Retirement planning for business owners is a different ballgame. Your personal financial security is often tied directly to your company's success, making it critical to build a strategy that separates your personal wealth from your business operations. A solid strategy for retirement planning for business owners ensures the future you've worked for is as successful as the business you built.

This guide provides a comprehensive look at the unique challenges entrepreneurs face and the key steps to secure a comfortable retirement.

Why Retirement Planning Is Different for Entrepreneurs

For most people, retirement planning means contributing to a 401(k) or an IRA. Simple enough. But for a business owner, the lines are completely blurred.

Your company often represents your largest asset, your primary source of income, and your life's work all rolled into one. This unique situation creates a specific set of challenges that traditional employees never face. The very nature of entrepreneurship often works against conventional retirement saving habits. Every spare dollar gets reinvested back into the business to fuel growth, leaving personal savings as an afterthought. This common practice can lead to a dangerous financial situation where you are asset-rich on paper but cash-poor when it comes time to step away.

The Asset-Rich, Cash-Poor Dilemma

Many successful founders find themselves approaching their 60s with a valuable company but very little in liquid retirement accounts. The assumption is that selling the business will fund their entire retirement. That's a huge gamble.

This all-in strategy is risky and overlooks several key factors:

- Market Volatility: The value of your business can swing wildly based on economic conditions, industry trends, and other factors completely outside your control.

- Finding a Buyer: A successful sale isn't guaranteed. It requires finding the right buyer at the right time and navigating incredibly complex negotiations.

- Emotional Attachment: After pouring years of your life into a company, the psychological difficulty of letting go can be a significant and unexpected hurdle.

This dependence on a single asset—the business—creates immense pressure. A well-structured retirement plan mitigates this risk by building wealth outside of the company. You can explore a more detailed breakdown of this in our guide to financial planning for business owners.

The goal is to build a financial life that can thrive independently of your business's daily operations or eventual sale. This separation is the cornerstone of a secure retirement for any entrepreneur.

Overlooking Personal Savings Is a Common Trap

The intense focus required to build a successful company means personal financial planning can easily fall by the wayside. Shocking new data highlights this trend: nearly 1 in 5 business owners have no retirement savings at all.

Even more concerning, 14% of entrepreneurs recently tapped into their personal retirement funds to support their business, further blurring the lines between personal and company assets. You can discover more insights about this growing issue in this report on the entrepreneur retirement crisis.

Understanding these unique challenges is the essential first step toward creating a robust and resilient financial future.

Selecting the Right Retirement Plan for Your Company

Picking the right retirement plan is one of the most powerful strategic moves you can make as a business owner. This isn't just about stashing away money for the future; it's a critical tool for slashing your taxable income, building personal wealth outside of your company, and winning the war for top-tier talent.

The options can feel a bit overwhelming at first, but they really boil down to your company's size, the consistency of your cash flow, and how aggressively you want to save. For most entrepreneurs, the best choice is usually one of a few popular, low-admin plans that pack a serious punch without the complexity of a massive corporate structure.

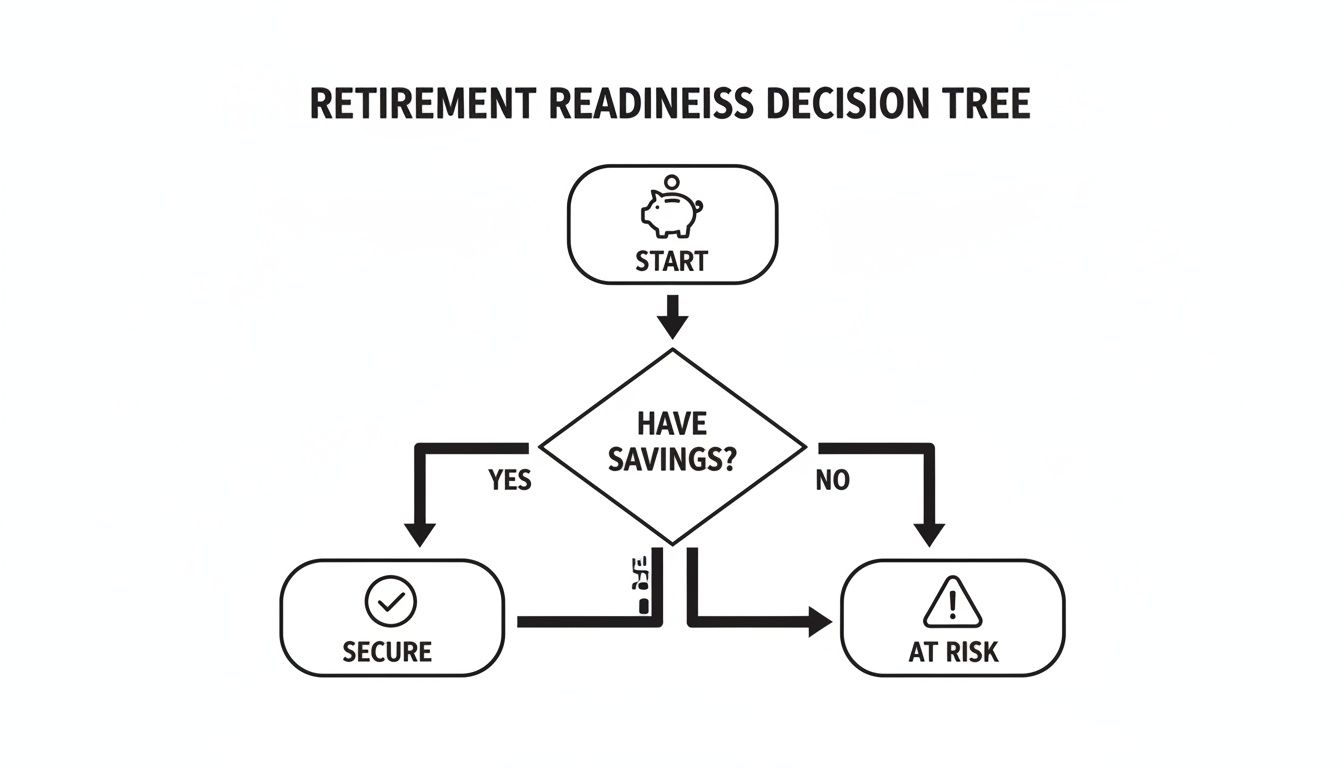

This decision tree is a great visual for where most people stand.

It highlights a fundamental truth: a dedicated savings plan is the line in the sand separating those who are prepared from those who are at risk.

The Best Plans for Solopreneurs and Small Teams

If you're self-employed or have just a few employees, three plans consistently rise to the top for their simplicity and high contribution limits. Each one serves a slightly different need.

- SEP IRA (Simplified Employee Pension): This is often the go-to for its incredible flexibility. Only the employer (you) contributes, up to 25% of compensation, capped at $69,000 in 2024. It's perfect for freelancers and consultants with lumpy income because you decide how much to put in each year. You can even skip a year if cash is tight.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): Think of this as a 401(k)-lite. It's built for small businesses (under 100 employees) that want to offer a solid retirement benefit to attract and keep good people. It requires you to make a small match, but the administrative load is far lighter than a full-blown 401(k).

- Solo 401(k): This plan is an absolute powerhouse for an owner-only business (or you and your spouse). You get to contribute as both the "employee" and the "employer," which lets you stash away a huge amount of money—often hitting the $69,000 max for 2024 (plus catch-up contributions if you're over 50). It also allows for plan loans and Roth contributions, adding some valuable flexibility.

A key takeaway for entrepreneurs is that you don't have to start with a complex plan. A SEP IRA or Solo 401(k) can be set up in minutes and allows you to put away tens of thousands of dollars in pre-tax savings annually.

To make the decision a bit easier, here’s a quick breakdown of how these plans stack up against each other.

Comparing Retirement Plans for Business Owners

This table should give you a solid starting point for figuring out which lane you belong in. The right choice depends entirely on your specific goals and business structure.

Advanced Options for High-Income Earners

Once your business is more mature and spitting out serious cash flow, it might be time to graduate to a more sophisticated plan. These come with more rules but let you save far more than the standard options.

A Defined Benefit Plan is basically a traditional pension you create for yourself. It allows for massive, tax-deductible contributions that can easily exceed $100,000 a year, depending on your age and income. This is the ultimate "catch-up" tool for established owners looking to supercharge their savings in just a few years. The tradeoff? They come with rigid funding rules and higher administrative costs.

For larger, growing companies, a Traditional or Safe Harbor 401(k) is the gold standard. It offers higher employee contribution limits than a SIMPLE IRA, options for profit sharing, and vesting schedules to encourage your best people to stick around. The admin is more involved, but as a tool for attracting and retaining talent, it's unmatched.

Choosing the right structure isn't just a box to check—it’s a foundational piece of your entire financial puzzle. It will directly shape your tax strategy, your ability to build personal wealth, and your company's competitive edge.

Designing a Profitable Business Exit Strategy

For most entrepreneurs, a great retirement hinges on a great exit. Your business is probably your single largest asset, and how you strategically unlock its value will define your financial future.

Many owners treat their exit as a distant, one-off event. The smart approach is to think of it as an essential, ongoing business process. This shift in mindset changes everything. You stop waiting until you're ready to retire to think about selling, and instead, you start building a company that’s attractive to buyers from day one. It not only sets you up for a much bigger payday but also makes your business stronger right now.

Unfortunately, this forward-thinking approach isn't the norm. There are serious gaps in retirement preparedness out there. Roughly half of all business owners have no formal exit strategy. Among those without a documented plan, a surprising 37% still plan to exit within the next decade, which is a recipe for potential headaches. You can see more on this from a 2025 business owner survey.

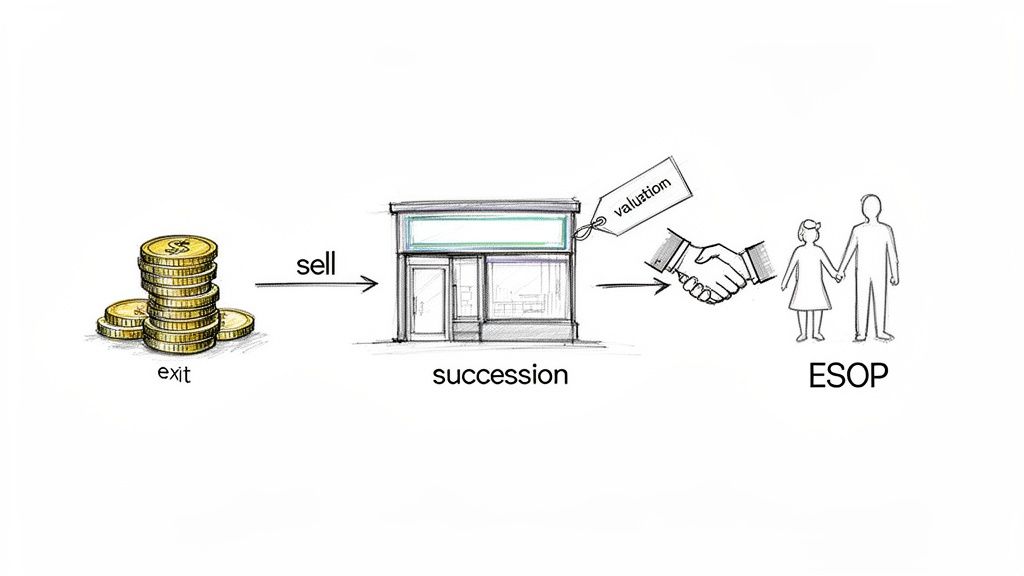

Exploring Your Primary Exit Pathways

When it's time to transition out of your business, you've got a few well-traveled roads to choose from. Each one has its own financial implications, timelines, and levels of complexity. Getting your head around these options early is a cornerstone of solid retirement planning for business owners.

- Third-Party Sale: This is the classic exit—selling your company to an outsider, whether that's an individual, a strategic competitor, or a private equity firm. This route usually offers the cleanest break and the biggest potential for a major liquidity event.

- Family Succession: Passing the torch to the next generation can be incredibly rewarding, but it's also packed with unique emotional and financial hurdles. Structuring this kind of transition requires careful estate planning to keep things fair and ensure the business doesn't skip a beat.

- Management or Key Employee Buyout: Selling to your trusted leadership team can be a great way to preserve the company’s culture and legacy. These deals are often financed over time, either through seller financing or bank loans, giving you a steady income stream in retirement.

- Employee Stock Ownership Plan (ESOP): An ESOP is a type of retirement plan that buys the company and holds its stock in trust for employees. It can be a highly tax-efficient way to sell your business gradually while rewarding the very people who helped you build it.

The right path for you depends entirely on your personal goals, your financial needs, and the kind of business you've built. There’s no one-size-fits-all answer here.

The Critical Role of a Professional Valuation

One of the biggest mistakes entrepreneurs make is guessing what their business is worth. Any exit planning you do is built on a foundation of sand without a formal, professional valuation. Getting a realistic assessment of your company's value is non-negotiable.

A professional valuation does more than just give you a number; it provides a detailed roadmap of your company's strengths and weaknesses from a buyer's perspective. It highlights areas for improvement that can dramatically increase your final sale price.

Think of it as a financial physical for your business. An appraiser will dig into everything—your financials, customer concentration, the strength of your management team, your position in the market. Understanding these factors is the first real step toward making your business more valuable. For a deeper dive, check out our guide on how to value your business.

What Buyers Truly Look For

At the end of the day, potential buyers—whether they're private equity firms or strategic acquirers—are looking for one thing: predictable, sustainable cash flow. They want to see a business that doesn't depend on you, and only you, to run.

Here are the key things that make a business irresistible to a buyer:

- Recurring Revenue: Subscription models, long-term contracts, and a loyal customer base are gold. They signal stability.

- A Strong Management Team: Buyers are purchasing a functioning system, not just a pile of assets. A capable team that can run the show without you is a massive selling point.

- Clean Financials: Clear, well-organized, and accurate financial records build trust and make the due diligence process a breeze. Messy books are a huge red flag.

- Diversified Customer Base: If a single client accounts for more than 15-20% of your revenue, that introduces significant risk that will absolutely devalue your company.

- Documented Systems and Processes: You have to prove that your business operations are systematic and repeatable. It shows a buyer that the "secret sauce" isn't just stuck in your head.

Structuring a deal to maximize what you take home involves more than just the sale price. It’s also about negotiating the right terms, managing the tax hit, and planning for what comes next. A well-designed exit strategy is your best guarantee that you won't leave money on the table and can smoothly convert years of hard work into a secure, comfortable retirement.

Separating Your Personal and Business Finances

One of the first—and biggest—mistakes business owners make is blurring the line between their personal and business finances. It’s an easy trap to fall into. When your personal checking account doubles as the company’s petty cash drawer, you create a tangled mess that’s a nightmare to unwind.

This isn’t just about messy bookkeeping. It complicates your taxes, puts your personal assets on the line, and makes true retirement planning nearly impossible. Building a financial firewall between you and your business isn’t just good accounting; it’s a non-negotiable step toward a secure future. It all starts with a simple mindset shift: start treating yourself like your most valuable employee. That means paying yourself a consistent, reasonable salary—not just dipping into the business account whenever the balance looks healthy. This simple discipline forces you to live on a predictable income, just like your team, and draws a clear boundary between company cash and your own money.

That steady paycheck is the foundation. It allows you to build a personal financial life that can stand on its own, separate from the day-to-day ups and downs of the business.

Building Your Financial Firewall

Putting this separation into practice requires a few deliberate actions. It’s really about creating systems that force good financial habits, protecting you from the temptation to co-mingle funds when cash gets tight.

Here are the foundational steps every single business owner needs to take:

- Open Separate Bank Accounts: This is the absolute baseline. You need a dedicated business checking account for all revenue and expenses, period. Your salary gets deposited from there into your personal account. Never, ever pay for groceries or a family vacation directly from the business account.

- Establish Separate Credit Lines: Get a business credit card and use it for all company-related purchases. This does more than just simplify expense tracking for your accountant; it helps build your company's credit history. That can be a lifesaver when you need financing without putting up a personal guarantee.

- Formalize Your Salary: Sit down with your CPA and figure out what constitutes "reasonable compensation" for your role in the company. Then, pay yourself that salary through a formal payroll system, complete with tax withholding. It legitimizes your income and keeps you clear of potential red flags with the IRS.

By putting these basic structures in place, you start building personal assets that are shielded from business liabilities. You're creating a safety net that protects your family and ensures your retirement savings aren't the first line of defense if the company hits a rough patch.

Why a Diversified Personal Portfolio Matters

Once you have that steady salary coming in, the next move is to aggressively build a personal investment portfolio that has nothing to do with your company. The whole point is to make sure your retirement isn't riding entirely on the future sale of your business.

For so many entrepreneurs, their business is their retirement plan. This is an incredibly risky approach. A downturn in your industry, a bad market, or a failed sale could wipe out decades of your hard work in an instant.

A diversified portfolio is your hedge against that risk. It lets you grow wealth across different asset classes—public stocks, bonds, real estate, you name it. This strategy gives you financial security, but just as importantly, it gives you flexibility.

The Freedom of Financial Independence

Having substantial personal assets gives you options. You won't be forced to sell your business at a bad time just because you need the cash to retire. You can afford to wait for the right market conditions and the right buyer, maximizing the value you’ve spent your life creating.

This financial independence also dials down the personal stress. Knowing your family’s future and your own retirement are secure, no matter what happens with the business tomorrow, allows you to lead with more confidence and clarity. This is the discipline that separates a stressful, uncertain exit from a confident and profitable one. It’s the final, critical piece that ensures the wealth you’ve generated in your business actually translates into a comfortable and well-funded retirement.

Advanced Wealth and Estate Planning Strategies

Once your business is throwing off consistent cash and you're hitting the contribution limits on your standard retirement accounts, the game changes. Your planning has to evolve. The focus shifts from just piling up money to strategically protecting it, growing it, and making sure it gets to the next generation.

This is where the more sophisticated side of wealth and estate planning kicks in, using tools built for successful entrepreneurs. We're moving beyond basic savings and into the world of trusts, smart philanthropy, and building a real legacy. It's all about making sure the wealth you’ve spent a lifetime building is preserved and goes exactly where you want it to, shielded from unnecessary taxes, creditors, and legal headaches.

Using Trusts for Asset Protection and Tax Efficiency

For a business owner, trusts are one of the most powerful tools in the playbook. They can do things a simple will just can't, giving you control over your assets, slashing potential estate taxes, and protecting your legacy from threats down the road.

An irrevocable trust, for example, can be a total game-changer. When you move assets into this kind of trust, they are legally no longer part of your personal estate. That’s huge for two reasons: first, those assets are generally shielded from future creditors or lawsuits. Second, they aren't subject to estate taxes when you pass away—and with federal rates as high as 40% for large estates, that's a massive saving. This is especially critical if you're planning to pass on a valuable business. Instead of leaving the company directly to your kids and triggering a potentially massive tax bill, placing it in a trust can ensure a much smoother, more tax-efficient handover.

The Foundation: Wills and Trusts

While these advanced techniques are powerful, they have to be built on a solid foundation. As you start thinking about the long-term plan, getting fundamental legal documents like Wills and Trusts in place is non-negotiable. Think of these as the instruction manual for your estate, spelling out exactly how your assets—both business and personal—are managed and distributed.

Without them, the state decides for you. That means a long, public, and often expensive probate process that can drain your estate's value and create a lot of friction for your family. A well-drafted plan keeps you in the driver's seat.

Many people think trusts are only for the super-rich. The reality is, for any business owner with a valuable company and personal real estate, a trust is a fundamental tool for avoiding probate and protecting what you've built for your loved ones.

Weaving Charitable Giving into Your Plan

Smart philanthropy isn't just about feeling good; it's a key part of advanced planning that comes with some serious tax benefits. Instead of just writing checks, you can use more structured approaches to get more bang for your buck and lower your tax bill at the same time.

Here are a couple of popular strategies:

- Donor-Advised Funds (DAFs): This is like having your own charitable savings account. You can contribute cash, stock, or even shares of your private business, and you get an immediate tax deduction for the full market value. Then, you can recommend grants to your favorite charities over time. This is an incredibly useful move in a high-income year, like when you sell your business.

- Charitable Remainder Trusts (CRTs): With a CRT, you can donate highly appreciated assets (like company stock) to a trust. The trust then pays you an income for a set period, and whatever is left—the "remainder"—goes to charity after you're gone. This technique lets you turn a highly appreciated asset into income without getting hit with an immediate capital gains tax.

These strategies let you support the causes you believe in while also serving as powerful tools in your financial plan. They can shrink your taxable estate and help you create a legacy that lasts.

Building Your Team of Professional Advisors

Successfully planning your retirement as a business owner isn’t something you do alone. The smartest entrepreneurs learn sooner or later—you can't be an expert in everything. Thinking of a team of specialized advisors as a luxury is a mistake. It’s a strategic necessity.

This team gives you a 360-degree view of your entire financial picture. They make sure your business moves, tax strategy, and personal wealth goals are all pulling in the same direction. Without that coordinated advice, you’re flying blind, risking costly mistakes and leaving opportunities on the table.

Assembling Your Core Advisory Board

Think of this group as your personal board of directors, dedicated to your long-term financial success. Each member brings a different, critical skill to the table. Their real power comes from working together.

Here are the key players you need in your corner:

- Certified Financial Planner (CFP): This is your quarterback. A great CFP pulls all the pieces together—investments, retirement accounts, insurance, and even cash flow. They’re the one who makes sure your exit plan actually funds the retirement you want.

- Certified Public Accountant (CPA): Your CPA needs to be more than just a tax preparer; they should be your tax strategist. They’ll help structure your business and personal finances to lighten your tax load, both today and when you eventually sell.

- Estate Planning Attorney: This is the professional who drafts the ironclad documents—wills, trusts, powers of attorney—that protect your legacy. For a business owner, their role is non-negotiable for creating a succession plan that keeps your assets out of probate and away from unnecessary estate taxes.

- Business Broker or M&A Advisor: When it’s time to sell, you need a specialist. These advisors guide you through the entire process, from valuing the company to finding qualified buyers and negotiating a deal that maximizes what you walk away with.

The Power of Coordinated Advice

Having these experts on call is one thing. Getting them to actually talk to each other is where the magic happens. Your financial life is all connected. A decision about your exit strategy has huge tax implications (hello, CPA), directly impacts your retirement income (your CFP’s territory), and needs to be baked into your estate plan (a job for your attorney).

When these pros work in silos, you get confusing advice and less-than-ideal results. The best advisory teams communicate. You should absolutely encourage them to collaborate on big decisions.

For example, when looking at advanced tax strategies around your exit, knowing how to hire a CPA who is willing to get on the phone with your other advisors is crucial. A proactive CPA who actually talks to your financial planner can save you a fortune.

What to Ask Potential Advisors

Finding the right people goes beyond just credentials on a wall. You're looking for partners who get the entrepreneur's mindset. They need to understand that your business isn't just an asset on a spreadsheet—it's your life's work.

When you’re interviewing advisors, get specific. Ask them about their experience with business owners like you. Say, "Tell me about a case similar to mine and how you helped that client through their retirement transition." Their answer will tell you everything you need to know about their real-world expertise.

Ultimately, you need people who have deep technical knowledge and who operate as fiduciaries, meaning they are legally bound to put your interests first. For a deeper dive on this, check out our guide on choosing the right retirement financial advisor.

Putting this team together is a direct investment in your future. It provides the clarity you need to turn the wealth locked up in your business into a secure and fulfilling retirement.

At Commons Capital, we specialize in helping successful business owners navigate these complex financial decisions. If you're ready to build a comprehensive retirement plan that aligns your business success with your personal goals, we invite you to connect with our team. Learn more at https://www.commonsllc.com.