Wondering "do I need a trust?" The short answer is: if you want to keep your family’s financial affairs private, bypass the lengthy and public court process of probate, and have precise control over your assets, then a trust is likely the right move for you. While a will is a good start, it’s a public document that requires a judge to oversee its execution. A trust, by contrast, is a private instruction manual for your assets that works during your life, if you become incapacitated, and after your death — all without court intervention.

This guide will break down what a trust is, demystify the idea that they are only for the ultra-wealthy, and show you the real-world scenarios where a trust is the smartest way to secure your legacy and protect your family’s future.

Understanding the Shift Towards Trusts

The question "do I need a trust?" is becoming more common as people seek better ways to manage their estates. For decades, a last will and testament was considered the primary estate planning tool. However, a will alone often can't address the complexities of modern finances or specific family situations.

A will is a static document that only becomes active after you die, and its execution is supervised by the courts in a public process called probate. This frequently leads to frustrating delays, unexpected legal fees, and a complete loss of privacy for your family. This is precisely why a trust offers a more powerful and private method for managing and passing on your wealth.

Why More People Are Choosing Trusts

The growing interest in trusts is a practical response to the limitations of a will. The U.S. Trusts & Estates industry is projected to reach $290.1 billion by 2025, largely because people want more control, privacy, and security. With a staggering 55% of U.S. adults lacking even basic estate documents, a trust is increasingly viewed as a critical safeguard, not a luxury.

The main reasons individuals are turning to trusts include:

- Avoiding Probate: A properly funded trust allows your assets to pass directly to your beneficiaries without court interference, saving time, money, and stress.

- Ensuring Privacy: A will becomes a public record. A trust keeps your financial details and beneficiary designations completely confidential.

- Planning for Incapacity: If you become unable to manage your affairs, a trust allows a hand-picked successor trustee to step in and manage your finances seamlessly.

- Controlling Asset Distribution: You can set specific conditions for how and when beneficiaries receive their inheritance, which is ideal for protecting assets for young children or loved ones unprepared for a sudden windfall.

A trust isn't just about what happens after you're gone. It's a living document that provides protection and control throughout your life, offering peace of mind that a simple will cannot match.

For a deeper look at whether a trust is right for you, this clear guide to Texas estate planning offers excellent insights. Although it's state-specific, the core principles apply almost universally. As we continue, we will explore these concepts further to help you decide if a trust aligns with your personal goals.

Quick Guide: When a Trust Makes Sense

Sometimes, a simple checklist is the best way to determine if a trust is the right fit. Here are several common scenarios where a trust is often the superior choice over a will alone.

If any of these situations resonate with you, it's a strong indicator that a conversation about a trust is worthwhile. A trust provides a level of precision and protection that a will simply cannot offer.

Comparing a Will Versus a Trust

When people begin estate planning, the first question is often: will or trust? Both are fundamental tools, but they function in completely different ways. Understanding these differences is the first step toward creating the right strategy for your assets and your family’s future.

A will is a legal document outlining your wishes for asset distribution after you die. Think of it as a letter of instruction to the court system. After you pass away, your will is filed with a court and enters a public process called probate. A judge then validates the will, settles any debts, and oversees the transfer of your assets to your named heirs.

A trust, conversely, is a private legal arrangement. When you create a trust, you establish a new entity, transfer your assets into it, and appoint a trustee to manage them for your beneficiaries. The crucial difference is that a trust is active from the moment you set it up and continues to operate seamlessly after you're gone — completely avoiding the probate process.

The Critical Role of Probate

If there’s one thing to understand, it’s this: the primary distinction between a will and a trust is probate. A will guarantees probate; a trust is designed to avoid it.

So what's the issue with probate? It is often a long, expensive, and very public affair. The process can drag on for months, sometimes over a year, during which your assets are effectively frozen. Your heirs cannot access them. Furthermore, legal fees, court costs, and executor fees can easily consume 3% to 8% of your estate's total value, reducing the inheritance you worked so hard to build.

Then there's the privacy issue. Probate is a public record. This means every detail of your will — the value of your assets, who receives what, and who receives nothing — is available for anyone to see. For families who prefer to keep their financial matters private, this is a significant drawback.

A will is an instruction to the court system, making your estate a public matter. A trust is a private agreement that keeps the court system out of your family’s affairs.

Control During Life and After Death

Another key difference is when these documents become effective. A will does absolutely nothing until you die. It has no authority while you're alive, meaning it offers zero protection if you become incapacitated and cannot manage your own affairs.

In that scenario, your family would have to go to court to petition for a conservatorship or guardianship. This is another public, costly, and emotionally draining legal process, at a time when they are already under stress.

A living trust, however, is effective the moment it is created and funded. If you become incapacitated, your chosen successor trustee can immediately step in to manage your finances without court intervention. It's a seamless transition that ensures your bills are paid and your assets are managed exactly as you intended. That peace of mind is invaluable. For a deeper dive, you can explore the key differences between a living trust vs a will and how they perform in these scenarios.

Privacy and Asset Protection

The privacy a trust provides cannot be overstated. By avoiding probate, the details of your estate plan — how much you had and who you left it to — remain completely confidential. This protects your beneficiaries from nosy neighbors, predatory financial advisors, and potential scammers.

While a standard revocable living trust doesn't offer creditor protection while you're alive, certain types of irrevocable trusts can build a powerful fortress around your assets, shielding them from future lawsuits or creditors. A will offers no such protection. Once assets pass through probate, they are exposed to the public, making a trust a far superior tool for long-term legacy preservation.

Understanding Different Types of Trusts

Once you understand how a trust can offer more control and privacy than a will, the next step is determining which type is right for you. While trusts can be highly specific, they generally fall into two main categories: revocable and irrevocable.

The distinction hinges on one simple question: Can you change your mind later?

The answer to that question affects everything, from your level of control to the tax and asset protection benefits you receive. Think of them as two distinct tools in your estate planning toolkit.

Revocable Living Trusts: The Flexible Blueprint

The Revocable Living Trust is the most common choice for many people, and for good reason — it’s a flexible blueprint for your estate. You create it, transfer your assets into it, and remain in complete control as the trustee. You can amend the terms, add or remove assets, or even dissolve it entirely if your circumstances change.

It’s like putting your assets into a personal safety deposit box where you hold the only key. You can move items in and out at will. This trust’s primary purpose is to bypass the costly and public probate process, which it does effectively. It also establishes a smooth transition plan if you become incapacitated, allowing your successor trustee to take over without a court order.

A revocable trust gives you maximum flexibility while you're alive. Its main goals are avoiding probate and planning for incapacity, but it won’t shield your assets from creditors or reduce estate taxes.

Because you retain control, the assets within a revocable trust are still considered yours by the law and the IRS. This means they are not protected from lawsuits or creditors and are included in your taxable estate upon death. For a deeper look, check out this guide on understanding a revocable living trust and its day-to-day functions.

Irrevocable Trusts: The Secure Vault

An Irrevocable Trust, in contrast, is structured more like a secure vault. Once you sign the documents and place assets inside, you generally cannot change the terms or retrieve the assets. By formally relinquishing control and ownership, you create a distinct legal entity to hold those assets for your beneficiaries.

Why would anyone do this? The benefits can be immense. Because the assets are no longer legally yours, they are typically protected from future creditors, lawsuits, and — most importantly for many high-net-worth families — estate taxes. This makes irrevocable trusts an essential tool for preserving wealth across generations.

This strategy is increasingly important. The federal estate tax exemption, currently at $13.61 million, is scheduled to be cut in half in 2026. In response, 86% of financial advisors are now recommending strategies like irrevocable trusts to help clients protect their wealth. With an estimated $84.4 trillion expected to be transferred between generations in the coming years, not having a plan is a significant risk.

Irrevocable trusts can be designed for specific objectives:

- Irrevocable Life Insurance Trust (ILIT): Keeps life insurance proceeds out of your taxable estate.

- Grantor-Retained Annuity Trust (GRAT): A powerful tool for transferring asset appreciation to heirs with minimal gift or estate tax.

- Charitable Remainder Trust (CRT): Allows you to arrange a future gift to charity while receiving an income stream and significant tax benefits today.

It's a powerful tool, but one that requires careful consideration. It’s worth digging into the specific pros and cons of an irrevocable trust to see if this level of permanence aligns with your goals. The choice between revocable and irrevocable really comes down to your priorities: flexibility and control, or ironclad protection and tax efficiency.

Revocable vs Irrevocable Trusts Head-to-Head

To make the choice clearer, here’s a breakdown of the key differences between these two powerful estate planning tools. This should help you start thinking about which structure might be a better fit for your family’s needs.

Ultimately, deciding on the right type of trust depends entirely on what you want to accomplish. Do you need a simple vehicle to avoid probate, or are you trying to solve more complex challenges like estate taxes and long-term asset protection? Your answer will point you in the right direction.

When Is a Trust Actually Necessary?

Knowing what a trust is and knowing when you need one are two different things. While a will forms the foundation of any estate plan, certain situations demand the precision and protection that only a trust can provide. These are not just fringe cases for the ultra-wealthy; they are common scenarios where a trust becomes the most important tool for protecting your family and your assets.

Often, the question "do I need a trust?" becomes clear when you see your own family's situation in one of these examples. Let's look at the real-world problems a trust is uniquely designed to solve.

Planning for Potential Incapacity

One of the most compelling reasons for a trust is planning for a time when you may be unable to manage your own affairs. A will is useless in this situation, as it only takes effect after your death. Without a trust, your family could face a lengthy, public, and expensive court process to have you declared legally incompetent just to appoint a guardian to pay your bills.

A revocable living trust allows you to avoid this entire ordeal. When you create the trust, you name a successor trustee — someone you have personally chosen — to step in and manage your finances immediately if you become incapacitated.

The transition is private, seamless, and occurs without a judge's approval. It ensures your life continues to run smoothly, with assets managed exactly as you'd want, even when you can't say so yourself.

Protecting Blended Families

Modern families are often complex, and a simple will can fall short in navigating the dynamics of a blended family. A trust, however, gives you the control to ensure everyone you love is cared for according to your specific wishes.

Consider a common scenario: you want to provide for your current spouse for the rest of their life but also want to guarantee that your assets eventually go to your children from a previous marriage. A will struggles to enforce this two-step process. A specific type of trust, such as a QTIP trust, handles it with legal precision.

- Your spouse receives income from the trust's assets for their lifetime, ensuring their comfort.

- The principal is preserved for your children, who will inherit it after your spouse passes away.

This structure locks in your plan, preventing the unintentional disinheritance of your children and protecting all your loved ones.

Managing Inheritances for Minor Children

You cannot legally leave a large sum of money directly to a minor. If you only have a will, a court will appoint a financial guardian to manage the money until your child turns 18. That process can be costly, and the person chosen by the court may not manage the funds as you would have. Then, on their 18th birthday, the child receives the entire inheritance in one lump sum — a potential disaster for most young adults.

A trust avoids all of this. You appoint a trustee you trust to manage the funds for the child’s well-being. More importantly, you get to set the rules. For example, you could instruct the trustee to pay for education and health expenses as needed, then distribute the inheritance in stages at more mature ages, like 25, 30, and 35.

Providing for a Beneficiary with Special Needs

If you have a child or another loved one with special needs who relies on government benefits like Medicaid or SSI, a direct inheritance can be catastrophic. Receiving even a modest sum can push their assets over strict limits, disqualifying them from essential services.

A Special Needs Trust is the solution. Assets in this type of trust are managed by a trustee and used to pay for supplemental needs — things government benefits don't cover, such as:

- Specialized medical equipment

- Enhanced therapy or rehabilitation services

- Educational programs

- Transportation and hobbies

This allows you to dramatically improve their quality of life without jeopardizing the critical government support they need.

Minimizing Estate Taxes and Maximizing Privacy

For high-net-worth families, estate tax planning is a major motivator. Certain irrevocable trusts are designed to move assets out of your taxable estate, which can significantly reduce — or even eliminate — the tax bill your heirs face. It is one of the most effective strategies for preserving wealth for the next generation.

Additionally, a trust keeps your family's financial affairs out of the public eye. When a will goes through probate, it becomes a public record. Anyone can see who you left money to, what assets you owned, and how much debt you had. A trust, however, is a private document. This privacy protects your family's inheritance from nosy neighbors, opportunistic creditors, and potential lawsuits. For a deeper dive, our guide on protecting assets from nursing home costs also covers some of these core asset protection ideas.

How Much Does It Cost to Set Up a Trust?

Let's discuss the practical side of creating a trust. While the upfront cost is higher than for a simple will, that initial investment often prevents much larger expenses — and headaches — for your family later on.

Think of it as preventative care for your estate. Probate fees, court costs, and legal bills can easily consume 3% to 8% of an estate's total value. A properly structured and funded trust is designed to avoid those expenses entirely, ensuring more of your legacy reaches your beneficiaries.

Breaking Down the Investment

The cost to set up a trust can vary significantly, depending on the complexity of your finances and your location. For a standard revocable living trust, attorney fees typically range from a few thousand to several thousand dollars. If you require something more specialized, like a trust for complex estate tax planning or to provide for a loved one with special needs, the investment will be larger.

However, you are paying for more than just documents. The cost includes:

- Expert legal counsel to understand your goals and design a trust that meets them.

- Drafting the trust agreement and all related paperwork, such as a pour-over will.

- Hands-on guidance for funding the trust, which is the most critical part of the process.

An unfunded trust is like an empty safe — it offers zero protection until you place your assets inside. The legal fees are an investment in ensuring the safe is built correctly and you know exactly how to fill it.

The All-Important Process of Funding Your Trust

Signing the trust document is just the first step. For the trust to work, you must formally transfer ownership of your assets into its name. This is called funding the trust, and it is where many people falter without professional guidance.

The process involves changing the legal titles on your assets. For example:

- Real Estate: You will sign a new deed to transfer your home from your individual name to the trust's name.

- Bank Accounts: You will need to work with your bank to retitle your checking, savings, and brokerage accounts into the trust's name.

- Other Assets: This could include business interests, valuable personal property, and non-retirement investment accounts.

An experienced estate planning attorney will guide you through every step, ensuring each asset is transferred correctly. Skipping this phase or doing it improperly is a massive mistake that can send your assets directly to probate court, defeating one of the main reasons for creating the trust. This meticulous work is a crucial part of what you are paying for and is essential for your peace of mind.

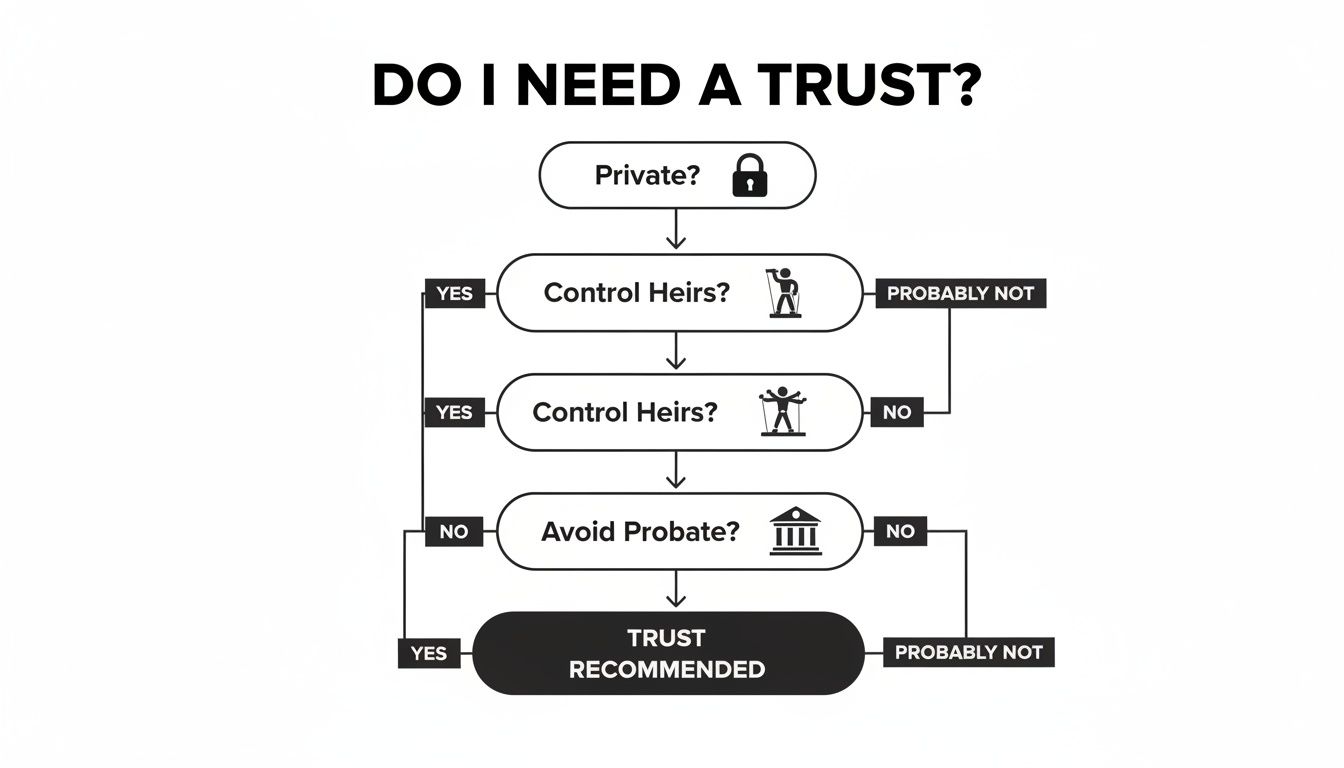

Making the Decision and Finding the Right Help

So, how do you decide if a trust is right for you? It comes down to weighing your goals for privacy, asset control, and family protection against the realities of your estate. It’s about what you want your legacy to do.

A few direct questions can help point you in the right direction.

This decision tree provides a quick visual guide. Notice how answering "yes" to questions about privacy, controlling inheritances, and avoiding probate consistently leads toward needing a trust.

As you can see, the more you want to dictate the terms of your legacy and keep your financial life out of the public record, the stronger the case for a trust becomes.

Questions to Guide Your Decision

If you’re still uncertain, consider this checklist. A "yes" to any of these questions is a strong signal that you should have a serious conversation about creating a trust.

- Is keeping my estate private a top priority? Remember, a will is a public document; a trust is not.

- Do I want to control how and when my heirs receive their inheritance? A trust lets you set rules, like distributing funds when they reach a certain age or meet a specific milestone.

- Do I own property in more than one state? A trust can help your family avoid the costly and frustrating process of ancillary probate in multiple states.

- Do I have a blended family? With a trust, you can ensure both your current spouse and children from a previous relationship are provided for exactly as you intend.

- Is planning for my potential incapacity important to me? A living trust allows your chosen successor trustee to manage your affairs without court intervention.

Finding a Qualified Estate Planning Attorney

While the internet is full of DIY trust services, this is one area where you should not cut corners. The legal details are unforgiving. A small mistake in how the document is written or how the trust is funded can invalidate the entire structure, costing your family far more in legal battles than you ever saved.

That’s why the expertise of a qualified estate planning attorney is so valuable.

Finding the right professional is critical. Look for an attorney who specializes specifically in estate planning — not a generalist. A true specialist brings a depth of knowledge that’s essential for building a trust that works under pressure and achieves your long-term goals.

The right attorney does more than draft documents; they act as a strategic partner, helping you build a comprehensive plan that protects your assets and secures your legacy for generations.

A great place to start is by asking for referrals from trusted advisors, like the team here at Commons Capital, or from friends who have already gone through this process. When you vet potential attorneys, check their credentials with your state's bar association and look up client reviews.

During your first meeting, ask about their experience with situations like yours. A good attorney will spend most of the time listening to your goals before suggesting a specific strategy.

A Few Common Questions About Trusts

When you start digging into the world of estate planning, a lot of questions naturally pop up. Let's tackle some of the most common ones we hear when people are trying to figure out if a trust is the right move for them.

Can I Be the Trustee of My Own Revocable Living Trust?

Yes, absolutely. In fact, most people who establish a revocable living trust name themselves as the initial trustee. This is a standard setup that allows you to maintain full, uninterrupted control over all your assets while you are alive.

You can buy, sell, and manage the assets held by the trust just as you always have. The key is that you will also name a successor trustee. This is the person who steps in to manage things if you become incapacitated and who handles distributing the assets to your heirs after you pass away — all without a judge or a courtroom in sight.

Does Putting My House in a Trust Affect My Mortgage?

For the most part, no. A federal law called the Garn-St Germain Act protects homeowners in this situation. When you transfer your primary residence into a revocable living trust, your lender cannot trigger the "due-on-sale" clause and demand immediate loan repayment.

It also typically won't trigger a reassessment of your property taxes or affect your homestead exemption in most states. However, it's always wise to notify your mortgage company and consult with your local tax assessor to be sure.

What Happens If I Forget to Fund an Asset into My Trust?

This is a huge, and surprisingly common, mistake. Think of your trust document as an empty, high-tech vault. It’s useless until you actually put your assets inside it. If you create the trust but don't formally transfer the legal title of your assets — a process called funding — the trust has no power.

Any assets left out of the trust will likely have to go through the public probate process, which is often the very thing you were trying to avoid. Making sure your trust is properly and completely funded is the last, crucial step that makes the whole strategy work.

Forgetting to fund your trust is like building a state-of-the-art security system but never turning it on. The structure is there, but it offers no real protection for the assets left outside.

Navigating these details is where having the right team makes all the difference. At Commons Capital, we work alongside you and your legal advisors to make sure your financial strategy and your estate plan are perfectly in sync. We're here to provide the clarity and confidence you need to secure your legacy.

Learn more about our private wealth management services.