Finding the right retirement financial advisor is a critical step in preparing for your post-career life. This specialist acts as the architect for your financial future, focusing on one primary goal: turning the assets you've spent a lifetime building into a steady, reliable income stream that lasts as long as you do.

Their job is to create a detailed playbook for how you will live off your investments, manage tax-smart withdrawals, and ensure your financial plan can weather the inevitable storms of market shifts and the wonderful risk of living a very long life.

The Mission of a Retirement Financial Advisor

Staring at your retirement accounts can feel like looking across a vast, uncharted sea. You've got the ship—your life’s savings—but you need a seasoned captain to draw the map and navigate the journey ahead. That's the real role of a retirement financial advisor.

They shift the conversation from simply growing your money to the far more complex art of distributing it. Their entire mission boils down to answering one critical question: How can you maintain the lifestyle you want, for the rest of your life, without ever running out of money? To get there, they build a comprehensive, personalized strategy that accounts for all the variables that retirement throws at you.

Beyond Basic Investment Advice

While a general financial advisor helps you accumulate wealth, a true retirement specialist excels in what the industry calls the "decumulation" phase. Think of them less as a stock picker and more as the general contractor for your entire financial world.

Their key responsibilities look something like this:

- Designing a Sustainable Income Stream: They figure out how to structure your portfolio to generate a reliable "paycheck" from a mix of sources, whether that's your 401(k), pensions, or Social Security.

- Optimizing Tax Strategies: This is huge. They create a withdrawal plan to minimize your tax bill, a move that can add years to the life of your portfolio.

- Managing Longevity and Market Risks: They stress-test your plan. What happens if the market tanks right after you retire? What if you live to be 105? They plan for these scenarios to ensure your strategy is resilient.

- Coordinating Estate and Legacy Goals: They work alongside attorneys to make sure your wealth is passed on smoothly and efficiently to your family or favorite charities, just the way you want.

This kind of specialized focus is becoming more and more critical. As household wealth has grown, so has the complexity of managing it, driving huge growth in the financial advisory profession. Fee-based advisory revenues have jumped from around $150 billion in 2015 to $260 billion in recent years. You can dig into the specifics by checking out the Investment Company Institute's recent findings on this trend. It’s clear people are seeking out expert guidance.

A retirement financial advisor's true value isn't just in picking stocks; it's in creating a durable financial plan that provides peace of mind, allowing you to focus on living your retirement, not just funding it.

Ultimately, they provide a structured framework designed to protect the wealth you’ve spent a lifetime building. Their work is all about making sure your financial resources are strategically lined up to support you through every single chapter of your retirement.

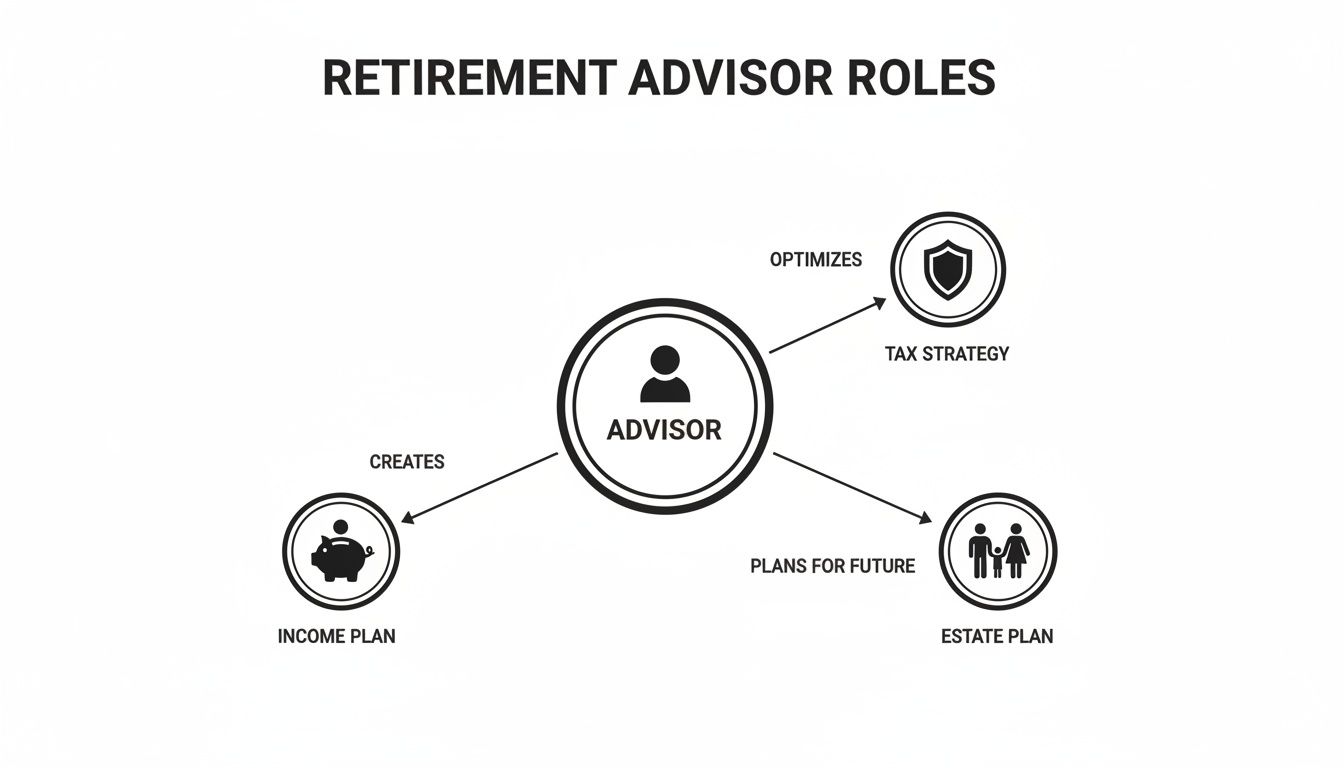

Building Your Retirement Paycheck from Your Portfolio

Getting to retirement isn't just about watching a number grow in your account. The real challenge—and where things get tricky—is figuring out how to turn that pile of assets into a steady, reliable paycheck for the rest of your life. This is where a retirement financial advisor really earns their keep, moving beyond simple investment management into the role of an income architect. Their main job is to design a durable system for drawing down your portfolio so you can actually live your life without constantly worrying about running out of money.

Think of it this way: your portfolio is a giant reservoir of water you've spent decades collecting. A generalist advisor might just give you updates on the water level. A retirement specialist, on the other hand, designs and builds a custom irrigation system. They calibrate every valve and pipe to deliver a predictable flow right when you need it, ensuring that reservoir lasts for the long haul.

A true retirement professional weaves together several critical areas—income planning, tax strategy, and estate coordination—into one cohesive plan.

As the diagram shows, these aren't just separate items on a checklist. They're interconnected parts of a strategy built to protect and distribute your wealth as efficiently as possible.

Creating Tax-Efficient Withdrawal Plans

One of the biggest wins you can get from a retirement-focused advisor is a smart withdrawal strategy. It sounds simple, but deciding which account to pull from first—your 401(k), a Roth IRA, or a taxable brokerage account—can have massive tax consequences. Getting it wrong can easily cost you tens, or even hundreds, of thousands of dollars over your retirement.

A strategic plan isn't just about pulling money out. It might involve:

- Tax Bracket Management: Carefully taking just enough from tax-deferred accounts each year to fill up the lower tax brackets without bumping you into a higher one.

- Roth Conversions: Intentionally moving money from a traditional IRA to a Roth, paying the taxes now to secure tax-free growth and, more importantly, tax-free withdrawals down the road.

- Asset Location: Placing investments that generate a lot of taxes (like corporate bonds) inside tax-sheltered accounts, while keeping more tax-friendly investments (like stocks you plan to hold) in your regular brokerage account.

This isn't guesswork; it's a deliberate approach that keeps more of your money working for you, transforming your nest egg into a much more powerful income engine.

Managing Risk in the Decumulation Phase

The way you think about investment risk has to completely flip once you stop earning a paycheck. While you're working, you have time on your side to recover from a market downturn. But when you’re actively living off your portfolio, a big drop can permanently cripple your financial plan. This nasty little problem is known as sequence of returns risk.

A poor sequence of returns—getting hit with a bear market in the first few years of retirement—can drain a portfolio way faster than expected, even if your long-term average returns end up looking good on paper.

A retirement advisor’s job is to actively fight this risk. They don't just "set it and forget it." They use specific strategies designed to shield your income from market swings. For high-net-worth folks, this often means looking beyond the usual stocks and bonds. This proactive risk management is what lets you sleep at night when you no longer have a W-2 to fall back on.

Coordinating Complex Estate and Trust Plans

For affluent families, retirement planning and legacy planning are two sides of the same coin. A skilled advisor understands they aren't working in a bubble. They act as the quarterback for your professional team, coordinating with your estate planning attorney and CPA to make sure everyone is on the same page.

This collaborative approach is designed to answer critical questions:

- How do we pass wealth to our kids and grandkids in the most tax-efficient way?

- Are our trusts structured properly to protect our assets and provide for our beneficiaries as intended?

- Does our retirement income plan leave room for our charitable giving goals?

By syncing up all these moving parts, an advisor ensures your financial plan is a single, cohesive machine that supports every part of your life and legacy. This integrated teamwork is a true hallmark of a retirement specialist.

Decoding Advisor Fees and the Fiduciary Promise

Before you trust someone with your life savings, you have to understand how they get paid. It's one of the most critical parts of the entire relationship.

An advisor's fee structure isn't just a boring detail on an invoice—it's a bright window into their motivations. It tells you whether their success is tied to yours, or to their ability to sell you something. Navigating the alphabet soup of compensation models can feel overwhelming, but it's the only way to find a partner whose interests are truly aligned with yours.

Let's break down the most common models so you know exactly what questions to ask.

Comparing Financial Advisor Fee Structures

There are really only a handful of ways advisors are paid. This table breaks down the common fee models, outlining how each structure works and its potential impact on your portfolio.

As you can see, the lines can get blurry, especially with the "fee-based" model. The goal is to find a structure where your advisor wins only when you win.

Understanding these distinctions is everything. For a more detailed look, you can dig into the key differences between a fiduciary financial advisor vs fee-only advisor and see just how closely compensation and advice are linked.

The Fiduciary Promise: A Legal and Ethical Duty

Beyond how an advisor is paid, there's a standard of care that is non-negotiable: the fiduciary duty.

Think of it like the Hippocratic Oath for doctors, but for your money. A retirement financial advisor who operates as a fiduciary is legally and ethically bound to put your interests first. Always. No exceptions.

This isn't just a nice-sounding marketing term; it's a legal requirement. It means they must give you advice that is solely in your best interest, even if it means they make less money. It also legally compels them to be transparent about any potential conflicts of interest.

The fiduciary standard is the bedrock of a trustworthy advisory relationship. It provides clients with peace of mind, knowing their advisor is obligated to monitor their financial situation and act as their advocate.

This commitment to your well-being completely changes the dynamic. It shifts the relationship from a sales transaction to a genuine partnership. When you work with a fiduciary, you can be confident that every single recommendation is designed to get you closer to your retirement goals, period.

Advanced Strategies for High-Net-Worth Retirees

Standard retirement advice often misses the mark for high-net-worth individuals and families. Once your wealth reaches a certain level, the financial playbook changes entirely. The challenges are just different—you're dealing with things like concentrated stock positions, multi-generational wealth planning, and ambitious philanthropic goals.

A generic approach just won’t cut it. This is where a specialist retirement financial advisor becomes absolutely critical. They operate in a world beyond basic portfolio models, using sophisticated strategies designed to protect and grow substantial wealth through every chapter of retirement.

Navigating Concentrated Wealth and Complex Incomes

For many successful people, wealth isn't spread neatly across a hundred different stocks. It’s often tied up in a single company’s stock, maybe from a long career as an executive or after selling a business. This creates a classic high-stakes problem: incredible growth potential chained to incredible risk.

An advisor who specializes in this area helps you carefully unwind that position over time without getting hammered by a massive tax bill or cratering the stock’s price. They build a structured plan that might involve:

- Selling shares strategically over several years to keep capital gains taxes manageable.

- Using tools like exchange funds, which can let you swap the concentrated stock for a diversified portfolio on a tax-deferred basis.

- Putting hedging strategies in place to lock in the value of the stock while you figure out a long-term plan.

This same kind of specialized thinking applies to people with irregular income, like professional athletes or entertainers. An advisor helps structure their earnings to build a stable financial base that can last for decades, long after their peak earning years are behind them.

Structuring Philanthropy for Maximum Impact

For many wealthy retirees, giving back is a huge part of the legacy they want to leave. But making a real impact is about more than just writing a check. A sharp advisor weaves your charitable goals right into your financial plan, making sure your generosity is both meaningful and smart from a tax perspective.

The goal is to create a charitable giving strategy that not only supports the causes you care about but also enhances your family's overall financial picture. This turns philanthropy from an expense into a powerful planning tool.

This could mean setting up a Donor-Advised Fund (DAF), creating a private foundation, or gifting appreciated assets to charities to completely sidestep capital gains taxes. A big piece of securing your financial future involves using effective strategies for minimizing taxes in retirement, and smart charitable planning is a major part of that equation. These advanced techniques ensure your contributions make the biggest difference possible.

The Importance of a Succession-Ready Firm

When you have substantial assets, the continuity of the advice you receive is just as important as the quality of it. You need a team that will be there not just for you, but for your children and even your grandchildren. This puts the advisor’s own business planning under a microscope.

The wealth management industry is staring down a massive talent shortage. Research shows an estimated 110,000 advisors—that's 38% of the entire workforce—are expected to retire in the next decade. For clients who need long-term stability, this is a huge red flag. It highlights how crucial it is to partner with a firm that has a solid succession plan. You can discover more insights about this trend from McKinsey & Co.'s analysis, which explains why the best firms are already investing heavily in the next generation of talent.

Choosing a firm with a deep bench of professionals means your family’s financial strategy won't get derailed when your primary advisor decides to retire. It’s about the peace of mind that comes from knowing your legacy is in the hands of a durable, multi-generational team.

Essential Questions to Ask Your Potential Advisor

Picking a retirement financial advisor is one of the biggest money decisions you’ll ever make. This isn't just about hiring someone to manage a portfolio; you're choosing a long-term partner who will help guide your financial life for decades. To get it right, you need to ask questions that go deeper than the surface to really understand their philosophy, how they operate, and what they’ve actually accomplished for people like you.

Think of this as your vetting guide. Armed with the right questions, you shift from being a passive client to an informed partner in your own future, ready to find someone who genuinely gets your vision for retirement.

Understanding Their Philosophy and Process

First things first, you need to get a handle on how an advisor thinks. Their investment philosophy is the bedrock of every single recommendation they will ever make, so it absolutely has to line up with your own goals and comfort for risk. If you get vague, canned answers here, that's a huge red flag.

Kick things off with these foundational questions:

- What is your investment philosophy? A good answer will be clear and straightforward. Do they believe in passive index funds, active stock picking, or some combination? More importantly, they should be able to explain why they take that approach with confidence and real-world reasoning.

- Are you a fiduciary, and will you state that in writing? This is a dealbreaker. A fiduciary is legally bound to act in your best interest, period. Anything less than an immediate, unequivocal "yes" is your cue to walk out the door.

- How do you and your firm get paid? You need total transparency here. Ask them to lay out their fee structure—is it fee-only, fee-based, or commission-based? Understand exactly how their compensation could influence the advice they give you. For truly unbiased advice, a fee-only fiduciary is widely considered the gold standard.

Assessing Their Experience and Specialization

Let's be clear: not all advisors are the same. You need someone who has spent years helping clients in your specific situation. A generalist might be fine for simple cases, but they often lack the nuanced knowledge needed for the complex challenges that come with retirement, especially for high-net-worth families.

Drill down into their actual expertise with these questions:

- Who is your typical client? Listen closely. You want to hear a description that sounds a lot like you. Do they work with executives managing concentrated stock positions, business owners planning an exit, or families focused on multi-generational wealth?

- What is the biggest challenge you’ve helped a client like me overcome? This question cuts through the theory and gets to real-world results. Their answer will tell you a lot about their problem-solving skills and whether they have hands-on experience with the issues that keep you up at night.

- What is your firm’s succession plan? With nearly 40% of advisors expected to retire in the next decade, this is more important than ever. You’re building a long-term relationship. A solid firm will have a clear continuity plan to ensure your family’s financial strategy doesn’t get disrupted when your advisor decides to hang it up.

A great advisor won't just manage your portfolio. They become your financial quarterback, proactively watching over your entire financial picture and giving you the peace of mind that comes from knowing an expert is in your corner.

For a more exhaustive list of questions to ask, be sure to check out our complete guide on what to look for in a financial advisor. It will help you cover all your bases so you can make a confident, well-informed decision.

How Technology Shapes Modern Retirement Advice

If you picture a retirement advisor sitting behind a mahogany desk with a paper ledger, you’re about 30 years out of date. The best advisors today pair decades of hard-won human experience with powerful technology to get better, data-driven results for their clients.

This tech-forward approach isn't about replacing human judgment; it's about making it sharper. By embracing sophisticated tools, a modern advisor can offer a level of detail, foresight, and clarity that was simply impossible before, giving you the kind of direct, efficient service that sophisticated clients rightly expect.

Dynamic Projections and Real-Time Planning

One of the biggest shifts has been the move from static, paper-based plans to dynamic, digital ones. Modern financial planning software lets an advisor create interactive retirement projections that you can explore together in real time.

Think of it as a financial flight simulator. You and your advisor can instantly model different scenarios and see the outcome:

- What happens if you decide to retire two years earlier than planned?

- How does a major purchase, like a vacation home, ripple through your long-term income?

- What’s the real impact of a market downturn in your first five years of retirement?

This turns your retirement plan from a rigid document gathering dust in a drawer into a living, adaptable strategy. It lets you make proactive adjustments and gives you a crystal-clear understanding of how today's decisions will shape your financial reality decades from now.

Leveraging AI and Data for Deeper Insights

Beyond just projections, technology helps a skilled retirement financial advisor put your portfolio through its paces. Sophisticated analytics can simulate thousands of different market scenarios, uncovering potential weak spots in your strategy long before they become real-world problems. This isn't about being pessimistic; it's about building a plan that's resilient, not just optimistic.

The industry is moving quickly to adopt these tools. Artificial intelligence is now the top technology priority for advisors, with 35% flagging it as the primary area for their firm’s investment. They see huge potential in using AI for everything from personalized client communication to spotting new opportunities. You can dig into the full details on these industry trends in the latest J.D. Power U.S. Financial Advisor Satisfaction Study.

Technology also brings everything together in one place. Modern client portals and dashboards provide a clear, consolidated view of your entire financial picture—from investment accounts to real estate holdings—updated daily.

This transparency empowers you. It eliminates guesswork and ensures you always have a precise, up-to-date handle on your net worth and how you're tracking toward your goals. When you're vetting an advisor, look for a firm that has clearly committed to this kind of innovation. It's often a direct reflection of their commitment to providing exceptional, data-informed service.

Common Questions People Have About Retirement Financial Advisors

You've read up on what a retirement advisor does, but let's be honest—the practical questions are probably still swirling. Here are some straightforward answers to the things people really want to know before they hire someone to manage their life's savings.

Is a Retirement Specialist Really That Different?

What’s the real difference between a retirement advisor and the person who helped you grow your 401(k)? Think of it like a doctor. Your general practitioner is great for your overall health, but for heart surgery, you want a cardiac specialist.

It's the same in finance. A general advisor is fantastic at helping you build wealth—the "accumulation" phase. But a retirement specialist is an expert in the trickier "decumulation" phase. This is the art of turning a big pile of assets into a steady, reliable paycheck that lasts the rest of your life. They live and breathe things like tax-efficient withdrawal strategies, squeezing every last dollar out of Social Security, and making sure your estate plans are buttoned up. It's a completely different skillset.

So, when do you need this specialist? While there's no magic number, the game really changes when you're working with $1 million or more in investable assets. At that level, the financial puzzle gets much more complex. You’re not just drawing down savings; you’re navigating advanced tax planning, coordinating with trust attorneys, and maybe even managing a large chunk of company stock. This is where a specialist’s focused expertise really pays off.

It's not just about the numbers. A study from Vanguard found the top reason people seek financial advice is for "peace of mind." They want to know a pro is watching over their situation and is legally bound to act in their best interest.

How Often Will I Actually Talk to My Advisor?

This is a big one. You're handing over a lot of trust (and money), so you shouldn't be left in the dark. A good advisor sets a clear communication rhythm right from the start.

Here’s what you should expect, at a minimum:

- Deep-Dive Reviews: At least once or twice a year, you should have a comprehensive meeting to go over your entire financial picture—every account, every goal, and your progress.

- Regular Check-Ins: Expect quarterly calls or updates to keep you in the loop on any minor portfolio adjustments or to give you their take on what the market is doing.

- Proactive Outreach: They should be calling you when the market goes haywire or if a big life event—like a change in tax law—affects your plan.

The relationship should feel proactive, not reactive. If the only time you hear from them is when you call with a question, that's a red flag. Consistent, ongoing dialogue is what keeps your financial strategy perfectly aligned with your life, year after year.

At Commons Capital, we provide the specialized guidance needed to navigate the complexities of retirement with confidence. Schedule a consultation with our team today.