If you are looking up how to open a trust account, chances are something important just changed. You sold a business. Your compensation jumped. A parent passed assets down. A career in sports or entertainment created a burst of income and a long list of people who now need to be planned for.

At that point, a trust stops being a theoretical estate planning topic. It becomes an operating tool. The right trust can keep assets organized, direct control to the right people, and prevent avoidable friction when wealth moves from one generation to the next. The wrong structure, or a trust that is signed but never properly opened and funded, creates paperwork without protection.

High-net-worth families usually need more than a generic checklist. They need a method that accounts for concentrated stock, private business interests, real estate, privacy concerns, future incapacity, blended-family issues, and in many cases, cross-border exposure. That is where the process becomes nuanced.

Why High-Net-Worth Families Need a Trust

A trust usually enters the conversation after a success event or a stress event. A liquidity event brings new cash and complexity. A family transition raises questions about who should control assets. A public-facing client starts thinking less about yield and more about privacy, continuity, and reducing the chance that a court becomes involved in family finances.

For affluent families, a trust is rarely just about passing assets at death. It is about control during life and continuity after it. A well-structured trust can define who makes decisions if the grantor becomes incapacitated, how children or future generations receive assets, and how investment accounts, real estate, and business interests are administered without unnecessary delay.

Probate avoidance matters here because delay and exposure matter. Tax planning matters because family wealth is often spread across multiple asset types and multiple jurisdictions. If you are sorting through broader estate questions, this overview on understanding inheritance tax is a useful companion to the trust planning discussion.

A trust also forces a family to make decisions they often postpone:

- Who should act with fiduciary responsibility

- Which assets belong inside the trust

- Whether control or protection matters more

- How distributions should work for children, spouses, or future heirs

- What happens if a trustee cannot serve

For many families, the first practical question is not whether they need a trust. It is which kind. If you are still deciding, this Commons Capital article on whether do I need a trust is a useful starting point before opening the account itself.

Choosing Your Foundational Trust Structure

The initial structural decision is structural. Before any bank or brokerage paperwork is completed, the grantor needs to choose the trust form that matches the family’s goals.

Most high-net-worth clients are deciding between a revocable living trust and an irrevocable trust. Both can hold assets. Both can be used to create a formal trust account. They do very different jobs.

The practical difference

A revocable living trust works best when the primary goals are continuity, simplified administration, privacy, and probate avoidance. The grantor usually keeps control, can amend the trust, and often serves as the initial trustee.

An irrevocable trust is the better choice when the family needs stronger separation between the grantor and the assets. That often matters for asset protection planning, advanced estate planning, or situations where the grantor wants to place boundaries around future use of wealth.

The trade-off is simple. Revocable trusts preserve control. Irrevocable trusts can create more protection, but they demand more discipline.

Revocable vs. Irrevocable Trust Comparison for HNWIs

What works well in practice

A revocable trust often works well for a business owner who wants successor management in place, wants personal accounts and real estate titled correctly, and wants family administration to stay out of court.

An irrevocable trust is often more suitable for a public figure, family office, or client with creditor concerns, concentrated wealth, or a deliberate plan to move appreciating assets outside the grantor’s direct estate. That is also where trustee selection becomes more sensitive, because the person or institution in control must function well under pressure.

Practical rule: If the client still wants to move assets in and out casually, rewrite terms freely, and remain the unquestioned decision-maker, a revocable structure is usually the more honest fit.

Other trust structures that matter

High-net-worth planning does not stop at the revocable versus irrevocable decision.

A discretionary trust can be useful when the grantor wants a trustee to have judgment over when and how beneficiaries receive funds. That matters when heirs are young, financially inexperienced, exposed to divorce risk, or likely to face creditor pressure.

A special needs trust may be essential if a beneficiary requires support that must be coordinated carefully with benefit eligibility and long-term care planning.

Some families also divide roles across multiple trusts rather than forcing one document to do everything. That can be cleaner than overloading a single trust with incompatible goals.

For readers comparing legal starting points, this overview of Wills Trusts can help frame how trust planning differs from a will-based plan.

International families need a different lens

According to the STEP 2025 survey, many international high-net-worth individuals face confusion over cross-border trust setups, and many delay because foreign bank requirements are unclear. The same source notes that EU DAC8 is effective in 2026 and mandates enhanced digital reporting for trusts (Estatementors).

That matters because a trust that works cleanly in one jurisdiction can become burdensome in another. If the family has UK, EU, or Asian ties, account-opening strategy should be reviewed alongside tax counsel and local legal counsel before documents are signed.

If you are weighing the control-versus-protection trade-off more closely, Commons Capital’s discussion of irrevocable trust pros and cons is a useful next read.

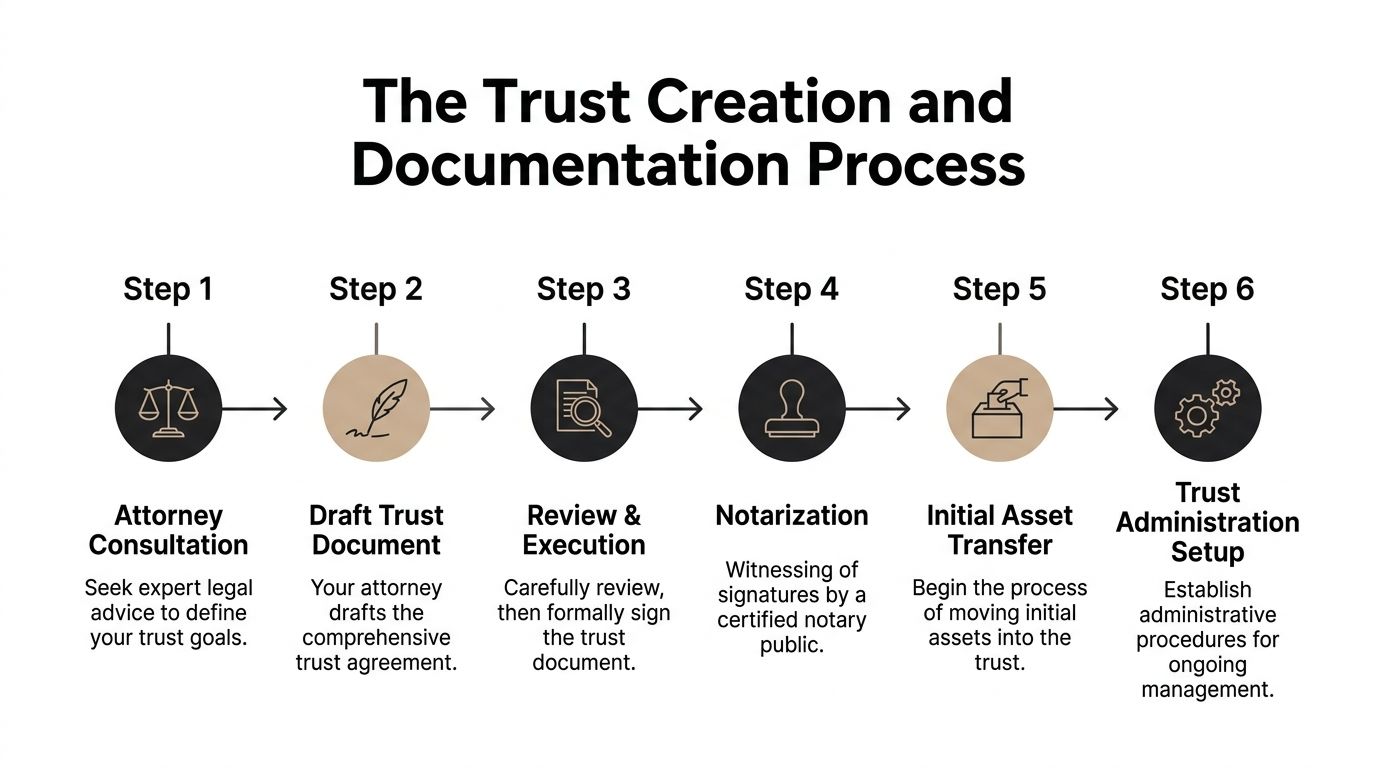

The Trust Creation and Documentation Process

Opening the account starts long before the custodian sees an application. The legal file has to be right first. Most failed openings are not caused by the bank. They are caused by incomplete trust preparation.

Start with the trust agreement

The trust agreement is not a formality. It is the document the institution will rely on to determine who has authority, what type of trust it is, and whether the account can be opened as requested.

For high-net-worth clients, the drafting stage should address more than boilerplate provisions. The trust should clearly state:

- Trust identity including the formal trust name and date

- Trustee authority including whether one trustee can act alone or whether joint signatures are required

- Successor trustee provisions so authority transfers cleanly if a trustee dies, resigns, or becomes incapacitated

- Asset-specific language for business interests, investment accounts, intellectual property, or family real estate

- Distribution standards especially if beneficiaries should receive assets at certain ages, upon milestones, or at trustee discretion

A bank operations team does not want to interpret ambiguous legal language. If authority is unclear, the application stalls.

Obtain the correct taxpayer identification

This is one of the most common failure points.

For irrevocable trusts, 40% to 50% of initial applications fail because the trust is missing an Employer Identification Number, since the trust must have a separate TIN from the trustees. The same Fidelity guidance states that success rates exceed 95% with attorney preparation, versus 60% for DIY setups (Fidelity trust account guidance).

That gap reflects a simple truth. The technical details matter.

A revocable trust may initially use the grantor’s Social Security number in some circumstances. An irrevocable trust typically needs its own EIN. If the wrong identifier is used, institutions pause the file, request corrections, and sometimes restart the process entirely.

Tip: Before submitting anything, confirm whether the trust is treated as revocable or irrevocable for account-opening purposes, and make sure the tax ID matches that legal status.

Build a clean documentation packet

Families often think the full trust agreement is all they need. In practice, institutions usually want a tighter packet that lets their compliance and new-account teams review authority quickly.

That packet commonly includes:

- Certified trust agreement or certification of trust

This gives the institution confirmation that the trust exists and identifies core terms without always requiring the full document. - Trustee identification

Government-issued identification for each acting trustee is standard. - Proof of authority

If a successor trustee is acting, the institution may want resignation documents, death certificates, or affidavits tied to the transition. - Signature pages

Many delays happen because execution pages are missing, outdated, or do not match the current acting trustees. - Tax identification support

For irrevocable trusts, that usually means EIN confirmation tied to the trust name.

Match the paperwork to the institution

Here, theory meets practice. Brokerages, private banks, and retail banks all review trust files differently.

Vanguard’s process for certain trust account openings includes an online flow built around trust name, trust date, trustee names, and signature pages. Fidelity also supports trust account workflows, but requirements and acceptable documentation can vary by trust type and asset type. A local bank may accept a certification of trust for a deposit account but require more review if the trust will hold large cash balances or multiple trustees.

The practical mistake is sending the same packet everywhere and assuming all institutions will process it the same way. They will not.

Review execution details carefully

A strong trust can still fail operationally if the document was not signed correctly or if state law formalities were not observed. Signature defects, incomplete notarization, and missing trustee acceptance language can all create avoidable delays.

For HNW families, I usually want the legal team and the wealth team aligned before opening begins. That is especially true when the trust will hold closely held business interests, private investment vehicles, or assets with transfer restrictions. The account-opening form is the end of the process, not the beginning.

Selecting the Right Trustee and Custodian

The trust document answers one legal question. The trustee and custodian answer the operational one. Who is going to carry this out well?

That decision shapes everything from distributions to reporting discipline to family conflict management. In many affluent families, the wrong trustee causes more trouble than the wrong investment allocation.

Individual trustee

A family member or trusted friend may know the beneficiaries well and understand the family’s history. That familiarity can be a real advantage, especially when the trust is intended to reflect family values rather than purely mechanical distribution rules.

It can also create problems.

An individual trustee may struggle with:

- Impartiality when siblings or blended-family beneficiaries disagree

- Administrative burden if the trust holds multiple account types or real estate

- Longevity if the trust is expected to last for many years

- Technical competence with tax filings, recordkeeping, and institution-specific requirements

This choice works best when the trust is relatively straightforward and the proposed trustee is organized, financially literate, and emotionally steady.

Corporate trustee

A corporate trustee brings process, continuity, and formal fiduciary oversight. For complex trusts, that often matters more than personal familiarity.

A corporate trustee is usually the stronger fit when the trust must manage substantial investable assets, make recurring beneficiary decisions, coordinate tax professionals, or act for many years across generations. Public-facing clients also benefit from institutional professionalism because emotionally difficult requests are handled through policy rather than family pressure.

The trade-off is style. Corporate trustees can feel less personal, less flexible, and more deliberate in timing.

Bank or brokerage trust platform

Sometimes the best answer is not a full corporate trustee mandate. It is a bank or brokerage relationship that serves as the trust custodian while an individual trustee retains authority. That can work well when the family wants investment custody and reporting at a recognized institution, but does not want to hand full discretionary administration to a corporate fiduciary.

This model often breaks down when the trustee is not prepared for the compliance burden. Digital convenience does not eliminate fiduciary responsibility.

Many U.S. HNWI under 50 prefer online trust setups, yet relatively few succeed for irrevocable trusts because of verification hurdles. Emerging FINRA rules expected in Q1 2026 would require blockchain-verified trustee authentication, with the goal of reducing fraud (Vanguard trust accounts).

A decision framework that works

Ask four questions before naming the trustee:

Key takeaway: Choose a trustee for capability, not sentiment. If the trust will hold meaningful wealth, the role is a job with legal duties, not an honorific.

For sports and entertainment clients, trustee choice deserves even more scrutiny. Income can be irregular, public exposure is higher, and asset types may include royalty streams, image rights, LLC interests, and rapidly changing liquidity needs. In those cases, experience and administrative discipline usually outweigh family familiarity.

Funding Your Trust and Transferring Assets

A trust that is signed but unfunded is mostly an empty shell. Families often believe the legal work is the hard part. In practice, the primary work begins when assets need to move.

Industry benchmarks show that 35% of trusts remain unfunded or partially funded, which negates their ability to avoid probate. Fully funded trusts have a 98% success rate in bypassing probate, which can consume 4% to 7% of an estate’s value (FreeWill trust funding guide).

That single issue explains why so many otherwise good plans underperform.

Cash and bank accounts

The cleanest asset to move is usually cash. Once the trust account exists, cash can be transferred into the account held in the trust’s legal name.

For larger cash positions, deposit insurance matters. The FDIC insures trust accounts using the formula number of owners × number of beneficiaries × $250,000, capped at $1,250,000 per owner. A single owner with five or more beneficiaries qualifies for the maximum $1,250,000 coverage per insured bank (FDIC trust account rules).

That means cash management inside a trust should be intentional. If the family holds large balances, account titling and bank concentration need to be reviewed instead of assumed.

Brokerage accounts and marketable securities

Brokerage assets are often mishandled because families assume beneficiary designations and trust ownership are interchangeable. They are not.

The institution typically requires trust documents, trustee identification, and transfer forms to retitle the account into the trust’s name or to open a new trust account and transfer positions into it. If there are multiple trustees, all required signatures must be collected exactly as the custodian requires.

What works best is consistency. Keep the trust name identical across legal documents, tax identification records, and account-opening forms. Minor naming mismatches can create weeks of follow-up.

Real estate

Real estate transfer is where many families discover that funding is legal work, not just account administration.

The property must usually be retitled by deed into the trust, and the deed must be properly prepared, signed, and recorded. If the property is mortgaged, the family should review lender issues before recording. If there are multiple properties in different states, each one should be handled with local legal guidance.

A signed trust does not pull real estate in automatically. The deed does the work.

Business interests and private entities

Affluent families often need the most coordination here.

If the trust will hold an LLC interest, limited partnership interest, or shares in a closely held business, review the governing documents first. Operating agreements, shareholder agreements, and buy-sell provisions may restrict transfers or require approvals.

The sequence matters:

- Confirm transfer restrictions in entity documents

- Coordinate with legal counsel on assignment documents

- Update ownership records and internal ledgers

- Ensure the trust is reflected consistently across legal and tax records

Trying to force a transfer before checking transfer restrictions is one of the most common errors in complex estates.

Special assets

Art, collectibles, intellectual property, royalty rights, and digital assets all need specific treatment. A trust can own them, but ownership has to be documented in the way that the asset class requires.

For clients in entertainment, this can include contracts, residual streams, naming rights, or image-related entities. For entrepreneurs, it may include patents, trademarks, or founder equity subject to restrictions. For family offices, it may include vehicles held in special-purpose entities.

Tip: If an asset requires its own title system, registry, transfer ledger, or contractual consent, assume the trust is not funded until that record is updated.

What does not work

Several patterns fail repeatedly:

- Signing the trust and stopping there

- Moving only one bank account and leaving the rest untouched

- Assuming a will “catches” everything cleanly

- Ignoring deeds, private investments, or legacy brokerage accounts

- Forgetting to update new assets acquired after the trust is created

The families who handle funding well usually maintain a live asset checklist and revisit it after each major purchase, sale, or business change.

Post-Opening Administration and Best Practices

Opening the trust account is the start of administration, not the end of planning. A trust only stays effective if the trustees operate it with discipline.

Keep records like a fiduciary

Trustees should maintain complete records of contributions, transfers, expenses, investment activity, and distributions. For affluent families, that often means centralizing statements, legal documents, and trustee actions in a format that can be reviewed quickly by tax advisors and successor fiduciaries.

That recordkeeping becomes more important when a trust owns multiple entities or makes discretionary distributions. Good records reduce conflict because they show exactly what happened and why.

Handle tax reporting correctly

Irrevocable trusts generally require their own tax administration. That often includes annual filing obligations and coordination with the trust’s CPA.

For readers looking more closely at the tax side, this Commons Capital article on taxes on a trust is a useful companion.

Review cash exposure and institution concentration

Trustees should also review where trust cash is held. The FDIC coverage formula for trust accounts involves the number of owners, beneficiaries, and a specific dollar amount, with a per-owner cap, which is a useful planning tool when structuring insured cash positions. A single owner with multiple beneficiaries can qualify for substantial coverage per insured bank.

That matters for trusts holding sale proceeds, reserve cash, or pending distributions. Cash safety is part of administration, not an afterthought.

Revisit the trust after major events

The trust should be reviewed after family changes, liquidity events, trustee changes, major real estate transactions, business restructurings, or changes in residence. A trust that was perfectly drafted years ago can become mismatched to the family’s current reality.

The best-administered trusts are reviewed periodically by legal, tax, and advisory teams together. That is how families avoid stale documents, incomplete funding, and operational surprises.

Frequently Asked Questions About Trust Accounts

Can I open a trust account before I transfer assets into the trust

Yes. In many cases, the account is opened first so there is a properly titled destination for incoming cash or securities. But the legal effect of the trust still depends on actual funding. Opening the account alone does not complete the plan.

Do I need a separate trust account for every asset

No. A trust can own many types of assets, and not every asset sits inside a bank account. The better question is whether each asset has been properly retitled, assigned, or recorded in the trust’s name where applicable.

Is a family member always the best trustee

Not necessarily. A family member may know the people involved, but that does not mean they can administer a complex trust well. For larger or more complicated estates, professional or institutional help is often the stronger choice.

Can a trust account hold investment assets and cash

Yes. Families commonly use trust structures for deposit accounts, brokerage accounts, and the proceeds from asset sales. The institution and trust terms will determine how the account is opened and administered.

What is the biggest mistake people make when learning how to open a trust account

They focus on signing documents and underestimate funding and administration. Most trust problems come from incomplete transfers, unclear authority, or weak follow-through after the account is opened.

Commons Capital works with high-net-worth individuals, families, family offices, and clients in sports and entertainment who need help structuring and managing complex wealth. If you want guidance on trust setup, trustee coordination, asset transfer strategy, or long-term administration, visit Commons Capital.