Private wealth management is more than an upgraded version of standard financial advice; it's a comprehensive, high-touch service designed specifically for high-net-worth individuals (HNWIs) and families. This isn't just about investment tips. It's an integrated strategy that coordinates every aspect of your financial life to grow, protect, and ultimately transfer your wealth according to your wishes.

Your Financial Quarterback: Understanding Private Wealth Management

Think of a private wealth manager as the quarterback for your entire financial life. A QB doesn't just throw the ball — they read the defense, call the plays, and coordinate a team of specialized players. That’s precisely what a wealth manager does. They direct a team of experts — investment analysts, tax advisors, estate planning attorneys — to execute a single, unified game plan built around your unique goals.

This approach is fundamentally different from standard financial advice, which often operates in the silo of investments. Private wealth management tackles the bigger picture. Significant wealth introduces a level of complexity that isolated, one-off solutions simply cannot manage. For a successful business owner, a top-tier professional, or a family navigating multi-generational finances, an off-the-shelf strategy is insufficient.

A Holistic Approach to Your Financial Well-Being

At its core, what is private wealth management is a service built on a deep, personal relationship. It’s about moving beyond the numbers on a spreadsheet to genuinely understand your family dynamics, your hopes for a legacy, and the values you want to uphold. Only then can a truly personalized financial road map be created.

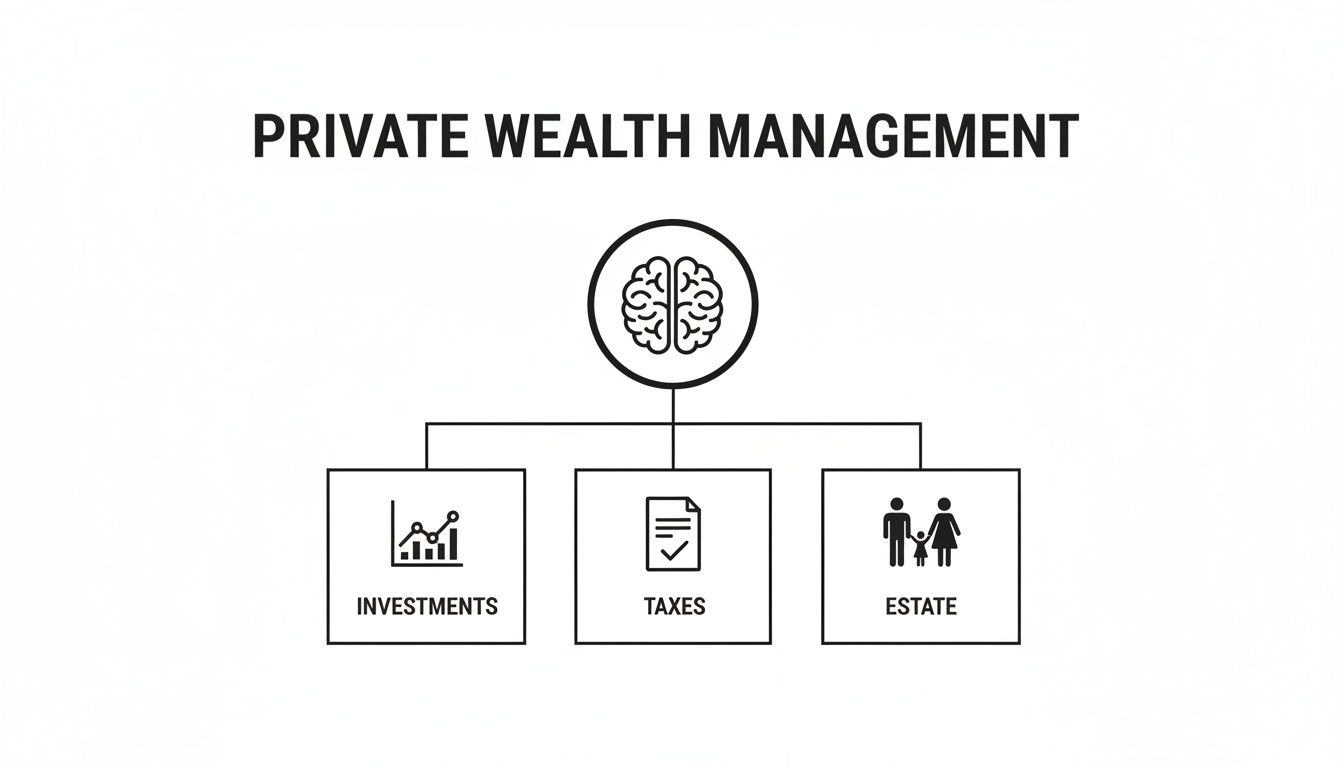

The core services of wealth management are an interconnected system, not just a checklist. Your overarching strategy is the brain, directing the specialized functions of investments, tax planning, and estate management to work in concert.

This integrated structure ensures that investment decisions are never made in a vacuum. They are constantly evaluated against tax implications and must align with your long-term estate and legacy objectives.

Why Integration Is the Secret Sauce

The real value emerges when all these elements work together seamlessly. For example, a high-return investment might look great on paper, but it's a failure if it creates a massive, unexpected tax liability. A skilled wealth manager anticipates these conflicts and optimizes your entire portfolio for tax efficiency.

Similarly, an estate plan isn’t just a stack of legal documents. It's a living strategy that ensures your business succession plan works in harmony with your family’s long-term financial security.

This blend of sharp analytical rigor and genuine human connection is the hallmark of effective private wealth management. It's about navigating choppy markets, guiding families through high-stakes decisions, and being a steady, trusted voice when things get uncertain.

Ultimately, the goal is to simplify complexity for you. With one central point of contact overseeing your entire financial world, you can make decisions with confidence, avoid costly mistakes, and focus on what truly matters. This partnership ensures every financial move is a coordinated step toward realizing your long-term vision.

Private Wealth Management vs. Standard Financial Advice

It's easy to confuse these two, but they serve very different needs. Here's a quick breakdown of how they compare.

While both provide value, private wealth management is built for a level of financial complexity that standard advice is not equipped to handle.

The Core Services of a Private Wealth Management Firm

True private wealth management is the central command for your entire financial world, a suite of interconnected services built to handle the complexities that come with significant assets.

Each service isn't a standalone product but a critical gear in a much larger machine, ensuring a decision in one area positively impacts your goals in another.

This unified approach prevents costly mistakes by making sure all the pieces are working together. Let's break down the essential services that form the bedrock of this high-level partnership.

Bespoke Investment Management

Investment strategies for HNWIs are custom-built, never off-the-shelf. A manager first gains a deep understanding of your risk tolerance, time horizon, and specific goals — whether you're funding a new company, mapping out retirement, or building a family legacy.

This isn't about chasing market trends. It's about constructing a sophisticated, diversified portfolio designed for long-term, sustainable growth.

The needs can vary dramatically. An athlete with a high but potentially short-lived income requires a different approach than a business owner planning to sell in ten years. The athlete’s portfolio might focus on capital preservation and steady income, while the owner’s could be structured to maximize growth before a major liquidity event.

A key difference is access. Private wealth clients often get exposure to exclusive opportunities not available to the public, including:

- Private Equity: Investing directly in private companies before they go public.

- Venture Capital: Backing promising startups with explosive growth potential.

- Private Credit: Lending money directly to businesses, often for higher yields than traditional bonds.

- Hedge Funds: Using advanced strategies to generate returns in various market conditions.

These alternative investments can provide powerful diversification away from public markets and offer significant return potential, but their complexity demands expert navigation.

Strategic Tax and Estate Planning

Effective wealth management is as much about what you keep as what you earn. A major part of the job is structuring a client's financial life to be as tax-efficient as possible, both today and for future generations.

This involves coordinating with tax professionals to execute strategies like tax-loss harvesting, strategic charitable giving, and structuring investments to minimize tax impact. For a family with significant assets, this planning is critical. While wealth managers coordinate this, the landscape often involves specialized experts like an independent financial advisor who can offer focused guidance.

Estate planning in this context goes far beyond just drafting a will. It's a comprehensive strategy for the seamless transfer of wealth, ensuring a client's wishes are honored while minimizing estate taxes and preventing family conflicts.

This process often involves setting up trusts, creating family limited partnerships, or developing a clear succession plan for a family business. The wealth manager acts as the quarterback, making sure all legal documents align perfectly with the overarching financial plan.

Philanthropic and Legacy Planning

For many successful individuals, making a lasting impact is as important as growing their wealth. Private wealth managers help clients transform their philanthropic vision into a structured, effective strategy.

This can involve several sophisticated approaches:

- Donor-Advised Funds (DAFs): A charitable giving account where you contribute, receive an immediate tax deduction, and then recommend grants to your favorite charities over time.

- Private Foundations: Establishing a formal charitable entity that can be managed by the family for generations, creating a powerful and lasting legacy.

- Charitable Trusts: Legal structures that allow for significant donations while also providing financial benefits to you or your heirs.

By weaving philanthropy into the overall financial plan, advisors help clients support the causes they're passionate about in the most impactful and tax-efficient way.

Comprehensive Risk Management

Protecting your assets from the unexpected is a cornerstone of wealth preservation. A private wealth manager starts by conducting a thorough risk analysis, identifying potential threats to your financial stability.

This extends beyond standard life and disability insurance to cover a broad spectrum of protections, including personal liability (umbrella) policies to guard against lawsuits and specialized insurance for unique assets like fine art, classic cars, or extensive real estate holdings.

For business owners, risk management also means implementing tools like key person insurance and buy-sell agreements. These ensure the business can survive the loss of a critical partner or owner.

The demand for these specialized services is clear. In the U.S., ultra-high-net-worth individuals — those with over $5 million — make up just 0.3% of the population but control a staggering 24.7% of all financial assets. Research shows these clients actively seek services like business planning (75%), foundation management (74%), and private banking (61%) to manage their complex financial lives. For more on this, you might be interested in our broader look at wealth management strategies.

Is Private Wealth Management Right for You?

When is the right time to hire a private wealth management firm? It’s less about hitting a specific number and more about reaching a certain level of complexity.

While many firms have a minimum for investable assets — often starting around $500,000 — the real trigger is when your financial life becomes too tangled for standard advice. It’s the tipping point where your wealth creates challenges that require a coordinated team of specialists to solve.

The answer becomes clear when you see your own story reflected in the types of clients who benefit most from this level of service. For them, a financial quarterback isn't a luxury; it’s a necessity.

The Successful Business Owner

For entrepreneurs, wealth is rarely a simple number in a bank account. It's often tied up in a single, illiquid asset: their business. This creates unique challenges that a generic financial plan cannot address, especially when navigating a major liquidity event like a company sale.

A private wealth manager plans for that moment years in advance, structuring personal and business assets to optimize the outcome and minimize the tax impact. This involves pre-sale planning, managing concentrated stock positions, and then building a diversified portfolio that secures your financial future long after the transition.

The High-Earning Professional

Top-tier surgeons, lawyers, consultants, or professional athletes face a different financial puzzle. Their income can be massive but also inconsistent or concentrated into a relatively short career. The primary goal is converting today's high earnings into lasting wealth.

A wealth manager for these professionals tackles specific challenges:

- Irregular Income Streams: Planning around large bonuses, performance payouts, or earnings that fluctuate significantly.

- Advanced Tax Strategies: Using sophisticated strategies to legally defer and reduce a high tax burden.

- Asset Protection: Shielding personal assets from professional risks through specialized legal and insurance structures.

The goal is to build a rock-solid financial foundation that provides stability and income long after peak earning years have passed.

The question to ask isn't just, "Do I have enough money?" It's, "Is my financial situation complex enough that a team of specialists would unlock more value than I could on my own?" When the answer is yes, it's time to find a true partner.

The Multi-Generational Family

For families where significant wealth has been inherited, the focus shifts from creation to preservation and purpose. The challenges are often less about numbers and more about people: stewardship, family governance, and ensuring wealth is a positive force for generations to come.

Here, a private wealth manager acts as an impartial guide. They help establish a clear framework for decision-making, such as a family constitution, and educate the younger generation on financial responsibility. They facilitate difficult conversations and ensure the family’s core values are woven into every financial choice.

The Prudent Retiree

Once you stop earning and start drawing down your assets, the rules change entirely. The primary goal for retirees is generating a reliable, tax-efficient income stream that will last a lifetime. This requires a shift from an accumulation mindset to a preservation and distribution strategy.

A wealth manager designs sophisticated income plans that balance growth with principal protection. They map out which accounts to draw from and when — taxable, tax-deferred, and tax-free — to minimize the tax bite and make the money last. This planning also extends to preparing for potential long-term care costs and crafting an estate plan for a seamless transfer of remaining assets.

Exploring Alternative and Private Market Investments

The investment world for the wealthy once centered on public stocks and bonds. That's changing. A massive shift is underway as affluent individuals and families seek better returns and more stability through alternative and private market investments.

This isn't a minor strategic tweak; it's a fundamental evolution. Savvy investors are now allocating capital to opportunities once reserved for large institutions. However, entering these complex markets requires a high level of expertise.

The Appeal of Going Private

What's driving this trend? It boils down to a few key motivators. Investors are chasing opportunities that public markets no longer offer as reliably.

- Higher Return Potential: Private equity and venture capital offer the chance to invest in groundbreaking companies during their explosive early growth years, long before an IPO.

- Greater Diversification: Alternative assets often have a low correlation to the stock market, providing a layer of stability to a portfolio during downturns.

- Income Generation: Assets like private credit and certain real estate investments can generate a steady, attractive income stream, often higher than traditional bonds.

The data below illustrates the growing enthusiasm among financial professionals for increasing their clients' allocations to private markets.

This trend reflects a clear and growing confidence in the long-term value these private assets can deliver.

Why Expert Guidance Is Non-Negotiable

While the potential upside is significant, these investments come with unique risks. This is where a skilled wealth manager proves their worth, providing the necessary due diligence and access.

Complexities they help navigate include:

- Illiquidity: Capital is often tied up for years, which demands careful, forward-thinking financial planning.

- Valuation Complexity: Determining the value of a private company is far more difficult than checking a stock ticker and requires deep, specialized analysis.

- Access and Due Diligence: The best deals are not publicly advertised. Wealth managers use their exclusive networks to find and rigorously vet these opportunities.

A wealth manager's real job is to unlock the incredible potential of private markets while methodically managing the risks. They make sure every single investment fits perfectly into the client's bigger picture and long-term goals.

Alternative investments are no longer a niche play. A recent survey found that 92% of financial advisors are already using them, and 91% plan to increase client allocations. The top choices are private debt (89%), private equity (86%), and real estate (85%).

Beyond these, wealth managers can assist with the intricacies of managing alternative investments like cryptocurrency wallets and digital assets. To invest successfully, you need a sophisticated partner who knows the landscape inside and out. To learn more, check out our guide on alternative investments.

How to Choose the Right Private Wealth Management Partner

Selecting a private wealth management partner is one of the most significant financial decisions you will ever make. This goes beyond hiring someone to manage your investments; you are building a long-term relationship with a trusted advisor who will guide your entire financial life.

Getting it right requires a clear, methodical approach. Think of it as hiring a C-suite executive for your personal enterprise. You need to do your homework, ask tough questions, and look beyond the sales pitch to find a firm that truly aligns with your goals, values, and financial complexity.

Start with Fiduciary Duty

Before you look at a performance chart, your first question should be simple: "Are you a fiduciary?" This is a non-negotiable starting point.

A fiduciary is legally and ethically required to act in your best interest, period. Advisors who operate under this standard, like Registered Investment Advisors (RIAs), must put your financial well-being ahead of everything else. This is different from the "suitability standard," where a broker might recommend a product that is merely "suitable" but also pays them a higher commission. Confirming a firm’s fiduciary commitment is your first line of defense.

Understand the Fee Structure

How a firm is compensated directly reflects its incentives. You need total transparency and should be skeptical of any advisor who is evasive about explaining their fee structure.

Most reputable firms use one of two models:

- Assets Under Management (AUM): The firm charges a percentage of the assets they manage for you. This aligns their success with yours — when your portfolio grows, so does their revenue.

- Flat Fees: Some firms, especially those working with very large portfolios, charge a fixed annual fee for predictability.

Avoid firms that rely heavily on commissions from selling specific financial products. This structure creates a conflict of interest, tempting the advisor to push whatever pays them the most, not what is genuinely best for you.

Assess Investment Philosophy and Expertise

A firm’s core beliefs about growing and protecting wealth must align with yours. Do they champion passive index investing or active management? There is no single right answer, but their approach must match your comfort level with risk and your long-term goals.

Equally important is their experience with clients like you. A wealth manager specializing in helping tech founders navigate stock options will be more effective than one who primarily works with retirees. Ask for examples of how they’ve helped people in similar situations.

This is also where you assess their advanced strategy toolkit. For instance, private market investing is no longer a niche play. A Private Wealth Survey from Hamilton Lane found that nearly 60% of financial professionals plan to allocate 10% or more of client portfolios to private markets. You need to know if a potential partner has the access and expertise to guide you there.

Choosing a partner is about finding a philosophical match. If their core beliefs about how to build and protect wealth don't align with yours, the relationship is unlikely to succeed long-term, no matter how impressive their credentials are.

Red Flags to Avoid

As you meet with potential firms, remain vigilant for warning signs. Spotting these early can save you from significant financial stress.

Be on the lookout for these critical red flags:

- Lack of Transparency: If an advisor is vague about fees, their strategy, or potential conflicts of interest, walk away.

- High-Pressure Sales Tactics: A true partner provides information and guidance, not pressure to make a rushed decision.

- A "One-Size-Fits-All" Approach: If their plan for you feels generic and not tailored to your specific life and goals, it shows they haven't been listening.

- Overpromising Returns: No one can guarantee market performance. Be deeply skeptical of anyone who promises consistently high returns.

Ultimately, this choice comes down to trust, chemistry, and alignment. Prepare yourself by knowing what to look for and what to ask. For a more detailed checklist, review our guide on the key questions to ask a potential wealth manager.

Your Client Journey with a Wealth Management Firm

Partnering with a private wealth management firm is not like buying a product off the shelf. It is the beginning of a long-term, collaborative process designed to build a complete picture of your financial world, founded on mutual trust and understanding.

The journey unfolds in clear, deliberate phases, moving from broad discovery to detailed implementation and continuous oversight.

The Initial Discovery and Goal Setting

The process begins with a series of in-depth discovery meetings. This is more than a review of your assets and liabilities. A true wealth advisor will spend significant time understanding your values, family dynamics, personal ambitions, and even your anxieties about the future. The goal is to understand who you are and what you want your wealth to accomplish for you and for future generations.

You’ll discuss everything from your true comfort level with risk to your philanthropic passions. This foundational stage is critical because every subsequent decision will be measured against the personal financial roadmap you build together.

A wealth management relationship is a two-way street. The discovery process is as much about you interviewing the firm as it is about them getting to know you. You're looking for the right fit in philosophy, communication style, and long-term vision.

Developing Your Customized Financial Plan

Once your advisor has a crystal-clear picture of your objectives, they move into strategy mode. They bring in specialists — tax professionals, estate attorneys, and investment analysts — to construct a comprehensive, integrated financial plan. This is a detailed blueprint crafted specifically for you.

This plan will map out specific, actionable recommendations for every piece of your financial life:

- Investment Strategy: A proposed asset allocation designed to meet your growth and income targets.

- Tax Optimization: Strategies to minimize your tax liability now and in the future.

- Estate and Legacy Plan: A clear structure for transferring your wealth efficiently and effectively.

- Risk Management: A thorough review of your insurance coverage and asset protection measures.

Implementation and Ongoing Partnership

After you approve the plan, the firm begins to execute the strategies. This is the hands-on phase — opening accounts, reallocating investments, and coordinating with your legal and tax teams to implement your estate plan.

But the journey doesn't end there. What is private wealth management if not an ongoing relationship? Your life and the markets will change. Your advisor will schedule regular reviews, typically quarterly or semi-annually, to track progress, discuss life updates, and make necessary adjustments. This ensures your strategy remains a living document, always aligned with your current reality and future goals.

Common Questions About Private Wealth Management

It's natural to have questions when dealing with significant wealth. Here are answers to some of the most common inquiries we receive from those considering a private wealth management firm.

What's the Typical Minimum to Get Started?

This varies by firm, but a common starting point is around $500,000 to $1 million in investable assets. The threshold is less about a magic number and more about reaching a level of financial complexity that requires the integrated, hands-on strategy that private wealth management provides.

Is a Private Wealth Manager a Fiduciary?

This is one of the most important questions you can ask. The short answer is: they should be, but not all are. A fiduciary has a legal and ethical obligation to act in your best interest, period. Registered Investment Advisors (RIAs) are held to this higher standard. Always confirm a firm's fiduciary status to ensure their advice is focused on your success, not on earning a commission.

The fiduciary standard is the bedrock of a healthy client-advisor relationship. It means our success is directly tied to yours. Every single recommendation has to pass a simple test: is this truly what's best for our client?

How Is This Different from a Robo-Advisor?

The difference is night and day, centered on personalization and financial scope.

- Robo-Advisors are excellent, low-cost tools that use algorithms to manage investment portfolios. They are ideal for individuals with straightforward needs or those just beginning to build wealth.

- Private Wealth Management is a high-touch, human-led partnership. We analyze your entire financial picture — complex tax situations, intergenerational wealth transfer, charitable giving, and access to private investment opportunities not available to the public.

Think of it this way: a robo-advisor is like a self-driving car on a clearly marked highway. A private wealth manager is your personal financial quarterback, coordinating a team of specialists to navigate a complex, ever-changing game. It's a scope that automated platforms are not designed to handle.

At Commons Capital, we know that managing significant wealth isn't just about numbers — it's about people, families, and futures. Our team is here to provide the sophisticated guidance and comprehensive strategies you need to move forward with complete confidence.

Explore how our wealth management services can help you achieve your goals.