For many business owners in Boston, selling your company is the most significant financial event of your life. It's the culmination of years, or even decades, of hard work, risk, and sacrifice. Proper wealth management for business owners in Boston isn't just about what you do after the sale; it begins years before you even think about listing your business. Strategic pre-sale planning can dramatically increase your final take-home value and ensure a smooth transition into your next chapter.

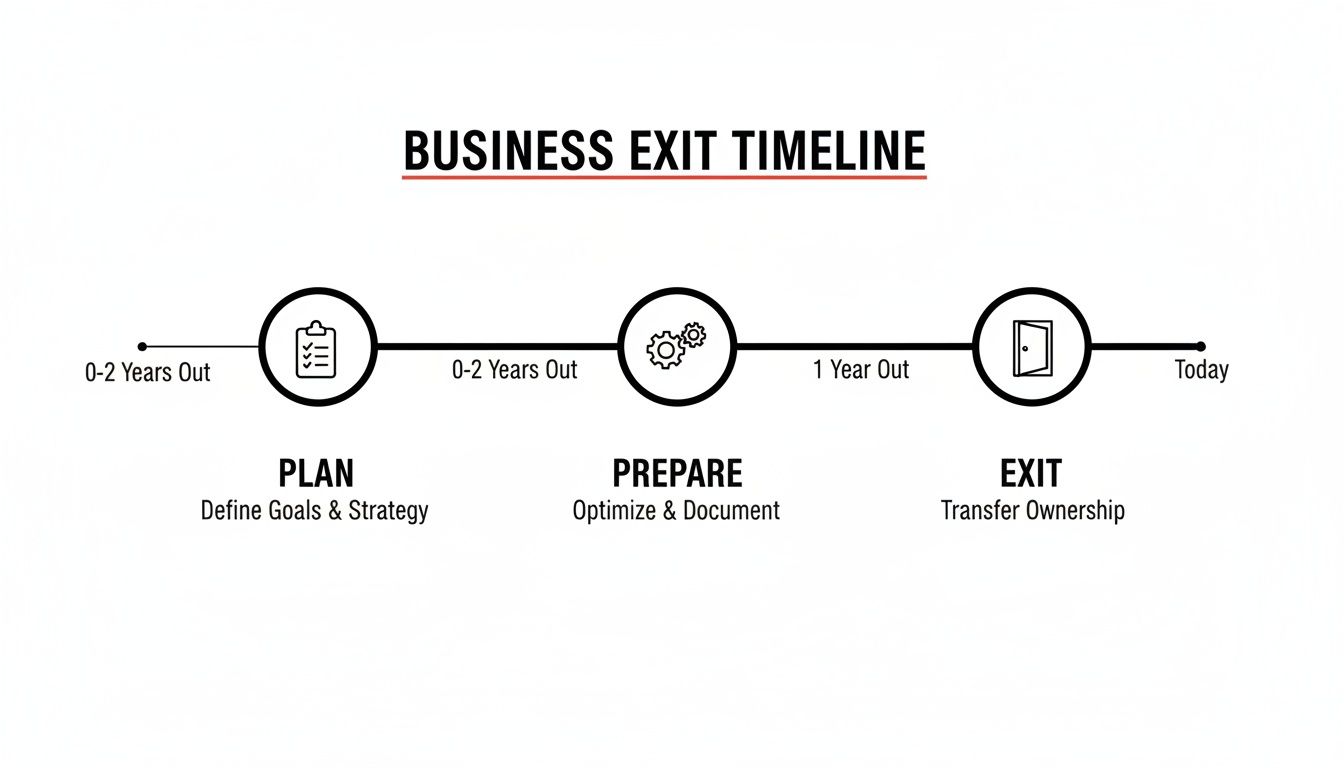

1. Pre-Sale Wealth Planning: What to Do 2-3 Years Before

The most successful business sales don't happen by accident. They are the result of meticulous preparation that starts long before a "for sale" sign ever goes up. To maximize your company's value and prepare for the massive liquidity event ahead, you need a 2-3 year runway. This is where a financial advisor for a business exit in Boston becomes a critical partner.

Your first step is to assemble a dedicated "exit team." This team should include:

- A Wealth Advisor: To integrate the business sale with your personal financial goals, estate plan, and tax strategy.

- A CPA/Tax Advisor: To clean up your financials and structure the sale for maximum tax efficiency.

- An M&A Attorney: To handle the legal complexities of the transaction.

- An Investment Banker or Business Broker: To find qualified buyers and negotiate the best possible price.

With your team in place, the focus shifts to "house cleaning." This involves getting your business in perfect shape for a buyer's scrutiny. Key actions include:

- Cleaning Up Financials: Move toward audited or reviewed financial statements. A buyer needs to trust your numbers completely.

- Reducing Customer Concentration: If a single client represents a large portion of your revenue, a buyer will see that as a major risk. Focus on diversifying your client base.

- Strengthening Your Management Team: A business that can run without you is far more valuable. Empower your key employees and ensure they are prepared to stay through a transition.

- Documenting Processes: Formalize your operations, from sales funnels to production workflows. This shows a buyer a well-oiled machine, not a business dependent on your tribal knowledge.

Planning your exit 2-3 years in advance is the difference between simply selling your business and maximizing its value. It transforms a potentially stressful event into a controlled, strategic wealth creation opportunity.

This preparatory phase is also the time to begin personal financial modeling. A wealth advisor can help you answer the most important question: "What's my number?" By understanding your post-exit lifestyle goals, you can determine the net sale price you need to achieve complete financial independence.

2. Tax Strategies for a Business Sale

It's not what you make; it's what you keep. This old adage is never truer than in a business sale. Without careful planning, federal and Massachusetts state taxes can take a massive bite out of your proceeds. The right tax strategy, implemented well before the sale, is a cornerstone of effective financial planning for a business sale liquidity event.

The structure of your sale has enormous tax implications. The two primary structures are an asset sale and a stock sale.

- Asset Sale: The buyer purchases specific assets of the company (e.g., equipment, customer lists, intellectual property). This is often preferred by buyers because it allows them to get a "step-up" in basis on the assets for future depreciation, reducing their tax burden. For the seller, this can result in a higher tax bill as gains on certain assets are taxed at ordinary income rates.

- Stock Sale: The buyer purchases the owner's shares in the corporation. This is generally preferred by sellers as the entire gain is typically treated as a long-term capital gain, which is taxed at a lower rate.

Negotiating a stock sale is often a key goal for the seller's team. Another powerful tool, especially for C-Corporations, is the Qualified Small Business Stock (QSBS) exclusion. If your company's stock qualifies under Section 1202 of the tax code, you may be able to exclude up to 100% of the capital gains from federal tax, up to $10 million or 10 times your basis. This is a game-changing provision that requires planning years in advance to ensure compliance.

Other pre-sale tax planning strategies include:

- Shifting to a Tax-Friendly State: For some owners, establishing residency in a state with no income tax (like Florida or New Hampshire) before the sale can yield significant savings, though this requires careful planning to meet legal residency requirements.

- Charitable Remainder Trusts (CRTs): By contributing a portion of your company stock to a CRT before the sale, you can defer capital gains tax, receive an immediate charitable deduction, and create an income stream for yourself.

- Timing the Sale: Pushing a sale into the next calendar year can defer the tax liability, giving your capital more time to grow before taxes are due.

3. What to Do with a Large Sum After the Sale

The wire transfer hits your account. For the first time, you are liquid, holding a sum of money larger than you've ever managed personally. This moment is exhilarating but also perilous. The period immediately following a liquidity event is when people are most vulnerable to making poor financial decisions. This is where a sudden wealth planning advisor becomes indispensable.

The first rule is: Don't make any sudden moves. Resist the urge to immediately buy a new house, fund a relative's business, or jump into a speculative investment. Your initial goal is capital preservation.

Here's a step-by-step plan for the first 6-12 months:

- Park the Cash: Place the proceeds in safe, liquid accounts like high-yield savings or short-term Treasury bills. The goal is not high returns; it's stability and access while you plan.

- Assemble Your "Life After" Team: This team, led by your wealth advisor, will include an estate planning attorney and a CPA. Together, they will build a comprehensive financial plan.

- Define Your Goals: What do you want this money to do for you and your family? Fund retirement? Start a new venture? Philanthropy? Your goals will dictate the investment strategy.

- Build a Diversified Portfolio: Your wealth advisor will design a globally diversified portfolio of stocks and bonds tailored to your risk tolerance and income needs. This is the engine that will preserve and grow your wealth for decades to come.

Managing sudden wealth is as much about psychology as it is about finance. It’s crucial to create a structured "decision-making framework" with your advisor to evaluate new opportunities and requests for money, protecting you from emotional choices.

4. Transitioning from Business Owner to Investor

For years, your identity and your wealth were tied to one asset: your business. You were an active operator, making daily decisions to drive growth. After the sale, your role fundamentally changes. You are no longer an operator; you are an investor. This mental shift is one of the biggest challenges for newly liquid entrepreneurs.

As a business owner, you were comfortable with concentrated risk. You bet on yourself, and it paid off. As an investor, the primary goal shifts from high growth to wealth preservation and diversification. Your new job is to manage your portfolio, not a company.

Key principles for the new investor mindset include:

- Embrace Diversification: Your wealth should now be spread across hundreds or thousands of companies, industries, and geographies through a well-constructed portfolio. The days of having all your eggs in one basket are over.

- Understand Risk and Return: Work with your advisor to define your risk tolerance. An appropriate asset allocation will be designed to meet your growth needs without exposing you to unnecessary volatility.

- Think Long-Term: Resist the temptation to check your portfolio daily or react to market noise. Your new plan is designed for decades, not days.

- Separate "Play" from "Core": If you want to invest in startups or other private ventures, allocate a small, specific percentage of your portfolio to these higher-risk assets. The vast majority of your wealth should remain in your core, diversified strategy.

This transition is not just financial; it's personal. Many former owners struggle with a loss of purpose. A good wealth management plan will incorporate your "what's next" goals, whether that's philanthropy, mentoring, travel, or starting a new, less-demanding venture.

5. Estate and Legacy Planning Post-Exit

Selling your business doesn't just change your financial picture; it completely redefines your estate. With significant liquid wealth, your focus must shift to ensuring that wealth is protected and passed on efficiently to the people and causes you care about. Effective wealth management for business owners in Boston must include a sophisticated estate plan.

With a large taxable estate, minimizing estate taxes becomes a top priority. The federal estate tax exemption is high, but it is scheduled to be cut in half at the end of 2025. Furthermore, Massachusetts has its own estate tax with a much lower exemption threshold (currently $2 million).

Your post-exit estate planning checklist should include:

- Updating Your Will and Trusts: Your existing documents are likely obsolete. You will likely need to establish new trusts, such as Revocable Living Trusts, to manage assets and avoid probate.

- Implementing Advanced Gifting Strategies: To reduce the size of your taxable estate, you can use strategies like Grantor Retained Annuity Trusts (GRATs) or make direct gifts to family members utilizing your annual and lifetime gift tax exemptions.

- Establishing Irrevocable Life Insurance Trusts (ILITs): An ILIT can own a life insurance policy outside of your taxable estate, providing immediate, tax-free liquidity for your heirs to pay estate taxes and other expenses.

- Defining Your Philanthropic Legacy: For many, this is the most rewarding part of wealth. You can establish a Donor-Advised Fund (DAF) for simple, tax-efficient giving or create a private foundation for more significant, family-run charitable endeavors.

A well-crafted estate plan is your final act of stewardship. It ensures your life's work creates a lasting legacy of security and opportunity for future generations.

This comprehensive planning transforms the proceeds from your business sale into multi-generational wealth, securing your family's future and cementing your legacy long after the deal is closed.

A comprehensive financial strategy requires expertise. Talk to Commons Capital before your business sale to ensure you are maximizing value and preparing for your next chapter. Learn more by visiting our website.