useful here, as it sheds light on the advisor's role and how they're compensated.

Communication and Reporting Protocols

Good communication is the lifeblood of any successful client-advisor relationship. Instead of leaving it to chance, the IPS should formalize how and when you'll connect. This simple step prevents misunderstandings and makes sure you always have a clear, transparent view of what’s happening with your portfolio.

This part of the document should specify:

- Reporting Frequency: How often will you get formal performance reports? Most families opt for quarterly.

- Meeting Schedule: When will you sit down for a formal review? This is typically done annually or semi-annually.

- Communication Channels: What are the best ways to handle quick, ad-hoc questions or updates?

Setting these ground rules from the start ensures a disciplined, proactive approach to managing your wealth. Everyone stays informed and on the same page.

Performance Benchmarks and Review Standards

So, how will you know if your strategy is actually working? The IPS answers that by setting up the right benchmarks to measure performance. These aren’t just picked out of a hat; they should be well-known indices that actually reflect your portfolio’s specific mix of assets. For instance, the U.S. large-cap stock portion of your portfolio might be measured against the S&P 500, while your bonds could be benchmarked against the Bloomberg U.S. Aggregate Bond Index.

A well-crafted IPS is crucial for curbing emotional investing by committing you to a long-term strategy with specific guidelines. For instance, the CFA Institute outlines key IPS components like risk tolerance and liquidity needs, which are fundamental in guiding a portfolio manager's asset allocation decisions, as you can discover in more detail from the Corporate Finance Institute.

This section also details your rebalancing strategy. You need to define the "trigger points" for bringing your portfolio back in line with its targets. A common, practical approach is to rebalance whenever an asset class drifts more than 5% from its target weight. This keeps your portfolio’s risk profile from accidentally creeping up over time.

Finally, your IPS should include any specific investment restrictions—your "do not buy" list. For many high-net-worth families, this is where personal values come into play through ESG (Environmental, Social, and Governance) screening, like excluding investments in tobacco or fossil fuels. It can also be used to prohibit certain complex or speculative investments, adding another layer of personalized risk control.

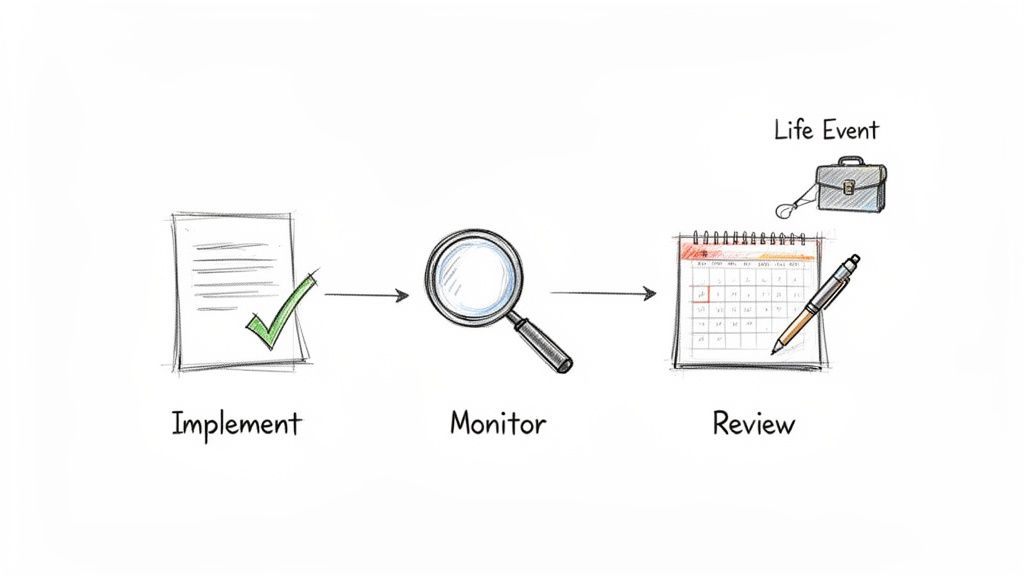

Bringing Your IPS to Life With Monitoring and Reviews

Getting your investment policy statement finalized is a huge accomplishment, but it’s really just the starting line. An IPS isn't meant to be filed away in a drawer; it has to be a living document that breathes and evolves right alongside your financial life. Its true power comes from putting it to work day in and day out, turning it from a static plan into your go-to management tool.

Once the ink is dry, the real work begins. Your advisor will immediately use its detailed guidelines to build or realign your portfolio. Every security, fund, and asset class should serve the specific purpose you’ve laid out. This is where the strategic vision on paper becomes a tangible financial reality.

The Cadence of Ongoing Monitoring

With the portfolio in place, the focus shifts to diligent monitoring. This is a constant process where your advisory team tracks your investments against the specific benchmarks you agreed upon in the document. This isn't about getting distracted by daily market headlines; it's a disciplined review of performance relative to your goals.

This systematic oversight is critical. It gives you an objective, data-driven way to evaluate whether your strategy is on track. Without it, performance reviews can get subjective and clouded by recent market noise, often leading to poor, reactive decisions. Your IPS keeps every conversation grounded in the long-term plan.

Your IPS acts as a behavioral guardrail. It anchors you and your advisor to a pre-agreed strategy, preventing emotional reactions to market volatility and ensuring decisions are made with discipline and a long-term perspective.

Consistent monitoring also keeps your portfolio's risk profile from getting out of whack. Over time, asset classes that perform well can grow to represent a much larger slice of your portfolio than intended, quietly ratcheting up your overall risk exposure. We call this "portfolio drift."

Rebalancing Your Portfolio Strategically

To counteract this drift, the IPS spells out a clear rebalancing strategy. This is simply the methodical process of trimming some of the assets that have grown beyond their target and buying more of those that have fallen below it. Think of it as a disciplined, automated way to "buy low and sell high."

There are a couple of common approaches to rebalancing, which your IPS should specify:

- Calendar-Based Rebalancing: This involves reviewing and adjusting the portfolio on a set schedule, like quarterly or annually. It provides a consistent, predictable routine.

- Threshold-Based Rebalancing: Here, you only take action when an asset class deviates from its target by a predetermined amount (e.g., more than 5%). This approach can be more opportunistic, responding directly to big market moves.

By codifying these rules, the IPS takes emotion out of the equation. It stops you from holding onto winners for too long or ignoring asset classes that are temporarily out of favor. If you want to dive deeper into the mechanics, our guide on what portfolio rebalancing is offers a much more detailed explanation.

Knowing When to Review the IPS Itself

While the portfolio is monitored constantly, the IPS document itself needs a thoughtful review from time to time. You should sit down with your advisor for a formal review at least once a year to make sure its core principles—your goals, constraints, and risk tolerance—are still on point.

However, some life events should trigger an immediate and thorough review of the entire document. An IPS is only effective if it mirrors your current reality.

Key triggers for an IPS review include:

- A Major Liquidity Event: Selling a business, exercising a big block of stock options, or receiving a large inheritance can fundamentally change your financial picture and what you want to achieve.

- Changes in Family Structure: Getting married or divorced, having a child, or the death of a spouse all have profound implications for your financial plan and legacy goals.

- Shifts in Long-Term Goals: Deciding to retire early, launch a major philanthropic initiative, or change your estate plans requires a strategic reassessment.

- Significant Tax Law Changes: New legislation can impact everything from estate planning to how investment gains are taxed, often demanding a strategic pivot.

This proactive review process ensures your Investment Policy Statement remains a relevant, powerful, and perfectly aligned guide for managing your wealth for years to come. It’s the mechanism that guarantees your financial constitution adapts to the changing seasons of your life.

Your Top Questions About the IPS, Answered

Even after you understand all the moving parts, actually sitting down to create an investment policy statement can bring up some valid questions. It's a common concern for high-net-worth families: how do we create a document that provides real discipline without tying our hands?

Let's walk through some of the most frequent questions we hear from clients. Getting these answers straight will help you move forward with more confidence, knowing you're building a truly valuable strategic framework.

How Often Should We Review Our Investment Policy Statement?

As a rule of thumb, you should plan for a formal review of your IPS with your advisor at least once a year. This yearly check-in ensures the document is still a true reflection of your current financial picture and what you want to achieve long-term.

That said, your IPS isn't something you can just set and forget. It has to be revisited immediately after any significant life event. These are the moments that can completely change the core assumptions your entire strategy was built on.

An IPS is designed to keep you steady during normal market ups and downs, so you shouldn't be changing it every time the market gets choppy. But a major shift in your personal life is a different story—that demands a fresh look to make sure your strategy still fits your new reality.

What kind of events are we talking about? Be ready to call your advisor for an immediate IPS review after:

- Selling a business or having another major liquidity event

- Receiving a significant inheritance or gift

- Changes in your family, like a marriage, divorce, or new baby

- A fundamental change in your thinking about your legacy or philanthropic goals

What Happens if My Advisor Doesn't Follow the IPS?

Think of the IPS as a formal agreement. It creates a powerful layer of accountability. If an advisor intentionally deviates from the guidelines you both agreed on without getting your documented consent first, that's a serious problem. It could even be considered a breach of their fiduciary duty.

This document is your protection. It gives you an objective, written standard that all investment decisions must be measured against. If you spot something that doesn't look right—maybe your asset allocation has drifted way outside the target ranges, or a type of security you specifically prohibited shows up in your account—you need to bring it up with your advisor right away.

The IPS gives you a clear, authoritative starting point for that conversation and for getting things back on track. It cuts through any ambiguity and makes sure both you and your advisor are playing by the same set of rules.

Can an IPS Be Too Restrictive and Cause Me to Miss Opportunities?

This is a great question, and we hear it all the time. The fear is that a rigid set of rules will stop an advisor from being able to jump on a great market opportunity when it appears. But a well-designed IPS is all about balancing discipline with strategic flexibility. It’s meant to set up guardrails, not put you in a straitjacket.

For example, your asset allocation won't be a single, fixed number. It will be defined with target ranges, something like 50-60% in equities. That built-in wiggle room gives your advisor the tactical space they need to make smart adjustments based on market conditions, all while staying within the framework you've already approved.

The goal isn't to handcuff your advisor. It's to make sure that every single action they take, whether it's playing offense or defense, is directly supporting your long-term goals and staying within the risk levels you’re comfortable with. The IPS ensures that any "opportunity" is always seen through the lens of your personal objectives. At the end of the day, it actually empowers your advisor to act decisively, because they're operating within a pre-approved strategic plan. You get the best of both worlds.

At Commons Capital, we believe a meticulously crafted Investment Policy Statement is the cornerstone of disciplined, long-term wealth management. We partner with high-net-worth families to build a strategic framework that aligns with their unique vision for the future. Learn how our personalized approach can bring clarity and confidence to your financial life.