Let's get straight to the point: what's the real difference between 401k and 403b plans?

The simplest answer is who offers them. 401(k) plans are the standard for private, for-profit companies. 403(b)s, on the other hand, are for public service and non-profit organizations — think schools, hospitals, and charities. While they look similar on the surface, this one distinction drives some critical differences for investors.

Understanding the Core Differences

At first glance, you could mistake a 401(k) and a 403(b) for being two sides of the same coin. Both are powerful, tax-deferred retirement accounts that help you save for the future. But the employer type — for-profit vs. non-profit — is the linchpin that dictates everything from plan administration and investment options to some very specific contribution rules.

For high-net-worth individuals, these subtleties are more than just trivia. Understanding them is key to maximizing your own savings, advising a spouse, or even fulfilling your duties if you sit on a non-profit board.

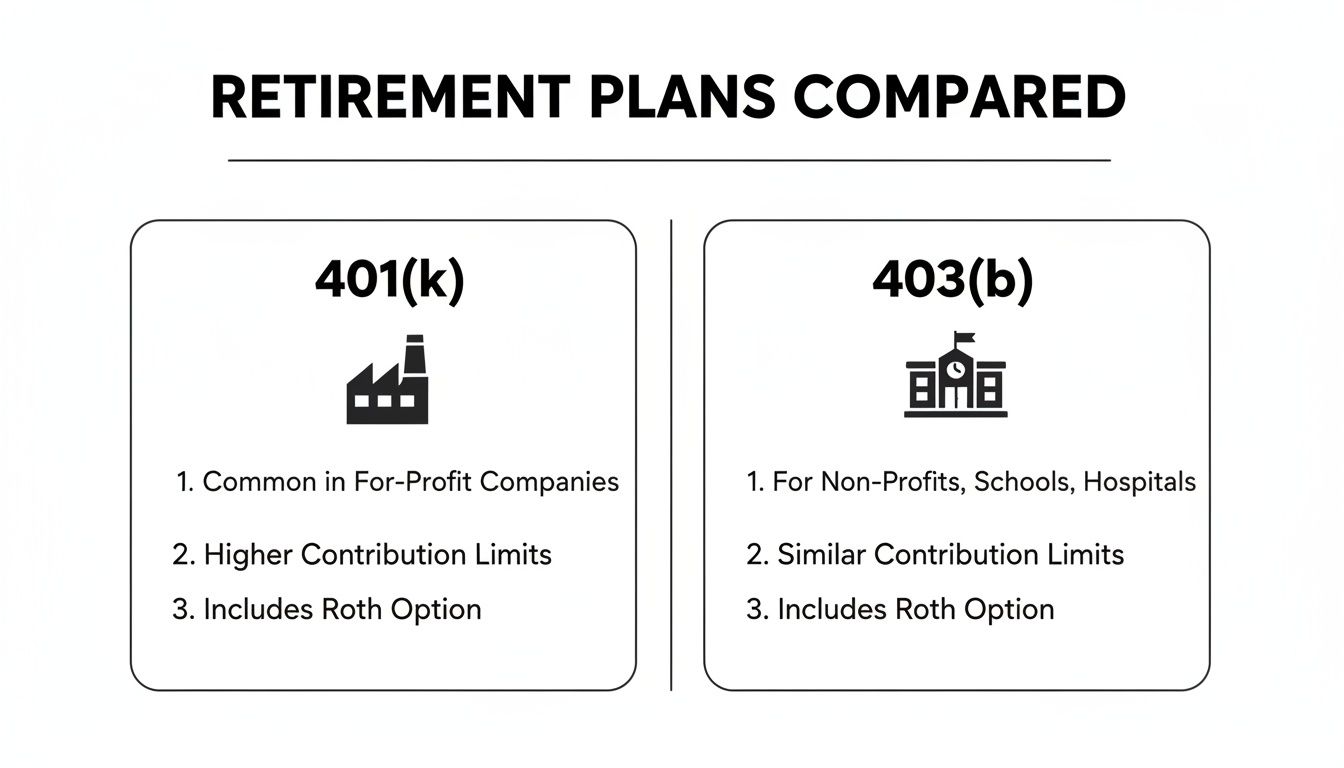

This visual guide quickly breaks down the core distinctions.

As the graphic shows, 401(k)s belong to the world of private industry, while 403(b)s serve the public and non-profit sectors. But that’s just the beginning of the story. Now, let’s dig into the practical implications for a savvy investor.

Key Distinctions 401k vs 403b at a Glance

To set the stage for a deeper dive, it helps to see a direct, side-by-side comparison of their main attributes. Although the IRS standardizes many contribution limits across both plan types, the underlying architecture can be surprisingly different.

This table provides a high-level snapshot of their primary characteristics.

As you can see, the difference between 401k and 403b extends far beyond just the employer type. It's worth taking the time to compare 403(b) plans versus 401(k)s in more detail to really understand the nuances.

Throughout this guide, we’ll unpack how these distinctions impact everything from your investment choices and fee structures to unique contribution rules you might be able to take advantage of.

Who Can Get a 401(k) vs. a 403(b)?

When you're trying to figure out the difference between 401k and 403b plans, it all boils down to one simple question: Where do you work? This isn't just a minor detail; it’s the primary gatekeeper that decides which plan you can access. It's a clear-cut rule that shapes the retirement path for millions of Americans.

Simply put, 401(k) plans are the standard for the for-profit, private sector. If you work for a tech startup, a law firm, a publicly traded company, or just about any other private business, a 401(k) is almost certainly the retirement plan you'll be offered.

In contrast, 403(b) plans are set aside for people working in public service and non-profit roles. These plans are exclusively for employees of 501(c)(3) non-profit organizations and some public sector employers.

Defining 403(b) Eligibility

The exclusive nature of the 403(b) means it's built for a very specific group of professionals. Knowing who falls into this bucket is key, especially for families where careers span different sectors.

So, who gets a 403(b)?

- Educators: Think teachers, professors, administrators, and other staff at public schools, colleges, and universities.

- Healthcare Professionals: Doctors, nurses, and other staff working at non-profit hospitals and medical centers.

- Non-Profit Employees: Anyone on the payroll at charitable organizations, foundations, and other 501(c)(3)s.

- Religious Workers: Ministers and certain employees of churches and other religious organizations.

This strict divide based on employer type creates two massive, but very different, retirement ecosystems. While 401(k)s are everywhere in the corporate world, 403(b)s represent a huge savings pool for the public service sector. To give you a sense of scale, by 2020, 403(b) plans held over $1.1 trillion in assets, earmarked for the retirements of millions of mission-driven professionals.

For high-net-worth families, this eligibility line in the sand has real strategic weight. Career choices — for you, a spouse, or even your kids — directly determine which retirement tools are available, which in turn impacts your entire financial plan and legacy.

Participation Rules and Demographics

Beyond the fundamental employer type, individual organizations can set their own rules for when you can join a plan. These usually involve a minimum age or a certain period of service. For example, a company might require you to be 21 years old and have worked there for a year before you're eligible to start contributing.

Interestingly, just having access doesn't mean everyone signs up. A study of North Carolina school personnel, for instance, found that only 32% participated in any available retirement plan. This gap between access and action is a major challenge for plan sponsors and a talking point for financial advisors. If you want to dig deeper into plan mechanics, you can explore more detailed plan comparisons on Guideline.com.

Ultimately, your career path opens the door to either the 401(k) or the 403(b). Knowing which plan you and your family members can use is the very first step in building a smart retirement strategy. It's the true starting point of this entire comparison.

How Contribution Limits and Catch-Up Rules Compare

At first glance, the core contribution limits for 401(k) and 403(b) plans look identical. The IRS sets the same ceiling for both, and for 2024, that number is $23,000 for anyone under 50. This often leads people to think the plans are mirror images in their savings power, but that's a mistake that overlooks a few crucial details.

The real strategic difference between 401k and 403b plans starts to show when you dig into the catch-up contribution rules. While both offer a standard boost for older savers, the 403(b) has a unique provision that can be a game-changer for long-tenured professionals in the non-profit world.

The Standard Age 50 Catch-Up

First, let's cover the basics. Both 401(k) and 403(b) plans allow participants who are age 50 or older to put away extra cash on top of the standard annual limit. For 2024, this age-based catch-up is $7,500.

This means an employee aged 50 or older can contribute a total of $30,500 to either plan — that's the $23,000 standard limit plus the $7,500 catch-up. For a lot of people, the story ends right there. But for a select group of 403(b) participants, this is where it gets interesting.

The Special 15-Year Service Catch-Up

Here’s a powerful, and often missed, feature exclusive to 403(b) plans. Certain employees with 15 or more years of service with the same employer — think public school systems, hospitals, or home health agencies — might qualify for a special catch-up contribution. The rule is really designed to help long-serving employees who might have saved less early in their careers finally make up for lost time.

This special provision lets an eligible employee contribute an additional amount, but it comes with some specific strings attached:

- An extra $3,000 per year.

- A lifetime maximum of $15,000 for this specific type of catch-up.

- The catch-up is only available if past contributions were less than an average of $5,000 per year.

It’s critical to understand that you can't double-dip on catch-ups in the same year if the excess amount is identical. The IRS makes you choose whichever provision — the age 50 or the 15-year rule — results in the larger contribution for that year.

A Practical Scenario Unpacking the Advantage

Let's see how this plays out with two 55-year-old professionals, both high earners trying to max out their retirement funds.

Scenario 1: The Corporate Executive

- Plan: 401(k)

- Maximum Contribution: $23,000 (standard) + $7,500 (age 50 catch-up) = $30,500

Scenario 2: The Hospital Administrator

- Plan: 403(b)

- Tenure: 20 years of service at the same non-profit hospital.

- Past Contributions: She averaged less than $5,000 per year over her career.

- Maximum Contribution: She can contribute the standard $23,000 plus her age 50 catch-up of $7,500. The $3,000 service-based catch-up is smaller than her age-based one, so the IRS requires her to use the larger of the two. Her max is still $30,500.

So where's the edge? The real power move for a 403(b) participant often comes from stacking their plan with a 457(b) plan, which is frequently offered by the same non-profit employers. The specialized 15-year catch-up rule can create a huge savings opportunity in specific situations, especially when planning across multiple account types.

For instance, this nuanced rule can give veteran non-profit employees an edge, as some 403(b) plans permit using the lifetime catch-up in years before or after age 50. When you pair a 403(b) with a 457(b), you can potentially skyrocket your savings far beyond what a 401(k) alone allows. To see how these figures stack up, you can discover more insights about 403b plan strategies on WealthTender.com. This makes the 403(b) an incredibly valuable tool for long-serving public sector executives aiming to accelerate their wealth accumulation before retirement.

Analyzing Employer Match and Vesting Schedules

An employer match is one of the most powerful wealth-building tools you'll find in a retirement plan. Think of it as an instant return on your investment before your money even has a chance to grow. But the generosity and structure of these matches often reveal a key practical difference between 401k and 403b plans, a distinction rooted in the economic realities of the for-profit versus non-profit sectors.

In the competitive for-profit world, companies lean heavily on robust 401(k) matches as a critical piece of their compensation packages. It's a key tool for attracting and keeping top talent. It’s not at all unusual to see a common formula like a match of 50% of the first 6% of an employee's contributions. In plain English, that’s an extra 3% of your salary dropped directly into your retirement account.

On the other hand, employer matches in 403(b) plans can be far less consistent. While many larger non-profits — think hospitals and universities — do offer a match, it’s frequently less generous than what their corporate counterparts provide. Budgetary constraints are a real factor here, and some smaller non-profits might not offer a match at all.

Understanding Vesting Schedules

Beyond the match itself, you have to understand when you actually own the money your employer puts in. This is all governed by a vesting schedule, which is just a timeline that determines your ownership rights to your employer’s contributions. Your own contributions, to be clear, are always 100% yours from day one.

You'll typically run into two main types of vesting schedules:

- Cliff Vesting: With this model, you gain 100% ownership of all employer contributions at once, but only after a specific period of service — up to three years. If you leave your job before hitting that "cliff" date, you walk away with nothing from your employer.

- Graded Vesting: This schedule lets you gain ownership incrementally. A very common example is a six-year graded schedule where you become 20% vested after two years of service, then an additional 20% each year after that until you’re fully vested after six years.

The Strategic Impact of Vesting on Your Finances

The vesting schedule is a crucial detail that often gets buried in the fine print of plan documents. For an executive weighing multiple job offers, the vesting rules can have a massive financial impact. A role with a three-year cliff vesting schedule is a big gamble if you aren't sure you'll stick around for the full term.

A generous employer match is only valuable if you stick around long enough to own it. When weighing a total compensation package, you must analyze both the matching formula and the vesting schedule to accurately project your long-term portfolio growth.

Because 403(b) plan sponsors often aim to encourage long-term employee retention through mission alignment rather than just pure compensation, some may actually offer more favorable vesting terms. It's not unheard of for 403(b) plans to have immediate vesting, where you own employer contributions the moment they hit your account. This gives your savings an immediate, undeniable boost and removes the "golden handcuffs" that come with long vesting periods.

Ultimately, the combination of the employer match and its vesting schedule is a critical point of comparison between 401(k) and 403(b) plans. For any high-net-worth individual, scrutinizing these details is absolutely essential for making smart career moves and maximizing every dollar available for retirement.

Comparing Investment Options and Fee Structures

The investment lineup is where the real daylight often appears between 401(k)s and 403(b)s. While things like contribution limits are set by federal rules, the actual investments available to you can be worlds apart. For any serious investor, digging into these differences is crucial for spotting hidden costs and getting the most out of your portfolio over the long haul.

Historically, 403(b) plans were almost synonymous with annuity products and a very narrow menu of mutual funds, typically all from one big insurance company. This old-school structure often meant higher fees and not much in the way of investment choice. While the landscape is getting better, many 403(b)s — especially those in smaller school districts or nonprofits — still operate on this annuity-heavy model.

In contrast, 401(k) plans almost always offer a much wider investment universe. You’re far more likely to see a diverse roster of mutual funds from many different companies, low-cost exchange-traded funds (ETFs), and in some cases, even individual stocks or company stock. This broader selection simply gives you more control to build a diversified and cost-effective portfolio.

The Vendor and Fee Landscape

The plan's vendor directly impacts both your investment choices and, critically, how much you pay. A key reason for the difference is that many 403(b) plans are not subject to ERISA (the Employee Retirement Income Security Act), the strict law that governs most 401(k)s. This means their fee structures can be less transparent and often much higher. ERISA forces 401(k) plan sponsors to act as fiduciaries, a legal duty to act in the best interest of employees, which includes picking reasonably priced investments.

For instance, it wasn't uncommon for a single school district's 403(b) to have multiple vendors, creating a confusing and expensive mess for teachers. This multi-vendor approach can drive up administrative costs and often relies on commission-based insurance products.

When you're looking at any plan, you have to scrutinize these key fees:

- Administrative Fees: These are the costs for recordkeeping, accounting, and general plan management. They might be a flat annual fee or a percentage of your assets.

- Investment Fees: Also called expense ratios, these are what the mutual funds or annuities charge. High expense ratios can seriously eat into your returns over time.

- Individual Service Fees: These are extra charges for specific actions, like taking out a plan loan or processing a rollover.

The long-term impact of fees is staggering. A seemingly small 1% difference in annual fees can slash your final retirement balance by nearly 28% over a 35-year career. This makes fee analysis an absolutely non-negotiable step when evaluating a retirement plan.

Investment Choices and Modern Plan Design

Modern 401(k)s often include investment options built for more sophisticated plans, like Collective Investment Trusts (CITs). These can be a powerful way for companies to lower costs for their employees. You can learn more about the advantages of Collective Investment Trusts in our detailed guide. While CITs are gaining traction in 401(k)s, they remain a rarity in the 403(b) world.

This gap in investment quality and cost can actually influence how much people save. Recent data showed that average savings rates in 403(b) plans hit 11.5% in late 2023. At the same time, 401(k) plans saw a stronger rate of 13.9%. This difference is often chalked up to factors like the more generous employer matches and better investment options typically found in for-profit 401(k) plans. You can see the full report on 403(b) participation and savings rates on PlanSponsor.com.

If you’re a high-net-worth individual, particularly one who serves on a nonprofit board, you're in a unique position. Pushing for a modern, low-cost, multi-asset 403(b) can make a huge difference for every employee. Advocating for a move away from high-fee annuities and toward a solid lineup of low-cost index funds and ETFs can dramatically improve retirement outcomes for everyone. The trend is slowly shifting, but it takes vigilance.

Strategic Retirement Planning In Action

It’s one thing to know the technical difference between a 401k and a 403b. It's another thing entirely to apply that knowledge to your own financial life. For high-net-worth individuals and families, retirement planning is rarely about just one account. It’s about making multiple accounts and strategies work together to cut your tax bill and build wealth faster.

So let’s move past the theory. Here are some actionable strategies for common, yet complex, situations. These scenarios will give you a clear sense of how to line up your retirement plan choices with your bigger financial goals.

The High-Earning Power Couple

Let's start with a classic scenario: a high-earning couple where one spouse is a corporate lawyer with a 401(k) and the other is a university professor with a 403(b). Their combined income easily pushes them into a high tax bracket, so tax-deferred growth is a huge priority.

Their main goal is simple: max out contributions across every retirement account they have.

- Step 1: Maximize Both Plans. Each spouse needs to contribute the maximum allowed to their own plan, and that includes any age 50+ catch-up contributions. The limits are individual, not household-based, which means they could sock away a combined $61,000 in 2024 if both are over 50.

- Step 2: Grab the Free Money. They need to make sure both are contributing at least enough to get the full employer match. This is free money — a critical part of their total compensation that should never be left on the table.

- Step 3: Look for a 457(b). The professor should see if her university also offers a governmental 457(b) plan. If it does, she can contribute to both her 403(b) and the 457(b), basically doubling her personal tax-deferred savings. This is a massive advantage her corporate spouse doesn't have.

- Step 4: Coordinate Investments. They should sit down and compare the investment menus in both plans. If the 401(k) has better, lower-cost index funds and more variety, they might lean their asset allocation more heavily into that plan while still maxing out the 403(b). And when it's time to roll money over, knowing how to convert a 401(k) to a Roth IRA can create valuable tax diversification down the road.

The Long-Tenured Non-Profit Executive

Now, imagine a 58-year-old hospital CFO who has spent 22 years at the same non-profit medical center. As a high earner, she wants to seriously accelerate her savings in her final working years. This is the perfect time to leverage the special 15-year service catch-up rule, something only 403(b) plans offer.

For long-serving employees in the non-profit world, the 15-year service catch-up is a powerful but often misunderstood tool. It demands careful calculation and close work with the plan administrator to stay compliant and get the most out of it.

Her strategy starts with a deep dive into her contribution history. If her average annual contributions over her career were less than $5,000, she can contribute an extra $3,000 per year, up to a lifetime cap of $15,000. Even though her age 50+ catch-up is larger, she can still use this special rule strategically to hit that lifetime cap before she retires.

The Business Owner's Decision

Finally, let's look at a successful entrepreneur running a growing for-profit consulting firm. She wants to add a retirement plan to attract and hold onto top talent. For her, the choice is clear: a 401(k) plan. A 403(b) simply isn’t an option for a for-profit business.

Her focus immediately pivots to plan design. She could set up a Safe Harbor 401(k) to automatically pass the IRS's non-discrimination tests, offer a generous employer match to compete with bigger companies, and pick a low-cost provider with a wide array of investment choices. For employees coming from government jobs, knowing the ins and outs of things like rolling over a TSP into a 401k shows a sophisticated understanding of retirement needs, making her firm that much more appealing.

Your Top Questions About 401(k) and 403(b) Plans Answered

Once you get a handle on the basic differences, the real-world questions start popping up. Let's walk through some of the most common ones we hear from clients. Getting these details right is key to navigating your retirement planning with confidence, especially when the difference between a 401k and 403b isn't always cut and dried.

Can I Contribute to Both a 401(k) and a 403(b) at the Same Time?

Yes, you absolutely can. This usually happens when you have two jobs — say, a full-time gig at a private company and a part-time position at a nonprofit university.

But here’s the critical detail: while you have two separate plans, your personal contribution limit is combined for the year. For 2024, that total is $23,000. If you're 50 or older, it's $30,500. You can't max out both plans; the IRS views it as one single bucket for your employee contributions.

What Should I Do With an Old 403(b) or 401(k) When I Change Jobs?

When you leave a job, you’ve got a few options for that old retirement account. There’s no single “best” answer here — the right move really depends on your financial picture, how you like to invest, and the quality of the plans you have access to.

Here are your main choices:

- Leave the money where it is. This is often an option if your balance is over $5,000. It's simple, but you're stuck with that plan's investment menu and fees.

- Roll it into your new job's plan. Consolidating accounts can make life easier. Before you do, though, compare the fees and investment choices of the new plan to see if it’s a good home for your money.

- Roll it over into an Individual Retirement Account (IRA). A rollover IRA almost always gives you the widest investment selection and the most control. This is a very popular move for hands-on investors.

- Cash it out. This is almost always a terrible idea. You'll likely get hit with a big income tax bill plus a 10% early withdrawal penalty if you're under 59½. It can do serious, long-term damage to your savings.

A direct rollover is the cleanest way to move your money. Whether you're going from your old plan to a new one or to an IRA, a direct transfer ensures you don't trigger any taxes and your retirement funds stay invested and working for you.

Are Roth Versions Available for Both 401(k) and 403(b) Plans?

Yes, and this adds a fantastic layer of strategy. Many employers now offer Roth options for both 401(k) and 403(b) plans. With a Roth, your contributions go in after-tax — meaning you've already paid taxes on that money.

The big payoff comes later. Your qualified withdrawals in retirement are 100% tax-free. This can be an incredibly powerful tool if you think your tax bracket will be higher down the road, or if you just want the peace of mind that comes with tax-free income in your later years. Deciding between Traditional (pre-tax) and Roth (after-tax) is one of the most important financial planning decisions you'll make.

Navigating the complexities of 401(k)s, 403(b)s, and your overall investment strategy requires expert guidance. At Commons Capital, we specialize in creating financial plans for high-net-worth individuals and families. Visit us at https://www.commonsllc.com to learn how we can help you achieve your financial goals.