How to talk to adult children about wealth in 2026 starts with one uncomfortable fact: 70% of family members struggle to approach wealth conversations. In practice, that means many families delay until a health event, liquidity event, sale, or estate document forces the issue.

That delay is expensive in ways families often miss. It creates confusion about expectations, weakens stewardship, and leaves adult children to fill information gaps with assumptions. In 2026, that approach is even riskier because tax rules, digital assets, and AI-driven visibility have changed what “waiting” costs.

The good news is that reluctance is not the same as resistance. Families can do this well. They just need a better process than one tense dinner conversation and a binder full of documents.

The Seventy-Percent Problem In Wealth Transfer

One number frames the challenge. Roughly 70% of family members find wealth conversations hard to start, as noted earlier. In advisory work, that tracks with what families describe in private. The obstacle is rarely a lack of care. It is the weight of the topic itself.

Parents are trying to protect work ethic, privacy, and family harmony at the same time. Adult children are often trying to ask reasonable questions without sounding as if they are asking for a payout. Siblings bring different histories, different assumptions about fairness, and different levels of financial maturity into the same room. A conversation that looks straightforward on paper can feel loaded within minutes.

The gap is not one of willingness

In many families, both generations want the discussion. They just want it handled differently.

Parents often prefer to finalize plans first, then share conclusions in a controlled setting. Adult children usually respond better to a process that gives context early, leaves room for questions, and separates values from dollar amounts. When those preferences collide, each side can misread the other. Parents read silence as avoidance. Children read delay as secrecy.

I see the same pattern across long-term client families. Communication breaks down because the conversation starts too late, starts with the wrong level of detail, or asks people to absorb emotional and financial information all at once.

That matters because transfer planning is never only technical. Documents can direct assets. They do not prepare heirs to handle responsibility, uncertainty, family roles, or future tax decisions. If you are reviewing trusts, gifting strategy, or ways to minimize estate taxes, the family communication plan belongs in the same workstream.

How 2026 Changes the Conversation

The old playbook was privacy first, disclosure later. For many high-net-worth families, that approach now creates more risk than protection.

By 2026, adult children may already have fragments of the story before a parent says a word. They may recognize the scale of a business sale, see property records, notice trust documents, track concentrated stock positions through public filings, or piece together digital asset activity from custody apps, exchange emails, or shared devices. AI adds another layer. It is easier than ever to assemble partial information from ordinary data trails, and partial information usually creates worse conversations than honest preparation.

That changes the standard for good planning. Families need a process that does three things well:

- Start with purpose so the first discussion does not turn into a debate about entitlement.

- Break disclosure into stages so relatives are not asked to process every legal, tax, and emotional issue in one sitting.

- Address 2026 realities directly, including the estate tax sunset, digital asset access, and privacy risks created by AI-assisted visibility.

Families do not need a dramatic reveal. They need a disciplined structure, clear boundaries, and enough candor to keep assumptions from filling the gaps.

Laying the Foundation Before You Speak

Before you schedule a family meeting, write a single email, or mention inheritance over dinner, do the private work first.

Parents often assume the hard part is saying the words out loud. Usually, the harder part is reaching internal alignment. If spouses are not aligned on what the wealth is for, what should stay private, what should be phased in, and what standards matter, the children will feel that split immediately.

Experts at Bernstein and Wescott recommend a values-first approach in which parents spend 30 to 60 minutes documenting their core values and the intended purpose of their wealth before initiating any dialogue. That sounds simple. It's not. But it works because it forces clarity before disclosure.

Start with purpose, not net worth

Families who begin with numbers tend to trigger the wrong conversation first. Adult children naturally jump to questions about access, fairness, control, or future lifestyle. Parents then get defensive because the questions feel transactional.

A better opening framework is to answer these privately before anyone else enters the room:

- What do we want this wealth to do? Security, opportunity, philanthropy, business continuity, family support, or some combination.

- What values must travel with the assets? Work ethic, responsibility, privacy, generosity, stewardship.

- What are we afraid of? Dependency, entitlement, sibling conflict, spouse tension, loss of ambition.

- What is essential? Confidentiality, trust structures, charitable commitments, governance rules, family business boundaries.

A practical parent checklist

Write your answers separately first. Then compare them as a couple or as co-decision-makers.

- Define the intent of the money: Is the wealth meant to provide a safety net, expand opportunities, preserve a family enterprise, fund philanthropy, or all of the above?

- Clarify support philosophy: Under what circumstances will you help with housing, education, healthcare, business ventures, or emergencies?

- Identify timing boundaries: What should be discussed now, later, or only when a legal or life event makes it appropriate?

- Set a language standard: Decide whether you'll speak in broad categories, percentages, structures, or eventually in exact numbers.

- Choose the first message: The first conversation should answer why you're bringing this up now, not reveal everything you know.

Practical rule: If parents can't explain their wealth philosophy in plain language to each other, they are not ready to explain it to their children.

What this preparation prevents

This work reduces the two most common failures. First, it prevents mixed messages, where one parent presents wealth as freedom and the other presents it as a burden. Second, it stops the meeting from turning into an accidental referendum on who deserves what.

A short written statement helps. It doesn't need legal language. One page is enough. It should cover values, intent, tone, and the limits of the first conversation.

Parents who do this groundwork usually enter the first meeting calmer, more consistent, and less likely to over-explain. That matters because children don't just hear content. They read confidence, hesitation, and disagreement.

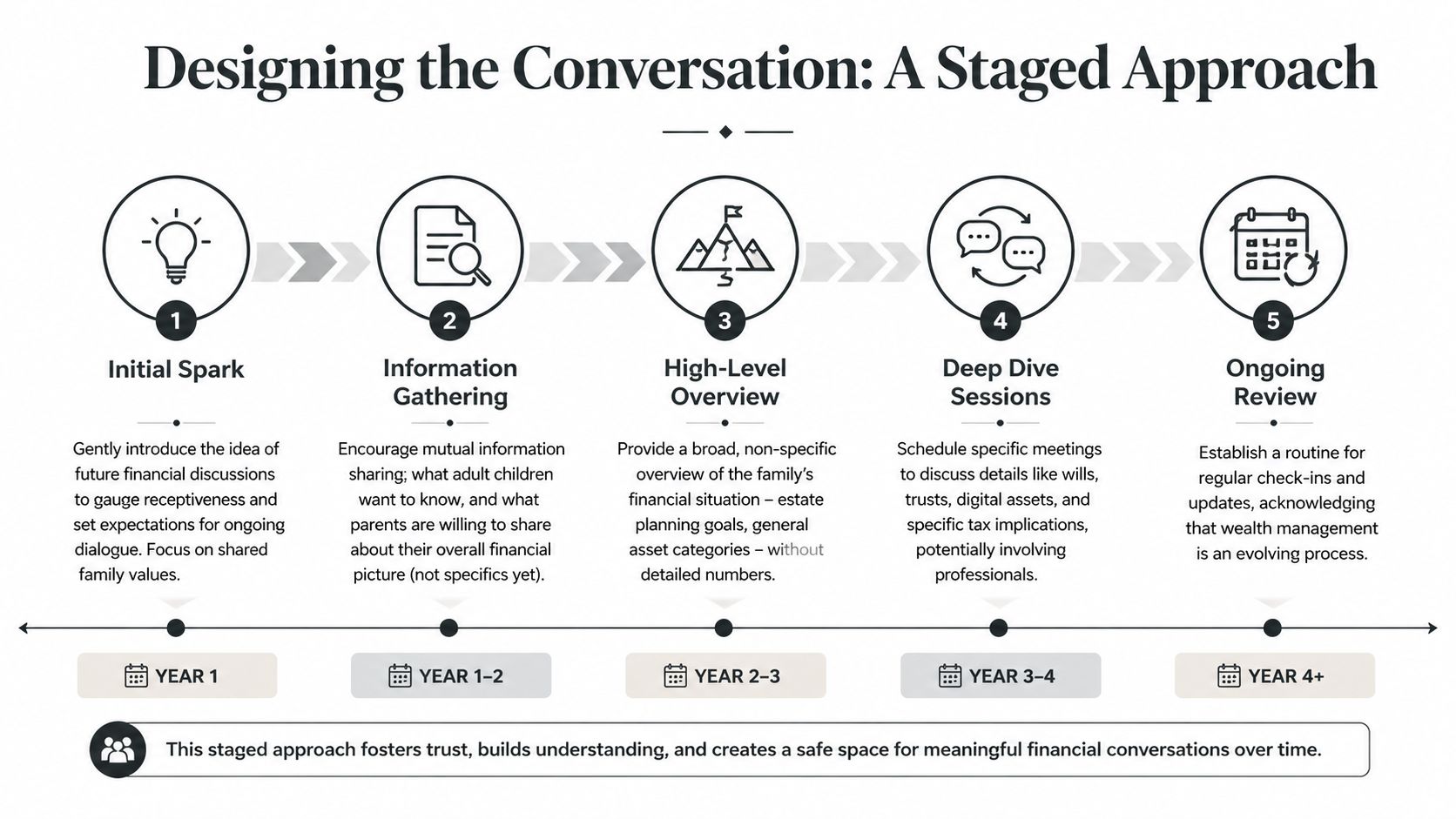

Designing the Conversation A Staged Approach

The biggest mistake wealthy families make is trying to compress years of context into one meeting. Parents have lived with the balance sheet, the business risk, the estate documents, and the trade-offs for decades. Their children have not.

That is why the one-shot disclosure usually fails. According to Transition Strategists, multi-year, facilitated processes result in 80% to 90% family cohesion, while single “big reveal” sit-downs often lead to conflict in 40% to 50% of cases. The key is a phased process that starts with individual discovery before group disclosure.

What works better than the big reveal

A staged approach recognizes that siblings rarely start from the same place. One may be financially knowledgeable and eager. Another may be successful in a career but uncomfortable around investing. A third may be in a divorce, business launch, or geographic move and have limited emotional bandwidth.

Trying to equalize those differences by delivering the same message, at the same depth, on the same day is what creates unnecessary friction.

A stronger design looks like this:

The first family meeting should stay high level

The first group conversation should not attempt to cover every legal entity, trust provision, basis issue, or distribution rule. It should establish a frame.

A useful agenda for that first meeting:

- Why this conversation is happening now

- What the family wants the wealth to support

- What parents hope to preserve beyond money

- How future conversations will work

- What topics will be discussed later with advisors present

- What questions are welcome now

Notice what's not on that list. There is no line item for exact net worth, allocation percentages by child, or a review of every estate document. Those details may matter later. They rarely help first.

Slow is not avoidance. Slow is sequencing.

Design for participation, not performance

Parents often overprepare for these meetings as if they need to deliver a master class. They don't. The first conversation succeeds when children leave feeling included, not overwhelmed.

That means asking questions such as:

- What do you already understand about our planning?

- What concerns you most about family wealth?

- What would help make future conversations useful rather than stressful?

- Do you prefer these conversations as a group, one-on-one, or with written follow-up?

The goal is not to “get through the agenda.” The goal is to begin a process your family can sustain.

Scripts and Strategies for the First Meeting

The first meeting usually turns on tone in the first few minutes. If parents sound evasive, children get suspicious. If parents sound too detailed too quickly, children get overloaded. The useful middle ground is direct, calm, and bounded.

One issue deserves special attention because it creates tension well before inheritance does: ongoing support. A 2026 Wells Fargo study, reported by Morningstar, found that the main driver of financial strain between parents and adult children is not the support itself, but a lack of communication about the terms, including whether support is a gift or a loan, whether repayment is expected, and when it ends.

Opening lines that lower the temperature

A productive first sentence does not sound like a legal memo. It sounds like a parent taking responsibility for clarity.

We want to start having more open conversations about family wealth and support, not because everything needs to be decided now, but because silence creates confusion.

Another useful version:

This isn't a meeting about numbers first. It's a meeting about what we want this wealth to mean, how we think about responsibility, and how we'll communicate better as a family.

If your children have very different personalities, say that out loud:

We know each of you may have different questions and a different comfort level. That's fine. We're not trying to force everyone into the same conversation all at once.

How to answer the question parents fear most

At some point, someone may ask, “So, how much is there?”

Don't dodge it awkwardly. But don't let that question hijack the meeting either.

A clean response sounds like this:

That's an important question, and we will address the financial structure in stages. Today, we want to start with purpose, decision-making, and expectations so the numbers have context when we discuss them.

That answer does three things. It acknowledges the legitimacy of the question, avoids unnecessary secrecy, and protects the pacing of the discussion.

Use precise language around support

When parents help adult children with rent, a down payment, graduate school, childcare, or a business bridge loan, vague language creates resentment later.

Use a simple framework and say it plainly:

- Gift: “This is support with no repayment expected.”

- Loan: “This needs to be repaid, and we'll document the terms.”

- Conditional support: “We'll help if certain conditions are met, and we'll define those conditions now.”

A short written follow-up after the conversation helps more than most families expect. It doesn't need to be adversarial. It just needs to be clear.

A first-meeting checklist

- State the purpose early: Avoid letting the room guess why the meeting was called.

- Invite questions without forcing disclosure: Some adult children process slowly and won't ask much in real time.

- Separate support from inheritance: Current financial help and future estate planning should not blur together.

- End with next steps: Confirm what will happen next, who will be involved, and what topics remain off the table for now.

Families often think they need eloquence. They need clarity more.

Navigating 2026 Legal Tax and Digital Asset Hurdles

Wealth conversations in 2026 aren't just emotional. They are technical. If parents talk about legacy without addressing tax law, digital property, and online visibility, the conversation is incomplete.

One emerging issue is that your children may already have an imperfect picture of family wealth before you say a word. A 2025 PwC survey and UBS reporting, summarized by WealthManagement.com, found that 45% of adult children already infer family wealth via online tools, while crypto holdings are up 25% among high-profile individuals. That combination creates privacy risk and disclosure complexity, especially for families with concentrated business interests, public profiles, or digital assets.

Tax law now belongs in the family conversation

Many high-net-worth families still treat tax planning as something only advisors need to discuss. That's no longer enough. If estate tax rules are changing, if trust strategy is being updated, or if gifting is part of the plan, adult children need a plain-English explanation of what those decisions are trying to accomplish.

What they don't need is a technical dump. They need orientation:

- Which assets may be transferred during life versus at death

- Why certain structures exist

- Why liquidity matters

- Why tax drag can affect what beneficiaries eventually receive

- Why timing matters if laws change

If family members understand only the outcome and not the reason, they often interpret planning structures as control rather than prudence.

Digital assets require a separate inventory

Digital assets shouldn't be treated as a footnote in the estate binder. Families now hold value in places previous generations never had to manage, including exchange accounts, cold storage wallets, tokenized interests, creator royalties, online businesses, and monetized digital accounts.

A family conversation should identify:

For families with cross-border exposure, even basic educational resources can help frame the issue. If adult children hold or may inherit digital assets tied to international tax obligations, a guide to crypto tax rules for Australians can show how quickly reporting becomes jurisdiction-specific.

AI changes the privacy equation

Parents often assume secrecy preserves stability. In reality, partial secrecy now invites speculation. AI tools, public databases, social media traces, and business press can generate estimates that are wrong but persuasive.

That creates a new job for parents: correcting false narratives before they harden. A useful script is simple:

You may already have impressions about our finances from what you've seen or inferred online. Some of that may be incomplete or inaccurate. We'd rather give you context than let assumptions drive expectations.

Families with meaningful crypto exposure should also make sure heirs understand the practical transfer issues. A plain-language primer on cryptocurrency planning basics can help adult children see that digital wealth is not just an investment topic. It's an estate administration topic too.

Building Financial Literacy and Governance Structures

A successful transfer doesn't happen because heirs eventually see the documents. It happens because they develop judgment.

One of the best ways to build that judgment is to give adult children limited responsibility before they have major responsibility. That may mean managing a modest taxable account, helping review a charitable budget, sitting in on an investment meeting, or participating in a family entity discussion with guardrails.

Use gifts as training, not just transfers

Advisors often recommend using annual exclusion gifts as a testing ground. In observed families cited qualitatively earlier, those gifts can reveal whether a child treats capital as a tool or as disposable spending. The point isn't surveillance. It's learning.

That trial period can show parents things that no résumé reveals:

- Decision quality: Does the child ask good questions before acting?

- Time horizon: Do they think in months or in years?

- Risk tolerance: Can they handle volatility without impulsive changes?

- Coachability: Will they engage with a CPA, attorney, or advisor productively?

If you want a broader framework for this kind of development, family wealth management is a useful lens. It shifts the focus from transfer mechanics to family capability.

Turn values into live exercises

Many parents talk about stewardship but never create a venue to practice it. That's why philanthropy often works so well as an educational tool. A donor-advised fund, family giving discussion, or shared review of charitable priorities teaches values in action.

Use real questions, not abstract speeches:

- Which causes fit our family values?

- How do we evaluate impact?

- Should giving be anonymous or public?

- Who researches opportunities and presents recommendations?

These are wealth conversations, but they don't feel like inheritance negotiations. That's exactly why they're effective.

Financial literacy grows faster when adult children have a defined role, a bounded amount of responsibility, and room to explain their reasoning.

Build a governance rhythm

Families with complexity need structure. That does not mean creating a miniature corporation unless the family needs one. It means agreeing on how decisions get discussed, who attends which meetings, and what belongs in writing.

A basic governance framework might include:

- A family meeting cadence: Annual or semiannual, depending on complexity

- Topic separation: Investments, philanthropy, family support, and legal updates should not all blur together

- Defined participation: Not every child needs the same role at the same time

- Document discipline: Meeting notes, action items, and follow-up questions should be captured

Governance sounds formal. In practice, it reduces emotional noise. People argue less when they know where decisions belong.

Sustaining Momentum and Resolving Conflict

The first good conversation buys you trust. It does not buy you permanence. Families stay aligned because they normalize communication over time.

That means scheduling future discussions before tension reappears. If meetings only happen during illness, market stress, divorce, sale negotiations, or estate updates, the family will associate money talks with crisis. A recurring cadence changes that pattern.

Set a repeatable meeting structure

A “state of the family” meeting works well when it is predictable and modest in scope. Keep it focused. Not every meeting needs every advisor or every document.

A practical annual agenda might include:

- Values and priorities review

- Major family changes since the last meeting

- High-level planning updates

- Education topic for this year

- Questions about roles, responsibilities, or support

- What needs a separate follow-up meeting

Some families also benefit from short check-ins between larger gatherings, especially when trusts are being revised, a business is being sold, or younger adult children are gradually entering the conversation.

Know when to bring in a neutral facilitator

Conflict in these meetings is rarely just about money. It often reflects old family roles. The responsible child feels overburdened. The independent child hears judgment. A spouse feels excluded. A parent slides into lecturing because anxiety takes over.

That's when an outside facilitator can help. Not because the family is failing, but because neutral process management makes it easier for everyone to stay in their actual role.

A facilitator is especially helpful when:

- Siblings interpret fairness differently

- One child dominates the room

- Parents cannot agree on what to disclose

- Spouses need a clearer boundary

- Support issues are bleeding into inheritance issues

A facilitator should slow the conversation down, not accelerate it.

What to do after a hard meeting

Don't try to solve every disagreement in the room. Capture the issue, define the next step, and separate emotional reaction from planning action.

Use a simple reset process:

- Summarize what was agreed: Put it in writing while it's fresh.

- Name unresolved items clearly: Avoid vague “we'll revisit this later” language.

- Assign ownership: Someone should be responsible for legal follow-up, tax review, or scheduling.

- Preserve the relationship: End with what remains shared, not only what remains disputed.

Families often assume conflict means the process is going badly. Often it means the family is finally discussing what was previously left unsaid. The actual risk isn't disagreement. It's drift, silence, and unmanaged assumptions.

Talking to adult children about wealth in 2026 requires more than courage. It requires a process that fits your family, your assets, and the realities of tax law, digital property, and privacy. If you want help designing those conversations thoughtfully, Commons Capital works with high-net-worth families to manage complex planning decisions with clarity, structure, and long-term perspective.