Buying a growth and income fund because it sounds balanced is lazy portfolio construction.

High-net-worth investors need a sharper standard. A pooled fund may offer convenience, but convenience is a weak reason to give up control of security selection, tax timing, and portfolio cash flow. In large taxable accounts, those trade-offs matter more than the label on the fund.

The objective is sensible. You want capital appreciation, but you do not want to chase pure growth and absorb unnecessary volatility. You also want dependable cash flow, but not at the cost of owning a slow portfolio built only for yield. That combination is reasonable. The bigger question is how to build it efficiently.

For affluent families, the starting point should be your balance sheet, tax profile, liquidity needs, and estate plan. It should not be a product designed for thousands of other shareholders.

That is the main weakness of the typical growth and income fund. It bundles good intentions into a structure that can be inefficient for the investor who already has enough capital to own the underlying stocks and bonds directly. You may end up holding far more positions than you need, receiving distributions on the fund’s schedule instead of your own, and paying an extra layer of fees for decisions that are only loosely connected to your goals.

Large, established funds can be professionally run and still be the wrong tool. Size does not solve the core problem. Structure does.

For many HNW investors, the better question is not which growth and income fund to buy. It is whether a fund should be the vehicle at all. In many cases, a self-constructed portfolio of individual equities and bonds is cleaner, more transparent, more tax-aware, and less expensive over time. That approach takes work, but a firm like Commons Capital can do that work for you and build around your actual constraints instead of forcing your wealth into a standardized wrapper.

Rethinking the Role of Growth and Income Funds in Your Portfolio

Growth and income funds exist because the need they address is real. Investors want two things at once. They want their assets to grow, and they want those assets to produce usable cash flow.

That combination matters even more when your financial life is complex. Business owners, retired executives, athletes, entertainers, and multigenerational families don’t just need return. They need flexibility, visibility, and control over how return shows up.

Why the default advice breaks down

The usual sales pitch for growth and income funds is convenience. One fund owns a mix of growth-oriented equities, dividend-paying stocks, and bonds. That sounds efficient.

For smaller accounts, it often is.

For larger taxable portfolios, convenience can become expensive. You may end up owning hundreds or thousands of positions you’d never select yourself. You may receive distributions on a schedule that doesn’t match your cash needs. You may also inherit portfolio decisions made for a broad shareholder base instead of your specific tax situation, liquidity needs, and estate plan.

A balanced fund is simple for the fund company. It isn’t always simple for the investor who has to live with the consequences.

The real decision for affluent investors

A high-net-worth portfolio shouldn’t start with a product. It should start with a set of constraints and priorities:

- Income needs: Are you spending portfolio cash flow now, or reinvesting it?

- Tax sensitivity: Are assets held in taxable accounts, retirement accounts, trusts, or a mix?

- Control requirements: Do you want to know exactly what you own and why?

- Risk tolerance: Are you trying to reduce drawdowns, smooth income, or preserve optionality for future opportunities?

Growth and income funds can address parts of that list. They rarely address all of it well.

My view

If you need a quick, broadly diversified allocation, a growth and income fund is defensible. If you have substantial assets and a real need for tax management, cash-flow design, and position-level transparency, it’s usually not the best answer.

That’s why experienced investors should treat these funds as one tool, not the default blueprint.

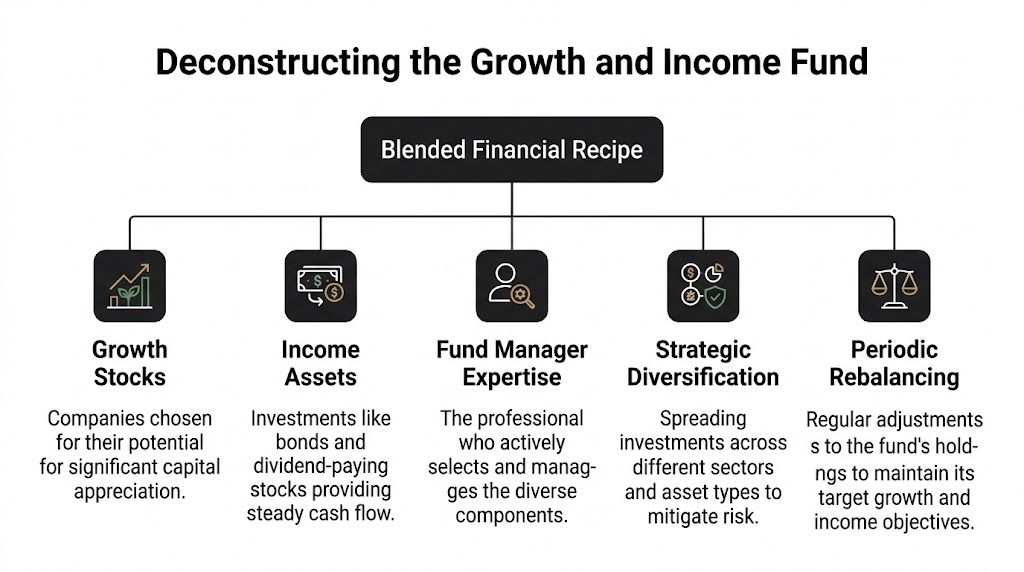

Deconstructing the Growth and Income Fund Structure

A growth and income fund is a blended financial recipe. The manager combines assets meant to appreciate with assets meant to distribute cash.

The idea is simple. One sleeve pushes long-term growth. The other sleeve dampens volatility and generates income.

The recipe behind the label

At the structural level, growth and income funds typically allocate 50-70% to growth-oriented equities and 30-50% to income-generating assets like dividend-paying blue-chip stocks and bonds, which is designed to reduce overall portfolio volatility compared with pure growth funds, according to Bajaj Finserv’s overview of growth and income funds.

That’s why you’ll often see versions of a stock-and-bond blend inside these strategies. The exact mix varies. The architecture usually doesn’t.

What the manager is actually doing

A fund manager is trying to solve five jobs at once:

- Select growth stocks: Companies expected to compound value over time.

- Source income assets: Dividend-paying equities, corporate bonds, government bonds, or other income-oriented securities.

- Diversify exposures: Spread holdings across sectors, issuers, and asset types.

- Rebalance periodically: Keep the fund aligned with its stated mandate.

- Translate all of that into one shareholder experience: A single NAV, a single distribution process, and one wrapper the investor can buy or sell.

That wrapper matters. It can make ownership easier. It can also hide trade-offs.

Why investors like the structure

The appeal is obvious.

You don’t need to build the allocation yourself. You don’t need to decide which bond maturities to own. You don’t need to monitor each dividend payer. You outsource the assembly line.

That’s why this category often appeals to retirees, families seeking portfolio income, and investors who want a middle ground between aggressive equity exposure and a pure income portfolio.

For readers who want a broader primer on pooled structures, Everglow Prosperity’s explanation of a Managed Investment Scheme is a useful framework for understanding how investor capital gets combined and managed inside a shared vehicle.

Where the structure becomes less attractive

The strength of the fund format is delegation. The weakness is also delegation.

When you buy a growth and income fund, you’re not just buying securities. You’re buying the manager’s timing, the manager’s tax profile, the manager’s turnover decisions, and the manager’s definition of risk.

For a mass-market investor, that’s acceptable.

For a client with significant taxable assets, multiple account types, or irregular cash flow needs, that loss of precision is often the biggest flaw in the product.

How These Funds Generate Total Return

Growth and income funds sell a tidy story. Own one fund, get appreciation and cash flow. The problem is that the two return streams often work against each other, and high-net-worth investors feel that compromise more than anyone else.

Total return comes from two sources. First, the underlying holdings rise in value. Second, the fund distributes dividends and bond interest. That sounds efficient. In practice, it often produces a portfolio that is only adequate at both jobs.

The appreciation side has to do the heavy lifting

The growth portion usually comes from the equity sleeve. If those stocks do not compound at a respectable rate, the whole strategy stalls. The income sleeve can cushion volatility and support distributions, but it rarely creates the kind of long-term wealth growth affluent families need.

That is the first mistake investors make. They overrate the income and underrate the need for real equity appreciation.

A fund can hold durable large-cap companies, dividend growers, and some slower-moving value names. That mix may look prudent on paper. It still has to earn its keep. If the equity sleeve is too defensive, the fund sacrifices upside. If it reaches for growth, it often starts to behave like a diluted stock fund with a bond ballast attached.

For a high-net-worth household, that middle ground is not automatically attractive. A large taxable portfolio usually needs sharper role definition than that.

The income side is steadier, but less flexible

The income engine is straightforward. The fund collects cash from stock dividends and bond interest, then distributes part of it to shareholders on the fund’s schedule.

That schedule matters.

Many investors treat fund distributions as if they were engineered around their personal cash needs. They are not. The vehicle decides when income goes out, how much is retained, and how gains and income are blended inside the payout. You receive cash when the fund distributes it, not when your planning calendar calls for it.

That is one reason direct ownership is often superior for affluent clients. If dividend income is part of the plan, a portfolio built around individual securities gives you more control over timing, quality, and tax impact. Commons Capital’s view on a dividend investing strategy built from individual holdings fits that approach better than relying on a pooled fund’s distribution mechanics.

Wrapper differences matter less than investors think

Growth and income strategies usually sit in a mutual fund or ETF wrapper. The wrapper affects trading and fund mechanics. It does not solve the core issue.

A mutual fund prices once at the close. An ETF trades throughout the day. That distinction matters at the margins. It does not change the fact that you still own a pooled structure with shared tax consequences, shared cash flow policy, and limited customization.

High-net-worth investors should stay focused on the core question. Is the pooled format helping the portfolio do its job, or is it forcing unnecessary compromise?

Why the result often falls short

To deliver strong total return, the manager has to get several decisions right at once:

- Build an equity sleeve that can compound.

- Use bonds and income assets that support cash flow without dragging returns.

- Control turnover so distributions and realized gains do not become wasteful.

- Keep the mix aligned with the investor’s objective, not just the fund’s mandate.

That is a demanding assignment. Even when the concept is sound, the execution often lands in the middle. The growth is muted. The income is acceptable but inflexible. The tax profile is mediocre. The investor loses visibility into which holdings are driving performance.

That trade-off may be fine in a smaller account. In a larger portfolio, it is usually a sign to stop buying packaging and start demanding precision.

A More Efficient Alternative The Case for Individual Securities

For many affluent investors, the cleaner answer is direct ownership. Own the stocks. Own the bonds. Build the mix intentionally.

That approach isn’t trendy. It’s just better when the portfolio is large enough to justify customization.

Why direct ownership usually wins

A growth and income fund gives you instant packaging. A direct portfolio gives you precision.

With individual securities, you can decide which companies deserve a place in the equity sleeve and which bonds belong in the income sleeve. You can control maturity structure, issuer quality, dividend exposure, concentration limits, and realized gains. You can also remove positions you no longer want without inheriting the rest of a pooled vehicle.

That matters more than most investors realize.

The three biggest advantages

Cost efficiency

A fund wraps management, administration, trading, and distribution into one product. You pay for that structure whether you need every layer or not.

With direct ownership, you’re paying for portfolio management advice and execution, but you’re not automatically accepting the internal drag of a pooled product. In many cases, especially in larger accounts, that’s the more rational setup.

Transparency

A direct portfolio tells you exactly what you own. No black box. No vague mandate language. No need to infer your exposures from a long fact sheet.

You know which stocks are supposed to drive growth. You know which bonds are there for income, capital preservation, or laddered liquidity. If a holding no longer fits the plan, you can address that holding directly.

Tax control

This is the most underappreciated benefit.

Funds create shared tax consequences. Direct ownership creates investor-specific tax decisions. That difference is enormous in a taxable HNW portfolio.

You can harvest losses selectively. You can defer gains intentionally. You can choose which lots to sell. You can match bond maturities to cash needs. You can redesign the income sleeve around taxable, tax-deferred, and trust accounts instead of forcing everything through one fund wrapper.

For investors weighing the drawbacks of pooled fixed income exposure, this discussion of the bond mutual fund structure is worth reading because many of the same control issues show up on the bond side first.

Fund Investing vs. Direct Ownership: A Comparison for HNW Investors

AttributeGrowth & Income FundDirect Portfolio of Individual SecuritiesSecurity selectionManager chooses the underlying holdings for all shareholdersInvestor and advisor can build around specific goals and constraintsTransparencyLimited to reported holdings and fund disclosuresFull visibility into each stock and bond ownedTax managementShared distributions and embedded gains can create unwanted tax outcomesGains, losses, and income can be managed position by positionCash-flow designDistribution schedule set by the fundIncome can be tailored through bond maturities and dividend sourcesFlexibilityMust accept the whole portfolioCan add, trim, or replace individual holdings selectivelyCustomizationBroad mandate for a general shareholder basePortfolio can reflect concentrated wealth, liquidity needs, and family objectivesBehavioral disciplineSimpler to hold as a single line itemRequires a coherent investment process and oversight

When a fund still makes sense

A fair point matters here. Not every investor should build a direct portfolio.

A fund can still work if:

- Account size is smaller: The portfolio may not justify full customization.

- The investor wants maximum simplicity: One holding may be good enough.

- The account sits in a tax-sheltered structure: Some tax drawbacks matter less there.

That said, most HNW households aren’t looking for “good enough.” They’re looking for a structure that respects complexity instead of flattening it.

If you have substantial taxable assets, convenience shouldn’t outrank control.

My recommendation

Use growth and income funds sparingly. Use direct ownership aggressively where customization matters.

For affluent investors, that usually means building a core portfolio of individual stocks and bonds, then using funds only where they solve a specific problem better than direct ownership can. That’s the right order of operations.

Navigating Risks and Tax Burdens with HNW Portfolios

The main risk in growth and income funds isn’t just market volatility. It’s the combination of market risk plus tax friction.

That combination can subtly weaken a portfolio even when the fund appears diversified.

Interest rates still matter

A fund that mixes stocks and bonds doesn’t become immune to macro conditions. It becomes exposed to more than one source of pressure.

When rates rise, the bond sleeve can struggle. Dividend-oriented equities can also come under pressure if investors rotate toward higher-yielding fixed income or if valuations compress. That’s a problem for a strategy built on the idea that one sleeve cushions the other.

This is one reason direct bond ownership is often superior for HNW investors. A fund investor owns an interest in a moving pool. A direct bond investor owns a maturity date, a stated coupon, and a clearer path to known cash flow if credit quality holds.

Tax drag is the bigger issue

For affluent families, the tax cost can be more damaging than the headline volatility.

According to this discussion of tax implications for growth and income funds, these funds can generate a significant portion of returns as ordinary income taxed at rates up to 37%, compared with long-term capital gains at 20%, creating an annual tax drag of 15-20% that often isn’t obvious to the investor.

That’s the core structural problem in taxable accounts.

The investor sees a diversified fund. The IRS sees a mix of tax character. Those aren’t the same experience.

Why this hits HNW families harder

High earners and affluent retirees often have layered ownership structures. Taxable brokerage accounts. retirement accounts. Trusts. Donor vehicles. Business entities. Sometimes all of them.

A pooled growth and income fund doesn’t adapt itself to those layers very well.

Here’s where the pain usually shows up:

- Ordinary income exposure: Bond interest and some distributions can push tax costs higher than expected.

- Limited harvesting flexibility: You can sell the fund, but you can’t selectively realize losses on the underlying positions.

- Distribution timing: You may receive taxable income in periods when you would have preferred to defer it.

- Blunt asset location: The fund itself doesn’t care whether a given security would be better placed in a tax-deferred or taxable account.

Investors often focus on pre-tax return because the fact sheet makes that easy. Wealth preservation happens after taxes, after distributions, and after avoidable friction.

A better way to manage both problems at once

Risk management and tax management shouldn’t be separate conversations. In an advanced portfolio, they’re part of the same design decision.

A direct portfolio lets you respond more intelligently:

- Adjust bond duration deliberately instead of accepting a pooled sleeve.

- Use individual bonds for known liabilities rather than relying on fund NAV behavior.

- Harvest losses selectively when volatility creates opportunity.

- Place income-heavy assets in the right account types when possible.

For investors who want a practical framework for realizing that tax value, this overview of tax-loss harvesting strategies is especially relevant because the strategy is far easier to execute with direct ownership than inside a traditional fund structure.

The headline lesson is simple. A diversified wrapper can reduce some visible risk while increasing hidden inefficiency. HNW portfolios should be built to avoid that trade.

Evaluating Your Options and Selecting the Right Strategy

If you’re going to use a growth and income fund, evaluate it like a professional. Don’t buy it because the category sounds sensible.

And if you’re going to build a direct portfolio, don’t do it casually. Do it with a clear framework.

How to evaluate a growth and income fund

Start with risk-adjusted performance, not raw return.

The Invesco Growth and Income Fund had $4,384,326,279 in total assets as of February 28, 2026, held 70 securities, and reported a 3-year Sharpe ratio of 0.87, 3-year standard deviation of 12.87%, and 3-year R-squared of 0.92 versus the Russell 1000 benchmark, according to Invesco’s fund page. Those metrics matter because they show how much volatility the manager accepted to generate results.

What to check beyond the headline numbers

A serious review should include:

- Portfolio construction: Does the fund hold the kind of businesses and bonds you want to own?

- Concentration and overlap: Are you buying exposures you already have elsewhere?

- Distribution quality: Is the income profile appropriate for your tax situation?

- Manager discipline: Does the fund appear consistent, or does the mandate drift?

- Fit with your balance sheet: A good fund can still be the wrong holding if it duplicates other assets.

How to evaluate a direct ownership strategy

The analysis is different because the goal is different. You’re not judging a packaged product. You’re designing a portfolio around your life.

That process should start with questions most fund buyers never get asked:

- What cash flow do you need? Not what sounds attractive. What will be spent, and what will be reinvested?

- Which assets belong in taxable accounts? Structure beats product selection.

- What risks are you willing to own directly? Credit risk, duration risk, equity concentration, and liquidity all need explicit decisions.

- Where do you need flexibility? Upcoming liquidity events, philanthropy, concentrated stock unwinds, and estate transfers all matter.

The right standard for affluent investors

The right choice isn’t the one with the easiest ticker symbol. It’s the one that improves your after-tax, after-fee, goal-specific outcome.

That often means using funds selectively and reserving the core role for directly owned securities.

For investors thinking about account protection and broader tax enforcement issues, Attorney Stephen A Weisberg’s article on Can The IRS Take Your 401k Understanding Your Rights And Protections is a helpful reminder that account structure and legal context matter just as much as investment selection.

The best portfolio isn’t the one that looks balanced on paper. It’s the one that aligns with your taxes, your spending, your timeline, and your actual sources of risk.

My recommendation

If you must use a growth and income fund, choose one only after reviewing risk-adjusted metrics, holdings, and tax implications.

If your portfolio is substantial, your income needs are nuanced, or your tax situation is complex, build around individual stocks and individual bonds first. Then use funds only where they add something specific that direct ownership can’t deliver efficiently.

Conclusion Building Your Personalized Growth and Income Plan

Growth and income funds solve a real problem. They try to blend appreciation and cash flow in one vehicle. That’s useful, and for some investors it’s enough.

For high-net-worth investors, “enough” usually isn’t the right standard.

The trade-offs are clear. A fund can offer convenience and broad diversification, but it can also reduce control, blur tax consequences, and force you into a structure designed for the average shareholder. That’s rarely ideal when your assets, tax profile, and planning goals are anything but average.

Direct ownership gives you more levers.

You can choose the companies that deserve a place in the growth sleeve. You can build the income sleeve bond by bond. You can decide where to realize gains, where to harvest losses, and where each asset belongs across taxable and tax-advantaged accounts. You can create a portfolio that matches your actual life instead of adapting your life to a generic product.

That’s the better framework.

There’s still a role for growth and income funds in some portfolios. They can work as a satellite holding, a transitional allocation, or a simple option in accounts where customization isn’t worth the effort. But they shouldn’t be the automatic answer for affluent families.

According to Capital Group’s advisor material, superior risk-adjusted performance comes from strategic allocation, and an advisor can help benchmark a custom portfolio against relevant indices and allocate 20-40% for portfolio income to pursue target yields and appreciation while mitigating risks like credit and reinvestment through high-quality holdings. I agree with the allocation point. I just don’t think a pooled fund should be the default way to express it.

A serious growth-and-income strategy should be built, not bought off the shelf.

If you’re evaluating whether to keep a fund, replace it, or redesign the entire structure around individual securities, focus on three questions:

- Is the portfolio tax-aware enough for your bracket and account mix?

- Do you have enough control over cash flow and risk?

- Can you explain exactly why each major holding is there?

If the answer to any of those is no, the portfolio needs work.

If you want a growth-and-income strategy built around your actual tax situation, income needs, and long-term goals, talk with Commons Capital. We help high-net-worth individuals, families, and institutions design portfolios that go beyond off-the-shelf funds and reflect the realities of complex wealth.