In an ever-changing economic landscape, establishing a durable financial foundation is more critical than ever. For high-net-worth families, the challenge extends beyond simple savings; it involves sophisticated strategies for wealth preservation, growth, and multi-generational stewardship. This guide moves beyond generic advice to provide a definitive framework of principles designed for complex financial situations.

We will explore 10 rock solid financial rules to live by for families, offering actionable insights that address everything from tax-optimized budgeting to comprehensive estate planning. These rules are the cornerstones used by successful families to build not just wealth, but a lasting legacy grounded in shared values and financial discipline. For affluent individuals, entrepreneurs, and retirees, mastering these concepts is not just about accumulation but about creating a resilient financial structure that can withstand market volatility and adapt to future needs.

This article provides a clear, actionable roadmap. You will learn how to implement a family financial constitution, optimize your tax strategies through strategic giving, and establish a disciplined investment policy. We will also cover the nuances of succession planning and the importance of maintaining open communication about financial matters across generations. To truly build a lasting financial legacy, families should investigate practical strategies and solutions for wealth protection to secure their assets against unforeseen risks. By implementing these proven strategies, you can navigate financial complexities with confidence, protect your assets, and ensure your family's prosperity for generations to come.

1. The 50/30/20 Budget Framework with Tax Optimization

A cornerstone of sound financial planning, the 50/30/20 rule provides a clear and balanced structure for managing after-tax income. This framework, popularized by figures like Elizabeth Warren, suggests allocating 50% to essential Needs, 30% to discretionary Wants, and a crucial 20% to Savings and Debt Repayment. For affluent families, this isn't just a budgeting tool; it's a strategic starting point for sophisticated wealth management and one of the most foundational rock solid financial rules to live by for families.

Elevating the Framework with Tax Efficiency

High-net-worth families can amplify the power of the 20% savings allocation by integrating tax optimization. The goal is to make every dollar saved work harder by minimizing tax drag and leveraging government-incentivized growth.

A family with a $500,000 annual after-tax income would allocate $250,000 to needs (mortgage, property taxes, insurance), $150,000 to wants (travel, dining, hobbies), and $100,000 to their savings strategy. Instead of simply placing this $100,000 in a standard brokerage account, they deploy it strategically. This includes maxing out 401(k)s and backdoor Roth IRAs for all eligible family members, fully funding Health Savings Accounts (HSAs) for triple tax benefits, and contributing generously to 529 plans for tax-free educational funding.

Actionable Implementation Steps

To effectively implement this enhanced framework, consider these practical steps:

- Automate Your Allocations: Set up automatic transfers from your primary checking account to designated savings, investment, and spending accounts immediately after receiving income. This enforces discipline and ensures your savings goals are prioritized.

- Conduct Quarterly Reviews: Life and financial situations change. A quarterly review with your wealth advisor allows you to adjust allocations based on new income streams, changing expenses, or evolving family goals like a new business venture or property acquisition.

- Involve the Family: Foster transparency and shared responsibility by including your spouse and older children in budgeting discussions. This creates buy-in and helps instill sound financial habits in the next generation.

- Leverage Professional Guidance: Work with a financial advisor to identify the most tax-efficient vehicles within each category. They can help navigate complex options like donor-advised funds for philanthropic goals or specialized trusts for estate planning, ensuring every allocation is optimized.

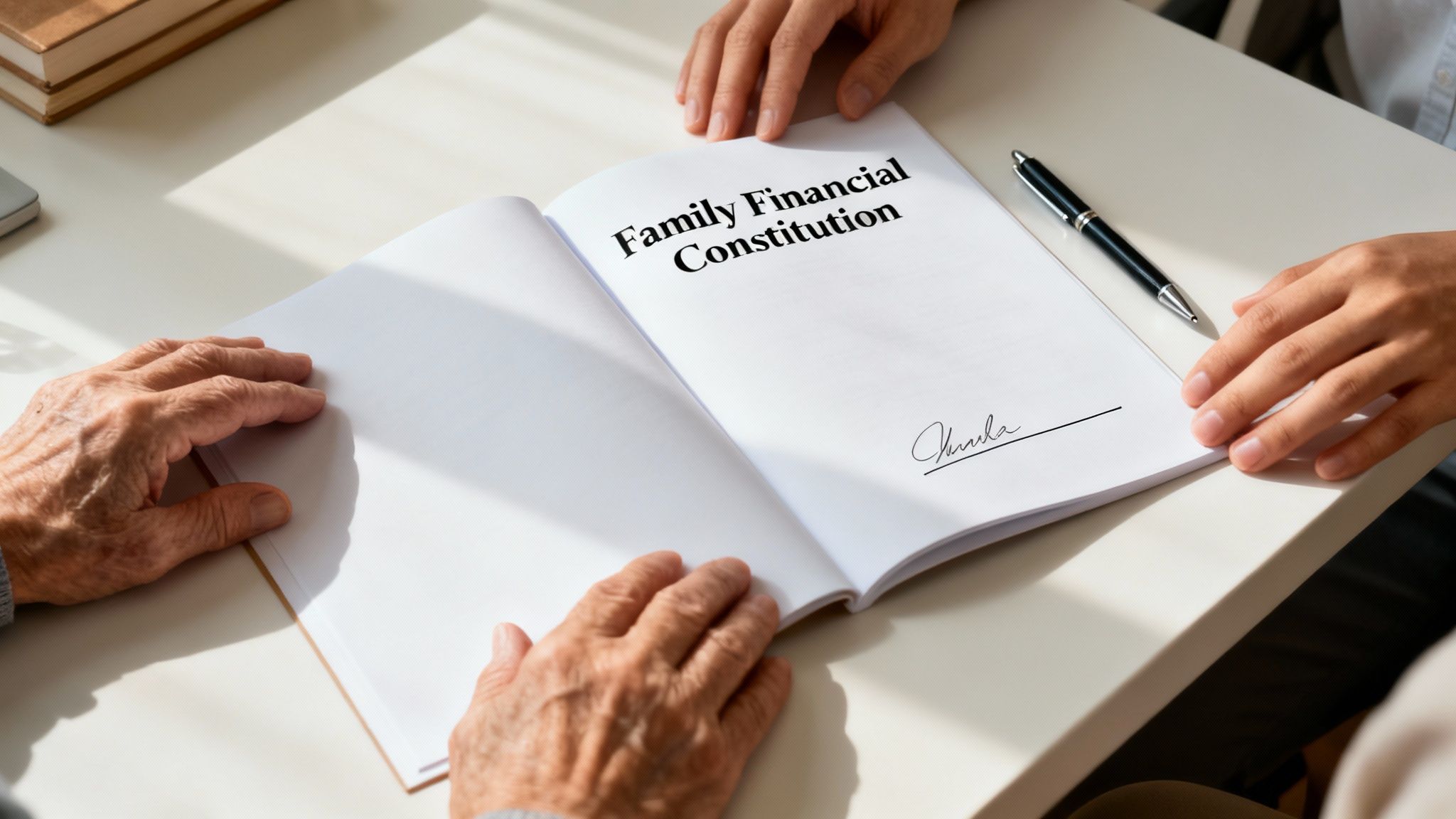

2. Establish a Family Financial Constitution and Values Statement

Moving beyond individual budgets, a Family Financial Constitution is a formal governance document that codifies a family’s shared values, financial philosophy, and decision-making processes. This foundational document, advocated by family wealth experts like Roy Williams and Vic Preisser, transforms abstract principles into concrete guidelines. It outlines everything from investment risk tolerance and charitable giving strategies to rules for family business succession, ensuring clarity and continuity across generations. For affluent families managing complex assets, this is one of the most critical rock solid financial rules to live by for families.

Elevating Governance with a Formal Framework

A Family Constitution acts as a strategic roadmap, preventing conflicts and preserving wealth by aligning stakeholders on key issues before disputes arise. Its power lies in its proactivity and comprehensive nature. It’s the difference between navigating a crisis with a pre-agreed plan versus making emotional decisions under pressure.

For example, a family with a significant real estate portfolio and a family-operated business might use their constitution to stipulate the criteria for family members entering the business, the process for liquidating shared assets, and the framework for distributing profits. This documented approach, similar to the multi-generational governance structures of families like the Rockefellers, provides a clear, objective system for managing wealth and legacy, preventing misunderstandings that can erode both capital and relationships.

Actionable Implementation Steps

To create a robust and effective Family Constitution, follow these steps:

- Involve All Stakeholders: Convene a family meeting including all relevant adult members to discuss core values and long-term goals. Inclusive development ensures widespread buy-in and a document that truly reflects the family's collective vision.

- Be Specific and Measurable: Avoid vague statements. Instead of "we value education," specify "the family will fund 50% of tuition for post-graduate degrees in approved fields for direct descendants who maintain a 3.5 GPA."

- Engage Professional Guidance: Work with a family governance advisor or an estate planning attorney. These professionals can facilitate difficult conversations, provide legal structure, and ensure the document is both comprehensive and legally sound.

- Schedule Regular Reviews: A constitution is a living document. Plan to formally review and update it every 3-5 years, or after major life events like a marriage, birth, or sale of a business, to ensure it remains relevant to the family's evolving circumstances.

3. Maintain an Emergency Fund Equal to 6-12 Months of Expenses for High-Net-Worth Families

While conventional wisdom often suggests a three-to-six-month emergency fund, high-net-worth families require a more robust financial safety net. Extending this reserve to cover 6 to 12 months of living expenses provides a critical buffer against the unique risks associated with complex financial portfolios, illiquid investments, and business ownership. This expanded fund isn't just about covering job loss; it's a strategic tool to prevent the forced liquidation of assets during market downturns, ensuring long-term wealth preservation and making it one of the most vital rock solid financial rules to live by for families.

A Strategic Asset Protection Tool

For affluent families, a larger emergency fund protects against more than just income disruption. It provides the liquidity needed to navigate capital calls for private investments, unexpected tax liabilities, or sudden business opportunities without derailing a meticulously planned investment strategy. It creates a firewall between personal liquidity and business or investment capital.

Consider a family with annual living expenses of $400,000. A 12-month emergency fund of $400,000 held in liquid, safe assets means they can weather a significant business downturn or a volatile market period without selling their equities at a loss or tapping into their core investment portfolio. This financial stability provides peace of mind and preserves their wealth-building momentum.

Actionable Implementation Steps

To build and manage this crucial reserve effectively, consider these steps:

- Implement a Tiered Liquidity Strategy: Structure your fund for both accessibility and yield. Keep one to two months of expenses in a high-yield savings account for immediate access. Place the remainder in low-risk, liquid vehicles like short-term Treasury bills or money market funds to earn a better return while maintaining safety.

- Establish a Separate Account: House your emergency fund in a dedicated account, completely separate from your daily operating or investment accounts. This psychological and physical separation prevents you from casually dipping into the funds for non-emergency spending.

- Automate and Rebalance: Set up automatic monthly transfers to build the fund to its target. If you use the fund for a true emergency, create a plan to replenish it immediately. Review the fund's size annually to ensure it still aligns with your current lifestyle and expenses.

- Consult Your Advisor: Work with your financial professional to determine the optimal size and allocation for your family's specific situation. They can help you balance the need for liquidity with the goal of minimizing cash drag on your overall net worth.

4. Implement Tax-Loss Harvesting and Strategic Charitable Giving Programs

A sophisticated approach to wealth management involves not just growing assets, but actively minimizing tax drag. Combining tax-loss harvesting with a strategic charitable giving program creates a powerful synergy, allowing families to reduce their tax burden, support causes they care about, and optimize their overall portfolio. This dual strategy is a cornerstone financial rule for families looking to maximize the impact of every dollar.

Elevating the Framework with Tax Efficiency

This strategy involves systematically selling investments at a loss to offset capital gains taxes. When paired with philanthropy, the benefits multiply. Instead of donating cash, families can contribute highly appreciated securities to vehicles like a Donor-Advised Fund (DAF). This allows them to potentially avoid capital gains taxes on the appreciated asset while receiving a fair market value tax deduction for the contribution.

For example, a family can harvest $50,000 in losses from their portfolio in December to offset $50,000 in gains realized earlier in the year, effectively neutralizing the tax liability. Simultaneously, they can donate $100,000 of appreciated stock (with a cost basis of $20,000) to their DAF, avoiding the taxes on the $80,000 gain and receiving a full $100,000 charitable deduction. This coordinated maneuver significantly enhances both their investment and philanthropic outcomes.

Actionable Implementation Steps

To effectively integrate these powerful tax strategies, consider these practical steps:

- Establish a Formal Review Calendar: Schedule quarterly or at least annual reviews with your financial and tax advisors specifically to identify tax-loss harvesting opportunities. This disciplined approach prevents missed chances to offset gains.

- Coordinate Investment and Philanthropic Goals: Work with your advisor to identify which appreciated assets are best suited for charitable contributions. This ensures you are maximizing tax benefits while funding your philanthropic mission without disrupting your core investment allocation.

- Maintain Meticulous Records: Tax-loss harvesting is subject to complex IRS regulations, including the "wash sale" rule. Ensure you or your advisor meticulously document all transactions, including cost basis and sale dates, to maintain full compliance.

- Leverage Professional Expertise: The nuances of executing these strategies require professional guidance. A wealth advisor can help you navigate wash sale rules by reinvesting in similar but not "substantially identical" securities and can structure complex donations through charitable remainder trusts. For a deeper understanding, you can learn more about tax-loss harvesting strategies and their implementation.

5. Establish Clear Debt Guidelines and Leverage Limits

While debt is often viewed negatively, strategic leverage can be a powerful wealth-building tool. The key is to control it, not let it control you. Establishing a formal family policy on debt defines acceptable uses for leverage, such as for a mortgage or business financing, and sets clear maximums. This disciplined approach prevents over-leveraging, protects family assets from excessive risk, and ensures financial stability across different economic cycles, making it one of the most critical rock solid financial rules to live by for families.

Elevating the Framework with Risk Management

For high-net-worth families, particularly those with business interests or significant real estate holdings, a debt policy acts as a crucial risk management framework. Instead of making ad-hoc borrowing decisions, the family operates under pre-agreed-upon rules that protect the core of their wealth. These guidelines, often inspired by the conservative leverage principles of investors like Warren Buffett, create a vital buffer against market volatility and poor decision-making under pressure.

For instance, a family might create a policy stipulating that total household debt cannot exceed 30% of their total net worth. A family with real estate investments might enforce a maximum 65% loan-to-value (LTV) ratio on all new property acquisitions. For a family with a substantial investment portfolio, a rule might limit margin borrowing to no more than 15% of the portfolio's value, preventing catastrophic losses during a market downturn.

Actionable Implementation Steps

To effectively implement this strategic framework, consider these practical steps:

- Create a Formal Debt Policy Document: Work with your financial advisor to draft a clear, written policy. This document should outline approved uses for debt, maximum debt-to-net-worth or debt-to-income ratios, and specific limits for different asset classes (e.g., real estate vs. securities).

- Conduct an Annual Debt Review: Schedule an annual meeting to review all outstanding family and business debts against the established policy. This is the time to assess interest rate risk, evaluate repayment strategies, and adjust the policy if family circumstances have materially changed.

- Educate All Decision-Makers: Ensure all adult family members who have financial authority understand and agree to the debt guidelines. This creates accountability and prevents a single member from taking on risk that could jeopardize the entire family's financial security.

- Model Leverage Scenarios: Engage your financial advisor to run stress tests and model the potential impact of increased leverage or rising interest rates on your family's overall portfolio and cash flow. This data-driven approach helps validate and refine your debt limits.

6. Implement Diversification Across Multiple Asset Classes and Risk Levels

A foundational principle of sophisticated portfolio management, diversification is the art of spreading capital across various uncorrelated asset classes. Based on the principles of Modern Portfolio Theory, pioneered by Harry Markowitz, this strategy is designed to protect wealth from single-sector downturns and reduce overall volatility without sacrificing growth potential. For high-net-worth families, this isn't just a suggestion; it is one of the most essential rock solid financial rules to live by for families to ensure wealth preservation across generations.

A Structured Approach to Portfolio Construction

The core idea is to combine investments like equities, fixed income, real estate, and alternatives (private equity, hedge funds) that react differently to economic events. When one asset class underperforms, another may perform well, smoothing out returns and shielding the portfolio from catastrophic losses. This structured approach is vital for weathering multiple economic cycles.

Consider a family with a $5 million investment portfolio. Instead of concentrating heavily in public equities, they might construct a diversified portfolio: $2 million in global stocks (40%), $1.25 million in bonds and fixed income (25%), $1 million in income-producing real estate (20%), and $750,000 in alternative investments (15%). This allocation provides a robust defense against market volatility while still capturing upside potential from various economic engines.

Actionable Implementation Steps

To build and maintain a properly diversified portfolio, families should follow a disciplined process:

- Establish Target Allocations: Work with a financial advisor to define your family's unique risk tolerance, time horizon, and financial goals. Use this profile to set specific target percentages for each asset class in your portfolio.

- Rebalance Strategically: Review your portfolio at least annually or when allocations drift more than 5% from their targets due to market movements. Rebalancing involves selling overperforming assets and buying underperforming ones to return to your desired mix.

- Utilize a Core-Satellite Strategy: Build the "core" of your portfolio with low-cost, broad-market index funds or ETFs. Use actively managed funds or direct investments as "satellites" to seek alpha in niche areas like private credit or venture capital.

- Ensure Adequate Liquidity: Maintain sufficient cash or cash equivalents to meet short-term goals and unexpected expenses without being forced to sell long-term investments at an inopportune time. This prevents market downturns from derailing your financial plan.

7. Establish Separate Accounts for Different Financial Goals and Time Horizons

Segregating capital into distinct accounts based on purpose is a powerful organizational strategy that brings clarity and discipline to family wealth management. This approach, rooted in goal-based portfolio management, involves creating separate buckets for each major financial objective, such as education, retirement, philanthropy, and business capital. This structural and psychological separation prevents goal-mixing, enables appropriate risk positioning for each timeline, and is one of the most effective rock solid financial rules to live by for families.

Tailoring Investments to Timelines and Goals

By creating dedicated accounts, families can align their investment strategies specifically to the time horizon and risk tolerance of each goal. A short-term goal like a home down payment in three years requires a conservative allocation, while a long-term legacy fund can be invested more aggressively for maximum growth.

For instance, a retired couple might structure their wealth into three buckets: a low-risk account with 1-3 years of living expenses in cash and short-term bonds, an intermediate account for needs 3-10 years out with a balanced portfolio, and a long-term legacy portfolio invested primarily in global equities. This prevents the need to sell growth assets during a market downturn to cover immediate expenses, providing both stability and growth potential.

Actionable Implementation Steps

To effectively implement a multi-account strategy, consider these practical steps:

- Create Purpose-Driven Naming Conventions: Label each account with its specific goal (e.g., "Grandchildren's 529 Fund," "2028 Real Estate Acquisition," "Family Charitable Trust"). This reinforces the purpose of the capital and discourages co-mingling.

- Automate Capital Flows: Work with your financial institution to set up automatic, recurring transfers from your primary income sources into each designated goal account. This "pay yourself first" method ensures consistent progress.

- Conduct Goal-Specific Reviews: During your quarterly financial reviews, assess the performance of each account against its specific benchmark and goal timeline. This allows for targeted adjustments without disrupting your entire financial plan.

- Leverage Different Account Types: Use the most tax-advantaged accounts for each goal. This means utilizing 529 plans for education, HSAs for healthcare, and various trust structures for philanthropic and legacy objectives, optimizing the efficiency of each bucket.

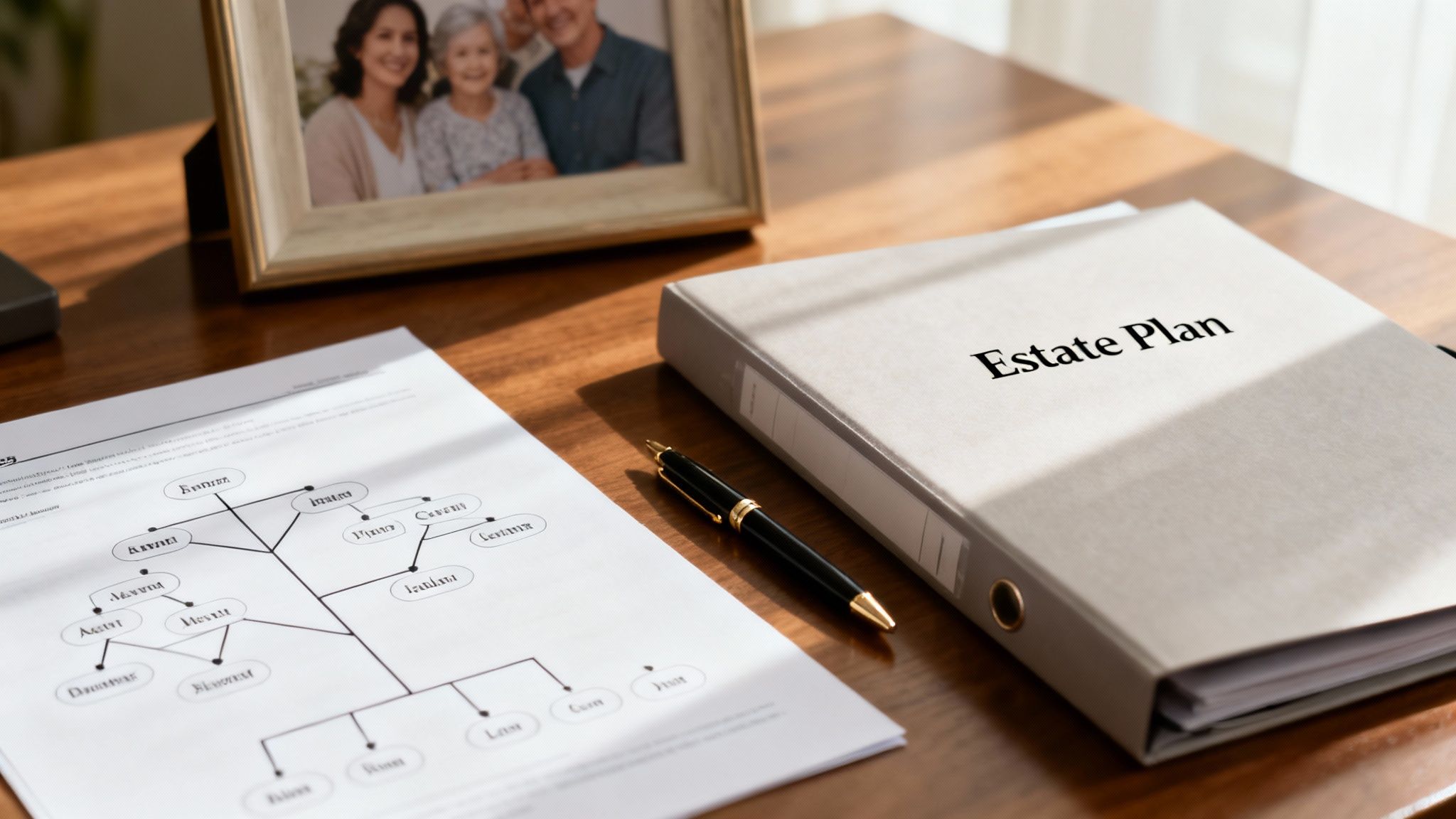

8. Create a Succession and Estate Planning Framework Updated Every 3-5 Years

An estate plan is more than a legal document; it's a dynamic framework for the responsible stewardship of generational wealth. For families of means, this involves a comprehensive, regularly updated system that outlines wealth transfer plans, business succession strategies, and contingency plans for incapacity. A static plan created decades ago is insufficient; a proactive, living plan is one of the most essential rock solid financial rules to live by for families.

Elevating the Framework with Proactive Reviews

The core principle is that your estate and succession plan must evolve alongside your family, business, and the legal and tax landscape. A family with a multi-million dollar estate might initially use an irrevocable life insurance trust (ILIT) to provide liquidity and reduce tax liability. As their business grows, they might add a detailed buy-sell agreement and a dynasty trust to protect assets for multiple generations. Regular reviews ensure these sophisticated tools remain aligned with their ultimate goals and current laws. To secure your family's future and ensure a smooth transfer of assets, understanding the roles of both trusts and wills is essential. You can learn more about Trusts and Wills in Texas to aid your estate plan.

Actionable Implementation Steps

To build and maintain a robust estate planning framework, follow these strategic steps:

- Assemble a Coordinated Team: Your plan's success depends on collaboration. Engage an experienced estate planning attorney, a tax advisor, a financial planner, and an insurance professional to work in concert, ensuring all aspects of your financial life are aligned.

- Schedule Regular Reviews: Calendar a formal review of your entire estate plan every three to five years, or after any major life event like a birth, death, divorce, or significant change in assets. This keeps documents current and effective.

- Communicate with Heirs: Include successor trustees and key beneficiaries in high-level planning conversations. Documenting your values and wishes alongside the legal structure helps prevent future conflict and ensures your intentions are understood and honored.

- Organize and Document: Create a central, secure file-either physical or digital-that contains all important documents, account information, and contact details for your professional advisors. Share its location with your appointed executor and trustee.

9. Establish Investment Policy Statements with Clear Rebalancing Disciplines

An Investment Policy Statement (IPS) is a formal governance document that codifies a family's investment strategy, moving it from abstract discussion to a concrete, actionable plan. Popularized by institutional best practices from organizations like the CFA Institute, the IPS outlines investment philosophy, objectives, risk tolerance, and specific asset allocation targets. This document is one of the most powerful rock solid financial rules to live by for families, as it removes emotion and behavioral biases from critical investment decisions.

Elevating the Framework with Rebalancing Discipline

The true power of an IPS lies in its pre-defined rebalancing protocols. These rules dictate precisely when and how a portfolio will be brought back to its target allocation, ensuring discipline during periods of market volatility. This prevents reactive, fear-driven selling during downturns or irrational exuberance during market peaks.

For example, a family office with a $100M portfolio might have an IPS targeting a 60% equity and 40% fixed income allocation. The policy could state a rebalancing trigger is activated whenever any primary asset class drifts more than 5% from its target. If a strong equity market pushes the allocation to 66% equities, the IPS mandates selling 6% of the equity position and reinvesting the proceeds into fixed income to restore the original 60/40 balance, systematically locking in gains.

Actionable Implementation Steps

To effectively implement this governance tool, consider these practical steps:

- Define Clear Rebalancing Triggers: Work with your advisor to establish specific, non-negotiable triggers. This can be time-based (quarterly, annually) or tolerance-band based (when an asset class deviates by a set percentage like +/- 5%), or a combination of both.

- Use the IPS as a Reference, Not a Draft: During market stress, the IPS is your anchor. It is the document you refer to for guidance, not the one you hastily revise based on short-term news. Its purpose is to enforce long-term strategy over short-term panic.

- Integrate Tax Efficiency: Your rebalancing strategy should be tax-aware. Collaborate with your CPA and wealth advisor to prioritize rebalancing within tax-advantaged accounts or by harvesting losses to offset gains where possible.

- Ensure Stakeholder Buy-In: The IPS should be a consensus document. All key family stakeholders and trustees should understand, agree to, and formally acknowledge the policy. It should be reviewed annually to ensure it still aligns with the family's long-term objectives.

10. Practice Regular Financial Education and Family Financial Communication

Beyond spreadsheets and investment accounts, the true preservation of multi-generational wealth lies in shared knowledge and open dialogue. Instituting a formal program of financial education and communication ensures family members are not just inheritors, but competent stewards. This approach, advocated by wealth preservation experts like Roy Williams and Vic Preisser, transforms wealth from a taboo topic into a tool for shared family values and goals. It is one of the most critical rock solid financial rules to live by for families aiming for long-term prosperity.

Elevating the Framework with Structured Governance

For high-net-worth families, this goes beyond simple dinner table conversations. It involves creating a structured governance model for communication. The objective is to build financial literacy, clarify the family's mission, and prepare the next generation for the responsibilities they will inherit. This proactive education prevents the disputes and mismanagement that erode wealth over time.

For instance, a business-owning family might hold quarterly meetings where a financial advisor explains portfolio performance in the context of global markets. They could also involve younger, interested family members in non-critical strategic discussions, providing them with real-world experience. Another example is an annual "wealth summit" for all adult stakeholders to review the family's balance sheet, philanthropic goals, and estate plan, ensuring alignment and transparency.

Actionable Implementation Steps

To effectively implement this rule, consider these practical steps:

- Establish a Meeting Cadence: Schedule regular family financial meetings (quarterly or semi-annually). Create and distribute an agenda beforehand with relevant documents like investment summaries to ensure productive discussions.

- Start Education Early: Financial literacy is a lifelong journey. You can learn more about how to teach kids about money with age-appropriate lessons on budgeting, saving, and investing to build a strong foundation.

- Focus on Values, Not Just Valuations: Use meetings to discuss the "why" behind the wealth. Talk about family values, philanthropic missions, and the purpose of the capital beyond the numbers on a page.

- Engage Neutral Third Parties: For sensitive topics or complex family dynamics, consider engaging a family business advisor or wealth psychologist. They can facilitate difficult conversations and help maintain objectivity and harmony.

10 Family Financial Rules Comparison

Integrating These Rules into Your Family's Financial DNA

The journey toward lasting financial prosperity is not a sprint; it is a marathon built on a foundation of discipline, strategic planning, and shared family values. The ten principles outlined in this guide represent more than just a checklist. They are the essential building blocks for a resilient financial architecture, designed to withstand market volatility, adapt to life’s transitions, and empower future generations. Adopting these rock solid financial rules to live by for families is the first, most critical step in transforming your financial future from a series of reactions into a deliberate, values-driven legacy.

Each rule, from the foundational 50/30/20 budget framework to the forward-looking discipline of a triennial estate plan review, contributes a unique layer of strength to your overall financial structure. Think of them not as isolated tactics but as interconnected components of a comprehensive system. Your Family Financial Constitution, for example, provides the "why" that fuels the "how" of your Investment Policy Statement and strategic charitable giving programs. Similarly, maintaining a robust emergency fund provides the stability needed to confidently pursue long-term growth through diversified investments without being forced to liquidate assets at an inopportune time.

From Knowledge to Action: Weaving the Rules into Your Life

True mastery comes not from simply understanding these rules, but from integrating them into the very fabric of your family's daily operations and long-term vision. This process requires a commitment to continuous action and open dialogue. It means moving beyond theoretical knowledge to practical, consistent application.

Here are the key takeaways to focus on as you begin this integration:

- Communication is the Cornerstone: The most sophisticated financial plan will falter without open and regular communication. The practice of family financial meetings is not just about reviewing numbers; it's about reinforcing shared values, aligning on goals, and educating the next generation. This transforms wealth from a mere asset into a tool for achieving a shared family mission.

- Discipline Over Emotion: Market fluctuations, economic uncertainty, and personal biases are constant threats to a sound financial strategy. Rules like establishing clear debt limits, creating an Investment Policy Statement, and adhering to a rebalancing schedule are designed to instill discipline. They provide a logical framework that guides decisions during periods of emotional stress, preventing costly, reactive mistakes.

- Proactive Planning Prevents Future Crises: Estate planning, succession strategies, and tax-loss harvesting are not reactive measures. They are proactive strategies that anticipate future challenges and opportunities. By addressing these complex issues regularly, you protect your assets, minimize tax burdens, and ensure a smooth transfer of wealth, leadership, and values. This foresight is what separates families who merely accumulate wealth from those who build enduring legacies.

The ultimate value of implementing these principles extends far beyond the numbers on a balance sheet. It cultivates financial literacy, fosters a sense of shared stewardship, and provides a clear roadmap for navigating complex financial decisions with confidence. By committing to these rock solid financial rules to live by for families, you are not just managing money; you are architecting a legacy of security, opportunity, and purpose that will benefit your loved ones for decades to come.

Navigating the complexities of high-net-worth family finances requires more than just rules; it demands expert guidance and a customized strategy. At Commons Capital, we specialize in helping families implement these sophisticated frameworks, turning financial principles into a powerful, integrated plan for long-term prosperity. Schedule a consultation with our team to begin building your family's enduring financial legacy today.