Retirement isn't a single finish line you cross. It's a journey, a new chapter of life that unfolds in distinct phases of retirement, each with its own challenges and opportunities. Understanding these stages is the key to creating a future that isn't just financially secure, but genuinely fulfilling.

It’s about more than just hitting a number in your 401(k); it’s about preparing for the life that comes after work.

Your Roadmap Through the Stages of Retirement

When you start to see retirement as a multi-stage journey, your planning becomes much more intentional. It's not about slamming on the brakes at 65; it's a gradual transition that can span decades. So many people focus entirely on the financial finish line—that magic savings number—but completely overlook the emotional and practical shifts that follow.

A truly successful retirement plan has to address both sides of the coin.

Thinking in phases helps you anticipate what’s coming next. For instance, your spending in the first few years might be higher as you finally take those trips you've been dreaming of. Later on, your focus might shift more toward healthcare costs. Recognizing this rhythm allows you to structure your finances and your life with much more confidence.

The Foundation of a Successful Retirement

A structured approach is your best friend here. Building a solid foundation before you even leave the workforce sets the tone for everything that follows. This prep work is about more than just spreadsheets; it’s about gaining clarity and finding your direction for the years ahead.

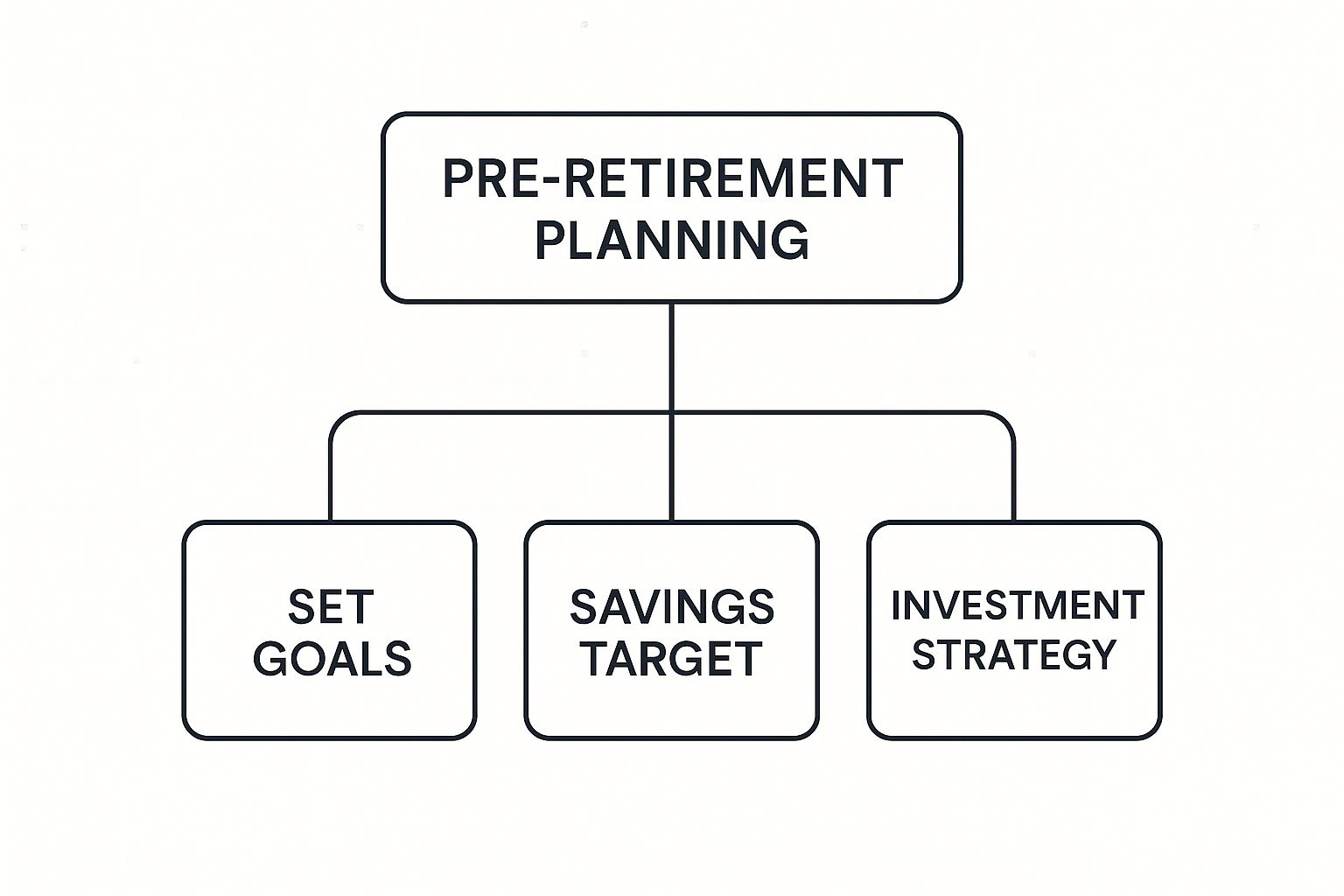

The visual below really breaks down the core components of smart pre-retirement planning.

What I love about this hierarchy is that it shows how a clear investment strategy and a specific savings target are built upon the most important thing: your personal goals. This framework ensures your financial moves are always tied to the life you actually want to live.

Successful retirement planning isn't just about accumulating assets; it's about designing a life. By breaking the journey into manageable phases, you can address the unique challenges and opportunities of each stage with confidence and purpose.

This guide will walk you through each of these critical stages. We'll dive into the insights and actionable steps you need to prepare for a rich, rewarding life after your career.

Preparing For Liftoff in Pre-Retirement

The final 5 to 10 years of your career are the launchpad for your retirement. This critical "pre-retirement" phase is where the game changes—you shift from simply accumulating wealth to strategically designing your future income streams. It's time to swap abstract goals for concrete numbers, stress-test your financial plan, and make the big decisions that will define the next chapter.

Think of it as the final pre-flight check before a long journey. Every single detail matters. This is the moment to maximize those last few years of savings and create a retirement budget that actually reflects the lifestyle you’ve been dreaming of. This is where meticulous planning truly pays off.

This runway is also getting longer for many people. Between 2002 and 2022, the average age people left the workforce in OECD countries went up by 3.1 years for women and 2.6 years for men. That extended timeline offers a valuable window for last-minute financial adjustments and even picking up new skills.

Solidifying Your Financial Foundation

During pre-retirement, your focus has to sharpen. It’s all about transforming that nest egg you’ve built into a reliable, steady source of income. This means taking a few key actions to get your finances ready for the transition. Getting these details right is what provides long-term stability and, just as importantly, peace of mind.

Here are the key financial priorities:

- Maximize Your Savings: Now is the time to take full advantage of catch-up contributions in your 401(k) and IRA. These special provisions let you sock away more cash in the years right before you retire, giving your portfolio one last powerful boost.

- Wipe Out High-Interest Debt: Put a laser focus on paying down credit cards, personal loans, or any other debt that's costing you a fortune in interest. Entering retirement debt-free is one of the most liberating things you can do for your financial flexibility.

- Create a Real-World Retirement Budget: Move past the guesswork. Track what you’re spending now and build a realistic budget for your post-career life. Don't forget to account for everything, from daily coffee runs to big travel plans and healthcare costs.

The goal of pre-retirement isn't just to save more, but to save smarter. It’s about creating a durable financial structure that can support your lifestyle for decades to come, no matter what the market does.

Preparing for the Lifestyle Shift

Beyond just the numbers, this phase is about getting ready for a huge shift in your identity. For many of us, our careers provide structure, a sense of purpose, and a social network. Figuring out how you’ll replace those things is just as crucial as managing your portfolio.

This is especially true for business owners facing this life change; you need specific strategies to ensure a smooth transition and financial security. It's worth exploring specialized guidance on retirement planning for business owners for more tailored advice.

Getting on the same page with your partner about your shared goals and actually visualizing what your day-to-day life will look like is an essential exercise. This is also the time to strategize the absolute best moment to claim Social Security and pension benefits to maximize your income over your lifetime. For a deeper dive into these core concepts, check out our guide on the 5 financial planning basics to consider now.

Living Fully in the Go-Go Years

Welcome to what many call the "honeymoon" phase of retirement. The Go-Go years, typically the first stretch after you stop working, are all about newfound freedom, high energy, and the excitement of finally chasing passions you’ve had on the back burner for decades. This is often a time of higher spending as you check off bucket-list trips, pour money into new hobbies, or maybe even relocate to that dream spot you've always talked about.

This exciting period is one of the most rewarding parts of retirement, but it also forces a critical question: Can your financial plan handle this more active lifestyle without jeopardizing your security down the road? Learning to manage this high-spend period is the key to enjoying it without a shred of worry.

Balancing Adventure with Financial Prudence

That initial thrill of retirement can sometimes sour into what's known as the “disenchantment phase” if you're not careful. Believe it or not, research shows that 85-90% of retirees might eventually feel a bit aimless or disillusioned after the vacation-like rush wears off. A huge contributor to this is often financial anxiety that creeps in from overspending in those early years.

The trick is to put a few financial strategies in place specifically for this unique life stage. Think of it as creating guardrails for your adventures.

A couple of practical ideas include:

- Creating a Dedicated 'Adventure Fund': Before you even retire, earmark a specific chunk of your savings just for travel and big hobbies. This gives you a clear green light to spend from this account without ever touching your core retirement capital.

- Using a Bucket Strategy: This popular approach involves splitting your assets into different "buckets." One bucket holds cash for your immediate living expenses (1-3 years). Another holds medium-term bonds, and a third contains long-term growth stocks. You live off the cash bucket, allowing your investments to grow untouched, and you simply refill it periodically.

The goal isn't to put a leash on your fun—it's to fund it intelligently. By separating your 'Go-Go' spending from your long-term, income-producing assets, you give yourself permission to enjoy today while protecting your financial health for all the phases of retirement yet to come.

Building Your New Social and Personal Structure

Just as important as managing your money is rebuilding the personal structure your career once provided. Think about it: work gives you a routine, a sense of identity, and a built-in social network. When that vanishes, it can leave a pretty big hole.

Proactively building a new framework for your days is crucial for lasting happiness. Start creating new routines that bring you genuine joy and a sense of purpose. This could mean joining a local club, volunteering for a cause you're passionate about, or just setting a simple schedule for regular exercise and coffee with friends. Cultivating these new connections and activities is what ensures your Go-Go years are not just active, but deeply fulfilling.

Finding Your Rhythm in the Slow-Go Years

After the whirlwind of the “Go-Go” years, most retirees find themselves easing into a different, more sustainable gear. This next chapter is what we call the “Slow-Go” years, a time defined less by a packed itinerary and more by finding a deep, satisfying rhythm. Life’s pace just naturally moderates. You'll likely see your spending follow suit as your focus shifts from ticking off bucket-list travel to enjoying local experiences, connecting with family, and getting more involved in your community.

It's all about settling in and truly enjoying the life you’ve worked so hard to build.

From a financial standpoint, this is a time for careful monitoring and steady adjustments. With a more predictable lifestyle, it’s easier to check in on your investment performance and tweak your withdrawal strategy as needed. The goal is to align your spending with your financial plan, making sure you have long-term stability without giving up your quality of life.

Proactive Healthcare and Lifestyle Planning

The Slow-Go phase is the perfect time to make some crucial decisions about the future, especially while you're still active and in good health. Taking a proactive approach to healthcare and your living situation now brings an incredible amount of peace of mind. It’s about making clear-headed choices from a position of strength, ensuring your wishes are known no matter what comes next.

Here are a few key areas to tackle:

- Review Long-Term Care Options: This is the time to investigate long-term care insurance or other strategies to cover potential health needs down the road. Understanding your options now prevents rushed, stressful decisions later on.

- Update Estate Documents: Dust off your will, trusts, and powers of attorney. Make sure they’re current and still reflect exactly what you want. Life changes, and your estate plan needs to keep up.

- Evaluate Your Living Situation: Does your current home still fit your life? Think about whether downsizing, renovating to age in place, or even relocating makes sense for your long-term comfort and mobility.

The planning you do in the Slow-Go years is a gift to your future self and your family. It's about taking control of the variables you can, so you can navigate the ones you can't with confidence and dignity.

Shifting Priorities Toward Well-Being

As people settle into this phase, there's often a global shift in priorities toward quality of life, healthcare access, and community. You can see this trend in the rising popularity of international retirement. In fact, 61% of countries offering retirement visas also provide tax benefits, and 68% keep application costs low. This isn't just about finding a sunny beach; it highlights a widespread focus on financial sustainability and finding supportive services in mid-to-late retirement. You can discover more insights about global retirement trends and what they mean for financial planning.

Ultimately, the Slow-Go years are about finding a sustainable kind of contentment—one that’s grounded in a well-managed financial reality and thoughtful preparation for the road ahead.

Navigating the Challenges of Late Retirement

The later years of retirement—sometimes called the 'No-Go' phase—are less about grand adventures and more about adapting to the inevitable changes in our health and mobility. While everyone's journey looks different, a little proactive planning at this stage is the key to staying in control and securing your peace of mind.

The focus naturally pivots from growing your wealth to managing it wisely. You’ll be thinking more about healthcare, simplifying daily life, and making sure your money is ready for potential medical or long-term care costs. This isn't just a financial exercise; it's about building a solid support system that eases the burden on your loved ones and lets you focus on your well-being.

Practical Steps for Peace of Mind

Taking a few concrete steps now is a true gift to your future self and your family. It’s all about getting your legal, financial, and logistical house in order so your wishes are crystal clear and your needs are met, no matter what. Think of it as creating a roadmap for your family to follow, taking the guesswork and stress out of an already emotional time.

Here are a few essential steps to consider:

- Appoint a Power of Attorney (POA): This is one of the most critical things you can do. Designate a trusted person to handle your financial and healthcare decisions if you're ever unable to do so yourself.

- Organize Important Documents: Create one central, easy-to-find file (whether it's a physical binder or a secure digital folder) with everything that matters. Include your will, trust documents, insurance policies, bank account details, and contact info for your financial advisor and attorney.

- Make Your Home Safer: Take a walk through your home and look for potential hazards. Simple tweaks like adding grab bars in the bathroom, improving the lighting, and removing throw rugs can make a massive difference in preventing falls and helping you stay independent for longer.

Financial and Lifestyle Adjustments

On the financial front, this period calls for a careful review of your assets and expenses. The goal is to make sure your income streams can comfortably support any increased healthcare needs. This might mean adjusting your portfolio or rethinking your retirement withdrawal strategies to favor stability and easy access to cash over aggressive growth.

Late-retirement planning is about ensuring your financial and personal affairs are in order, granting you and your family clarity and comfort. It's the ultimate act of taking care of the people you love by preparing for the inevitable.

Simplifying your lifestyle often becomes a top priority, too. For many, this means downsizing to a more manageable home. As you navigate that process, a compassionate guide to downsizing for seniors can offer invaluable support in making thoughtful decisions. Planning ahead like this keeps you in the driver’s seat, ensuring your late retirement is lived with dignity and security.

Building Your Legacy Beyond Wealth

As you move through the later stages of retirement, your perspective often shifts. The focus expands beyond your own comfort and asks a much bigger question: what will you leave behind?

Your legacy is so much more than just the numbers in your accounts. It's the values you stood for, the stories people will tell, and the impact you made on your family and community. This phase is all about defining that deeper purpose and taking steps to make it a reality.

A huge piece of this puzzle is structuring your financial legacy. This means smart estate planning to ensure what you’ve built is passed down exactly as you wish, while minimizing taxes and heading off potential family disputes before they can start. It’s about having a clear, legally sound plan in place.

Defining Your Financial and Personal Legacy

Building a legacy is a two-sided coin: it requires both financial planning and personal reflection. The two are completely intertwined—your financial tools are what bring your personal values to life. Whether you want to support your family for generations or contribute to a cause you believe in, a well-designed plan is the key.

Here are a few ways to start thinking about it:

- Strategic Charitable Giving: This is a powerful way to support causes you’re passionate about while also being tax-efficient. You could set up a donor-advised fund or make direct contributions that reflect what’s most important to you.

- Establishing Trusts: Trusts are incredibly useful tools. They give you control over how and when your assets are distributed, which helps protect your beneficiaries and ensures your wealth is managed wisely long after you're gone.

- Comprehensive Estate Planning: This is the foundational roadmap for your entire legacy. For a deeper dive into why this is so critical, our guide explores if you need an estate plan.

Your legacy is the story that will be told about you long after you are gone. It's built not just with wealth, but with wisdom, intention, and the values you pass down.

But just as important—if not more so—is the non-financial legacy. This is the wisdom you share and the family traditions you create. It could look like mentoring a young person in your field, putting together a detailed family history, or simply spending dedicated time passing down skills and stories to your grandkids.

Ultimately, defining and acting on your legacy brings a profound sense of fulfillment. It transforms retirement from simply being an endpoint into a period of lasting significance, ensuring your influence and values carry on for a long, long time.

Rethinking Retirement with a Phased Approach

The old idea of a hard-stop retirement—working full-time one day and being completely retired the next—is quickly becoming a thing of the past. Let's be honest, that sudden leap from a packed schedule to wide-open days isn't for everyone. Instead, many people are now easing into their next chapter with a phased approach.

This simply means gradually reducing work hours or shifting to a more flexible, less demanding role. It’s a strategy that creates a much smoother and more manageable transition, effectively blurring the lines between your final working years and the "Go-Go" phase of retirement. The financial advantages are powerful, too. You give your investments more time to grow while potentially delaying the need to start taking withdrawals. Just as important, it helps you hang on to the sense of purpose, routine, and social connection that so many people miss after leaving the workforce entirely.

Is a Phased Retirement Right for You?

This modern approach isn't just a passing trend; it's a practical response to today's economic realities. In the U.S., 33% of individuals have already postponed retirement, and 30% are planning to retire in stages, often because of financial pressures. In fact, workforce participation among those aged 65 and older has grown faster than the overall labor market. That signals a major shift in how we think about the final leg of a career. You can discover more insights about these retirement trends and what’s driving them.

Deciding if a phased retirement fits your life involves weighing both the financial and personal benefits.

A phased retirement transforms the end of a career from an abrupt stop into a gentle off-ramp. It provides the space to adjust emotionally and financially, ensuring the transition into the next chapter is both secure and fulfilling.

If you're considering this path, here are a few key things to think through:

- Financial Impact: How will a reduced income affect your budget? Run the numbers to see how long you can delay tapping into your retirement accounts.

- Employer Flexibility: Not all companies have formal programs, so you’ll need to talk to your employer. See if options like reduced hours, remote work, or a consulting role are on the table.

- Personal Fulfillment: What do you want to get out of your remaining work years? Is it about staying engaged and challenged, earning some extra income, or simply maintaining those daily social connections?

Structuring this transition thoughtfully can make the journey through all the phases of retirement far more enjoyable and a lot less jarring.

At Commons Capital, we specialize in helping clients design financial strategies that align with their unique vision for retirement, whether that’s a traditional path or a more flexible, phased approach. Learn more about how we can help you plan for every stage of your life.