Choosing the right advisor is one of the most significant financial decisions you'll ever make, especially when substantial assets are involved. The quality of this partnership hinges on alignment, transparency, and specialized expertise. Yet, many high-net-worth individuals, business owners, and retirees are not entirely sure where to begin the crucial vetting process. This guide provides the essential questions to ask a wealth manager, ensuring you can confidently select a partner who truly understands your complex needs and is equipped to safeguard and grow your legacy.

Before you entrust your wealth to anyone, use this comprehensive checklist to conduct a thorough and insightful interview. A well-structured conversation is the best tool to uncover potential red flags, understand an advisor’s core philosophy, and ultimately find a fiduciary who will prioritize your best interests above all else. Finding the right fit requires more than a surface-level discussion; it demands a deep dive into their processes, ethics, and experience. For those looking to improve their overall financial acumen, gaining additional financial fitness insights can also provide a solid foundation for these important conversations.

This listicle moves beyond generic queries. We will break down not just what to ask, but why each question matters, what a great answer looks like, and the follow-up questions that separate a good advisor from a great one. We will explore key areas including fiduciary duty, fee structures, investment philosophy, risk management, and experience with specialized situations like concentrated stock positions or multi-generational wealth transfer. This framework is designed to empower you to make your decision with absolute clarity and confidence.

1. What is your investment philosophy and how do you construct diversified portfolios?

This is one of the most critical questions to ask a wealth manager because their answer reveals the fundamental principles guiding every investment decision made on your behalf. A manager's investment philosophy is their strategic blueprint for growing and preserving your capital. It dictates whether they favor active management (picking individual securities) or passive strategies (tracking market indexes), and how they approach risk.

For high-net-worth individuals, understanding this philosophy is crucial as it directly impacts how your substantial assets are allocated across stocks, bonds, real estate, and alternatives. A clear, well-reasoned philosophy ensures their approach aligns with your personal financial goals, risk tolerance, and time horizon.

What a Good Answer Looks Like

A strong response will be clear, confident, and supported by evidence. The manager should be able to articulate their core beliefs without resorting to jargon.

- Example 1 (Blended Approach): "Our core philosophy is a 'core-satellite' approach. We build the 'core' of your portfolio, about 75%, with low-cost, diversified index funds and ETFs for broad market exposure. The remaining 25% 'satellite' is dedicated to actively managed investments in sectors where we see unique opportunities, like emerging tech or healthcare innovation. This balances cost-efficiency with the potential for outperformance."

- Example 2 (Factor-Based): "We follow an evidence-based, factor-investing philosophy, popularized by firms like Dimensional Fund Advisors. We construct portfolios that systematically tilt towards factors historically associated with higher returns, such as value, profitability, and company size. This removes emotional decision-making and relies on academic research to drive long-term growth."

Red Flags to Watch For

- Vagueness: Answers like "We buy good companies" or "Our goal is to make you money" are too generic.

- Chasing Trends: A philosophy that seems to change with every market headline suggests a lack of a disciplined, long-term strategy.

- Inability to Explain: If a manager cannot explain their philosophy in simple terms, they may not fully understand it themselves.

Actionable Follow-Up Questions

- Can you provide your firm's written investment policy statement or philosophy document?

- How did this philosophy perform during the 2008 financial crisis or the 2020 COVID-19 downturn?

- How do you customize this philosophy to accommodate a client's specific goals, like funding a charitable foundation or planning for a business sale?

2. How do you customize financial plans for high-net-worth individuals and families?

This question probes beyond investment management to assess a wealth manager's ability to handle the intricate financial lives of high-net-worth (HNW) clients. A generic, one-size-fits-all financial plan is inadequate for those facing challenges like multi-generational wealth transfer, complex tax scenarios, or concentrated business holdings. You need a bespoke strategy, not a template.

For affluent families, the answer reveals whether the manager can integrate diverse elements such as business succession, executive compensation, and philanthropic goals into a single, cohesive plan. This holistic approach ensures all aspects of your financial life work in concert, protecting and growing wealth in a way that aligns with your family’s unique values and long-term vision.

What a Good Answer Looks Like

A strong answer will detail a structured, yet flexible, planning process. The manager should demonstrate experience with situations similar to yours and emphasize a deep, personal discovery phase.

- Example 1 (For a Business Owner): "Our process begins with a deep dive into your business and personal balance sheets. For a business owner like you, we'd integrate a business valuation and succession plan directly into your personal retirement and estate strategy. This ensures we manage liquidity events, like a future sale, in the most tax-efficient way possible while securing your family's future."

- Example 2 (For a Corporate Executive): "We specialize in navigating complex executive compensation. Our first step is to analyze your entire package, including RSUs, stock options, and deferred compensation plans. We then build a customized strategy around tax-advantaged exercising and diversification schedules to manage concentration risk while aligning with your long-term goals for retirement and legacy."

Red Flags to Watch For

- Product-Pushing: If the conversation quickly shifts to specific investment products before they fully understand your situation.

- Vague Process: Answers like "We get to know you and build a plan" without specific steps or details about their discovery process.

- Lack of Relevant Experience: Hesitation or inability to provide examples of how they've helped clients in situations similar to yours.

Actionable Follow-Up Questions

- Can you walk me through your financial planning process, from our first meeting to plan implementation and review?

- What specialists (e.g., estate attorneys, CPAs) do you collaborate with, and how is that process managed?

- How often would we review and update this plan, and what events would trigger an immediate revision?

3. What are your fees and how are they structured (AUM, flat fee, commission-based)?

Fee transparency is non-negotiable when selecting a wealth manager. This question cuts to the core of your professional relationship, revealing not just the cost of their services but also the alignment of their incentives with your financial success. Different fee models, such as assets under management (AUM), flat fees, or commissions, can create vastly different outcomes and potential conflicts of interest.

For high-net-worth clients, a small percentage difference in fees can amount to tens or hundreds of thousands of dollars over time. You must understand how fees are calculated, what services they cover, and whether the structure promotes a fiduciary standard of care. Understanding the total cost is one of the most vital questions to ask a wealth manager before engaging their services.

What a Good Answer Looks Like

A trustworthy manager will provide a clear, written fee schedule and proactively explain all potential costs, including those from third parties. Their answer should be direct and transparent.

- Example 1 (Tiered AUM): "We operate on a fee-only basis using a tiered AUM model. Our fee is 1.0% on the first $1 million, 0.75% on the next $4 million, and 0.50% on assets above $5 million. This structure ensures our compensation grows only when your portfolio grows, aligning our interests directly with yours. It includes all financial planning, investment management, and coordination with your CPA and attorney."

- Example 2 (Flat Fee): "We charge a flat annual fee for comprehensive wealth management, which typically ranges from $20,000 to $50,000 depending on the complexity of your situation. This fee is quoted upfront and covers everything from estate planning strategy to tax optimization and investment oversight. We find this eliminates any incentive to gather more assets and focuses us purely on providing advice."

Red Flags to Watch For

- Lack of a Written Schedule: If they can't provide a clear, documented fee schedule, consider it a major red flag.

- Emphasis on Commissions: A "fee-based" advisor may still earn commissions from selling products like insurance or annuities, creating a conflict of interest.

- Hidden Costs: Evasive answers about underlying fund expenses, trading costs, or custodial fees suggest a lack of full transparency.

Actionable Follow-Up Questions

- Could you provide a sample fee calculation for a portfolio of my size and complexity?

- Are there any other costs I should be aware of, such as trading fees or internal expense ratios on the funds you use?

- Are your fees negotiable for clients with significant assets?

- For a comprehensive understanding of different models, you can explore this wealth management fees comparison to see how various structures stack up.

4. How do you handle tax efficiency and what is your tax optimization strategy?

For high-net-worth investors, what you keep after taxes is often more important than the headline return. This question dives into a wealth manager's ability to proactively minimize your tax burden, a critical component that can significantly boost your net returns over time. A sophisticated manager sees tax optimization not as a year-end task, but as an integral part of portfolio construction, trading, and long-term planning.

Effective tax management involves a suite of strategies, from asset location (placing tax-inefficient investments in tax-advantaged accounts) to strategic charitable giving. Understanding a firm’s approach is essential because studies from firms like Morningstar suggest that tax-efficient management can add a substantial percentage to annual after-tax returns, compounding powerfully over the long term.

What a Good Answer Looks Like

A compelling answer will demonstrate a systematic, ongoing process for tax management that is integrated into their investment approach. The manager should provide specific, tangible examples of how they add value.

- Example 1 (Systematic Approach): "We integrate tax management directly into our portfolio management. We employ a continuous tax-loss harvesting strategy, scanning portfolios daily for opportunities to offset gains. We also prioritize asset location, strategically placing high-turnover or income-producing assets like corporate bonds in tax-deferred accounts, while growth-oriented, tax-efficient equities are held in taxable accounts to benefit from lower long-term capital gains rates."

- Example 2 (Concentrated Position Focus): "For clients with concentrated stock positions, our strategy is multifaceted. We create a long-term diversification plan to minimize capital gains, often using donor-advised funds for charitable inclinations to get a deduction while offloading appreciated shares. We also coordinate directly with your CPA to ensure our trading activity aligns with your overall tax picture, especially concerning estimated quarterly payments."

Red Flags to Watch For

- Reactive vs. Proactive: A manager who says, "We can sell some losers at the end of the year if you want" is being reactive. A proactive manager has a defined, ongoing strategy.

- Lack of Coordination: An unwillingness to work directly with your CPA or tax attorney is a major red flag, as it can lead to siloed, inefficient financial decisions.

- No Specifics: Vague statements like "We are very tax-aware" are insufficient. They should be able to describe their actual process and the tools they use.

Actionable Follow-Up Questions

- What is your specific policy on tax-loss harvesting? Is it automated or manual, and what is the minimum loss you typically harvest?

- Can you provide an example of how you helped a client with a concentrated stock position diversify in a tax-efficient manner?

- How do you coordinate with my other advisors, like my CPA and estate planning attorney, on tax-related matters?

5. How do you approach risk management and what happens during market downturns?

This question is paramount because it probes beyond generating returns and into the critical function of preserving capital. For high-net-worth individuals, protecting substantial assets from significant loss is often as important as growing them. A wealth manager's approach to risk management reveals their discipline, foresight, and strategy for navigating the inevitable market turbulence.

Understanding their playbook for downturns is crucial. It shows whether they have a systematic process to mitigate losses and a communication plan to guide you through volatility, preventing reactionary decisions. This is what separates professional asset management from simple investing; it's the structured defense that protects your long-term financial plan.

What a Good Answer Looks Like

A confident answer will detail a proactive, multi-layered risk management framework. The manager should clearly explain both their portfolio construction techniques and their client communication strategy during periods of market stress.

- Example 1 (Diversification & Rebalancing): "Our primary risk tool is true diversification. We construct portfolios with a 60% stock, 30% bond, and 10% alternatives mix, which helps cushion against equity market shocks. During the 2020 COVID correction, this model saw a -15% decline versus -25% for a more stock-heavy portfolio. We also adhere to a strict rebalancing discipline, systematically trimming over-performing assets and buying under-performing ones to maintain our target allocation."

- Example 2 (Hedging & Communication): "We actively manage downside risk using tactical strategies like options or managed futures to hedge against severe market declines. For qualified clients, this can limit portfolio downside to a pre-defined level, for instance, a maximum loss of -10% when the broader market falls -20%. Equally important is our communication plan; during volatile periods, we increase our outreach with weekly market updates and proactive calls to ensure you understand our strategy and remain focused on your long-term goals."

Red Flags to Watch For

- No Clear Plan: Answers like "We just ride it out" or "We advise clients not to panic" lack a concrete strategy.

- Over-Reliance on Market Timing: A manager who claims they can perfectly time market tops and bottoms is unrealistic and likely taking on undue risk.

- Lack of Historical Context: If they can't explain how their strategy performed in past downturns like 2008 or 2020, they may lack experience or a tested process.

Actionable Follow-Up Questions

- Can you show me how a model portfolio similar to mine performed during the 2008 and 2020 market crises?

- Do you conduct stress tests on portfolios, and can you walk me through the results under different scenarios?

- What is your specific communication protocol when the S&P 500 experiences a correction of 10% or more?

6. What is your experience with sports and entertainment industry clients, and how do you address their unique financial challenges?

This is a vital question for professionals in sports and entertainment, whose financial lives defy conventional planning. Their careers often involve short, high-earning windows, irregular income streams from contracts and endorsements, complex compensation structures, and intense public scrutiny. A generic financial plan simply won't suffice.

Asking a wealth manager about their specific experience with this demographic ensures they understand these unique pressures. An adept advisor will have proven strategies for income smoothing, career transition planning, tax-efficient structuring of deals, and preserving wealth long after the spotlight fades. Their expertise is critical for turning a few high-earning years into a lifetime of financial security. When considering a wealth manager, it's beneficial to ask about their understanding of these unique career arcs, perhaps even drawing on resources offering motivational insights for sports business life.

What a Good Answer Looks Like

A strong answer will demonstrate deep, firsthand knowledge of the industry's financial landscape and provide concrete examples of how they've guided clients through it.

- Example 1 (Athlete Focus): "We specialize in working with professional athletes. For a recent NFL client, we built a multi-year plan centered on his signing bonus, smoothing that income to cover his entire estimated 10-year career. We established trusts for tax efficiency and set up a post-career business venture, ensuring his earnings work for him long after he leaves the field."

- Example 2 (Entertainer Focus): "We helped a musician transition from touring income to a more stable financial life built on royalties and intellectual property. We structured their endorsement deals through an S-corp for tax advantages and created a family wealth education program to teach their children about financial stewardship and long-term planning."

Red Flags to Watch For

- Generic Responses: An advisor who says, "We treat all our clients the same," likely lacks the specialized knowledge you need.

- Lack of Specifics: If they can't provide examples of how they've handled lump-sum payments, deferred compensation, or royalty streams, they may be out of their depth.

- No Professional Network: An advisor without a network of agents, entertainment lawyers, and CPAs familiar with the industry cannot provide comprehensive service.

Actionable Follow-Up Questions

- Can you walk me through a case study of a client with a similar career trajectory to mine?

- How do you help clients manage lifestyle pressures and avoid overspending during peak earning years?

- What is your process for planning a client's transition out of their primary career? You can learn more about our approach through our guide on wealth management for professional athletes.

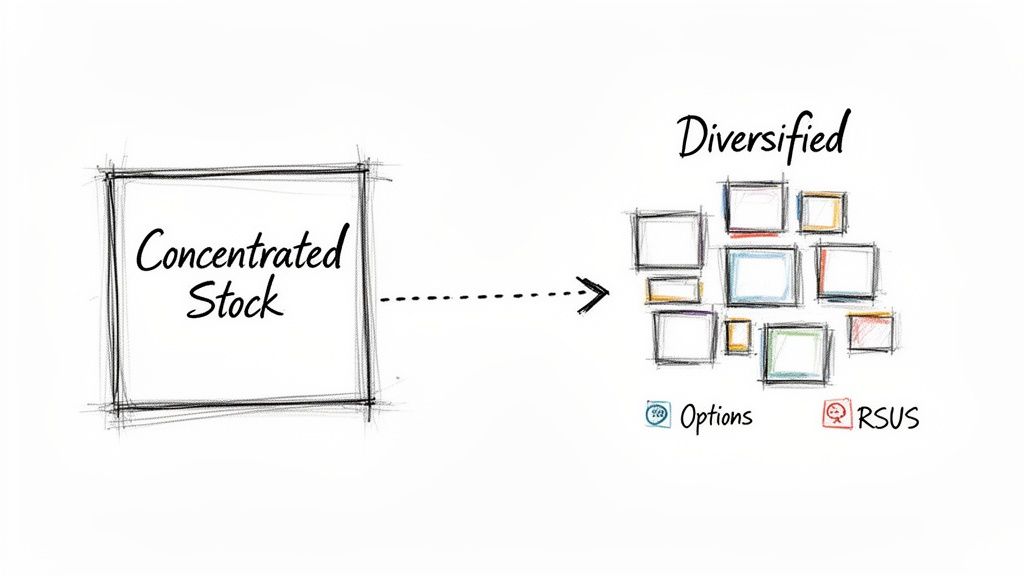

7. How do you handle concentrated stock positions and executive compensation planning?

This question is vital for high-net-worth individuals, especially business owners and corporate executives, whose wealth is often tied up in a single company's stock. A concentrated stock position creates significant risk, as your financial future becomes overly dependent on the performance of one asset. Managing this requires a sophisticated understanding of diversification strategies, tax implications, and executive compensation nuances.

This is a critical question to ask a wealth manager because a generic "sell and diversify" approach can trigger massive tax liabilities and cause you to miss out on future growth. An expert advisor will have specialized tools and strategies to mitigate risk while managing tax efficiency and retaining upside potential. Their ability to navigate stock options (ISOs vs. NSOs), Restricted Stock Units (RSUs), and insider trading rules is a key differentiator.

What a Good Answer Looks Like

A knowledgeable manager will immediately move beyond simple diversification and discuss a multi-pronged, customized strategy. They should sound like a specialist, not a generalist.

- Example 1 (For a Tech Executive): "For a position like yours, we would first analyze your RSU vesting schedule and tax situation. We'd likely implement a systematic sell-down plan using a 10b5-1 trading plan to avoid insider trading concerns. For your vested shares, we might explore a 'collar strategy,' where we use options to set a floor on the downside risk while allowing for some upside participation, deferring capital gains taxes in the process."

- Example 2 (For a Business Owner): "Given the low cost basis of your privately held stock, a direct sale would be tax-prohibitive. We could explore contributing a portion of your shares to an exchange fund. This would allow you to swap your concentrated position for a diversified portfolio of other private company stocks on a tax-deferred basis, immediately diversifying your risk without a current tax bill."

Red Flags to Watch For

- One-Size-Fits-All Advice: A manager who only suggests "sell it all and buy mutual funds" ignores the immense tax and opportunity cost implications.

- Lack of Specifics: If they can't clearly explain the mechanics of a collar, a variable prepaid forward, or an exchange fund, they lack the necessary expertise.

- Ignoring the Tax Impact: A failure to immediately bring up the tax consequences of any diversification strategy is a major red flag.

Actionable Follow-Up Questions

- Can you walk me through a case study of how you helped a client in a similar situation?

- What are the specific tax implications and costs associated with the strategies you recommend?

- How do you coordinate with a client’s CPA and estate planning attorney to ensure these strategies are fully integrated?

8. What is your process for understanding my goals and how do you measure success?

This question shifts the focus from abstract market returns to what truly matters: your life. A top-tier wealth manager recognizes that your portfolio is a tool designed to fund your specific life goals, not just to outperform an index. Their process for discovering, quantifying, and tracking these goals reveals whether they are a true financial partner or simply an investment salesperson.

For high-net-worth individuals, whose objectives often include complex legacy planning, philanthropy, or business succession, this goal-based approach is paramount. It ensures that every financial decision is intentionally aligned with your unique vision for the future, providing a clear roadmap and a meaningful benchmark for success.

What a Good Answer Looks Like

A strong answer will detail a structured, multi-step discovery process and explain how they translate life goals into an actionable financial plan with clear metrics.

- Example 1 (Comprehensive Discovery): "Our process begins with a deep discovery phase using a detailed questionnaire and several in-depth meetings to understand your values, family dynamics, and specific objectives, like retiring at 60 with a $250k annual income. We then use financial planning software to model various scenarios, stress-test your plan, and determine a probability of success, aiming for a 90% confidence level. Success isn't just about beating the S&P 500; it's about our annual review showing you're on track to exceed your retirement funding goal."

- Example 2 (Dynamic Goal Tracking): "We believe your plan must be a living document. After quantifying your goals, we create a personalized 'Wealth Plan' that we review with you semi-annually. Our reporting goes beyond portfolio performance; it shows your progress toward each specific goal, such as funding your children's education or your charitable foundation. When a life event occurs, like an inheritance, we immediately update the plan to analyze how the new capital can best be deployed to accelerate your objectives."

Red Flags to Watch For

- Portfolio-First Approach: If the manager immediately starts talking about investment products before asking about your goals.

- Benchmark Obsession: A singular focus on market benchmarks (like the S&P 500) as the only measure of success.

- Lack of a Process: Vague responses like "We'll have a conversation about your goals" without a clear, systematic framework.

Actionable Follow-Up Questions

- Can I see a sample of your client discovery questionnaire or a redacted financial plan?

- How do you help clients prioritize when they have competing financial goals?

- What is your process for updating the plan when significant life or market events occur?

9. How do you coordinate with other professional advisors and approach estate & wealth transfer planning for multi-generational wealth?

For high-net-worth families, financial success isn't managed in a vacuum. True wealth management involves a synchronized effort between your wealth manager, CPA, estate planning attorney, and insurance specialists. This question assesses a manager's ability to act as the "quarterback" of your financial team, ensuring every decision is tax-efficient, legally sound, and perfectly aligned with your family's long-term legacy goals.

This collaborative approach is essential for sophisticated strategies like multi-generational trusts, charitable giving, and business succession. It prevents costly oversights where an investment decision might create an unintended tax consequence or conflict with your estate plan. A manager who excels at coordination can help you effectively create generational wealth by ensuring your entire financial picture is cohesive.

What a Good Answer Looks Like

A strong answer will detail a proactive and structured process for collaboration, demonstrating that they lead the coordination rather than waiting for you to do it.

- Example 1 (Proactive Team Approach): "We see ourselves as your family's Chief Financial Officer. With your permission, we establish a formal communication channel with your CPA and estate attorney. We host an annual joint meeting to review your portfolio, recent tax returns, and trust documents together. This allows us to, for instance, coordinate the timing of a large stock sale with your CPA to optimize for capital gains, while ensuring the proceeds are titled correctly per your estate plan."

- Example 2 (Structured Process): "Our process begins by creating a shared financial dashboard that all your trusted advisors can access. Before recommending any major strategy, like setting up a Spousal Lifetime Access Trust (SLAT), we model the financial and tax implications and share our analysis with your attorney and accountant for their input. This ensures every piece of the plan works in harmony from day one."

Red Flags to Watch For

- Siloed Thinking: A manager who says, "We just handle the investments; you'll have to talk to your CPA about taxes."

- Lack of a Process: Vague responses like "We can call your attorney if needed" suggest they lack a formal, proactive coordination strategy.

- No Professional Network: If they cannot refer you to trusted CPAs or attorneys they have worked with, it may indicate a lack of experience with complex HNW planning.

Actionable Follow-Up Questions

- Can you provide an anonymous example of how your coordination with a client's CPA and attorney resulted in a better outcome?

- How do you facilitate communication and information sharing between all the professionals on my team?

- What is your process for preparing the next generation to responsibly inherit and manage the wealth you are helping us build?

10. How do you stay informed about market conditions, regulatory changes, and emerging opportunities?

The financial landscape is in constant flux, with markets shifting, tax laws evolving, and new regulations emerging. This question tests a wealth manager's commitment to continuous learning and professional development, which is essential for providing timely and effective advice. A proactive manager doesn't just react to change; they anticipate it to protect your assets and capitalize on new opportunities.

For high-net-worth clients, a manager’s ability to stay current can mean the difference between seizing a lucrative tax-planning window or missing it entirely. Their process for staying informed reveals whether they are a dynamic advisor who adapts to the environment or one who relies on outdated, static strategies.

What a Good Answer Looks Like

A strong answer will detail a systematic process for absorbing and applying new information. It should highlight a blend of formal education, technology, and industry engagement.

- Example 1 (Systematic Approach): "Our firm has a dedicated research team that provides daily market summaries and in-depth analysis on economic trends. Personally, I dedicate two hours every morning to reading key publications like The Wall Street Journal and The Financial Times, and I use a Bloomberg Terminal for real-time data. We also hold weekly team meetings to discuss regulatory updates from sources like the CFP Board and identify how changes, like the SECURE Act 2.0, create new planning opportunities for our clients."

- Example 2 (Professional Development Focus): "As a CFA charterholder, I am required to complete at least 20 hours of continuing education annually, which I often exceed. I focus on topics relevant to my clients, such as advanced estate planning and alternative investments. I also attend several industry conferences each year, which helps me identify emerging strategies and network with other top professionals. This is how we first identified a unique private credit opportunity that benefited several of our accredited investor clients last year."

Red Flags to Watch For

- No Clear Process: Answers like "I read the news" are insufficient. A lack of a defined system for staying informed is a major concern.

- Outdated Credentials: A manager who hasn't pursued any continuing education or new certifications in years may not be up-to-date on modern financial strategies.

- Dismissiveness: A manager who downplays the importance of staying current on regulatory or tax law changes may expose your portfolio to unnecessary risks.

Actionable Follow-Up Questions

- What specific publications, research platforms, or tools do you rely on daily?

- Can you give a recent example of how a regulatory or tax law change prompted you to contact your clients with new advice?

- How much time do you and your team dedicate to professional development and training each year?

Moving Forward: How to Make Your Final Decision

You have journeyed through a comprehensive framework of critical questions designed to empower your search for the right wealth management partner. This isn't just a simple checklist; it's a strategic tool for uncovering the core values, expertise, and operational integrity of any potential advisor. The process of asking these questions is as revealing as the answers themselves. Pay close attention not only to what they say but how they say it. Is their communication clear? Do they listen intently to your follow-up questions? Does the conversation feel like a partnership or a sales pitch?

The goal is to move beyond the surface-level gloss of a marketing brochure and truly understand the engine that will be driving your financial future. By probing into everything from their fiduciary commitment and fee structure to their specific experience with complex situations like concentrated stock positions or the unique financial cycles of entertainment professionals, you are building a 360-degree view of your potential partner. This diligence is the foundation of a successful, long-term advisory relationship.

Synthesizing the Answers: From Information to Insight

After conducting several interviews, you will have a wealth of information. The next crucial step is to synthesize this data into actionable insight. Don't let the details overwhelm you. Instead, organize your notes and reflect on the key themes that emerged from each conversation.

Consider these three essential pillars as you compare your candidates:

- Alignment: Does the advisor's investment philosophy, risk tolerance, and communication style align with your own? A philosophical mismatch can create friction and doubt, especially during periods of market volatility. The right partner should feel like a natural extension of your own financial thinking.

- Expertise: Did the advisor demonstrate deep, specific knowledge relevant to your unique situation? For a business owner, this might be succession planning. For a professional athlete, it could be managing uneven income streams. Generic answers are a red flag; you are seeking tailored, expert guidance.

- Trust: This is the most critical and often intangible element. Did you feel a genuine sense of rapport and transparency? A true fiduciary relationship is built on a bedrock of trust. You must have unwavering confidence that your advisor is always acting in your best interest, without conflicts of interest clouding their judgment.

Remember, the list of questions to ask a wealth manager is your primary tool for evaluating these pillars. The responses you gather will illuminate which firm is not just competent, but is the right fit for you and your family’s legacy.

Your Final Decision and the Path Ahead

Making your final choice is a significant decision that will have a lasting impact on your financial well-being. This is not a moment to rush. Review your notes, perhaps have a second, more informal conversation with your top one or two candidates, and trust your gut instinct. The ideal wealth manager is more than a financial expert; they are a strategic partner, a confidant, and a steward of your legacy.

By investing the time now to conduct this rigorous due diligence, you are not just hiring a service provider. You are forging a relationship that will provide clarity, confidence, and strategic direction for years to come. You are ensuring that the wealth you have worked so hard to build is protected, nurtured, and positioned to achieve your most ambitious goals, empowering you to focus on what truly matters in your life.

Finding a firm that can confidently and transparently answer these questions is the first step toward a successful partnership. At Commons Capital, we were founded on the principles of fiduciary duty and customized, comprehensive planning for high-net-worth individuals and families. If you are seeking a partner who can provide clear answers and a tailored strategy for your complex financial life, we invite you to start the conversation with us today at Commons Capital.