You’ve spent years controlling the variables that matter in retirement. Asset allocation, tax location, concentrated stock risk, liquidity events, estate structures, real estate exposure. Then Medicare enters the picture and introduces one of the least appreciated threats to a high-net-worth plan: healthcare costs that can remain open-ended under Original Medicare.

That’s why medicare supplement insurance options deserve the same analytical discipline you’d apply to a bond ladder or trust structure. For affluent retirees, Medigap isn’t mainly about buying more insurance. It’s about converting an uncertain liability into a planned expense, preserving freedom of provider choice, and preventing healthcare decisions from spilling into portfolio decisions at the wrong time.

If you need a clean primer before weighing plans, this guide on what a Medicare Supplement Plan is is a useful starting point.

Navigating Your Medicare Supplement Insurance Options

Most retirees first encounter Medigap as a list of lettered plans. That framing misses the key decision.

The better question is this: which structure best protects your balance sheet while preserving access to care you want to use?

A wealthy household usually isn’t trying to minimize this month’s premium at all costs. It’s trying to avoid three expensive mistakes:

- Accepting unlimited medical cost drift: Original Medicare leaves gaps that can create irregular, hard-to-budget expenses.

- Losing provider flexibility: A narrow network may be acceptable for some households, but many affluent retirees value unrestricted specialist access.

- Applying too late: Delaying the decision can turn a straightforward purchase into an underwriting problem.

A Medigap policy works best when you treat it like financial infrastructure. It sits alongside cash reserves, long-term care planning, tax planning, and estate documents.

Early in the process, focus on four questions:

- Do you want maximum predictability? If yes, richer Medigap designs usually deserve attention.

- How often do you expect to use outpatient care? Frequent office visits can change the Plan G versus Plan N math.

- Will you travel often or live in multiple locations? Mobility increases the value of broad provider access.

- Are you entering a protected enrollment window? Timing can matter as much as plan design.

A good Medigap decision does something simple but powerful. It reduces the chance that a health event forces you to sell assets, trim gifting, or rethink retirement cash flow. That’s the frame to carry through every plan comparison that follows.

Medigap as a Core Wealth Preservation Strategy

A retiree with an $8 million portfolio can absorb a five-figure medical bill. The larger risk is that unpredictable healthcare expenses arrive at the wrong time, force avoidable withdrawals, and weaken a distribution plan that was designed to last for decades.

This is the primary role of Medigap for affluent households. It converts part of retirement healthcare risk from an irregular liability into a budgeted expense that can be coordinated with withdrawal strategy, liquidity reserves, and estate planning. Used that way, Medigap functions less like a retail insurance purchase and more like a balance-sheet defense decision.

Original Medicare leaves cost sharing in place and does not impose a standard annual out-of-pocket maximum the way many employer or Medicare Advantage plans do. For a high-net-worth family, the practical concern is not insolvency. It is loss of control. Large or recurring medical bills can force distributions from taxable accounts during down markets, reduce flexibility around Roth conversions, and narrow the margin for planned gifting or trust funding.

Why this matters for wealth preservation

Wealthy retirees often insure against risks they could technically self-fund because volatility itself has a cost. An unplanned $20,000 to $50,000 draw from the portfolio may not change lifestyle today, but it can alter the after-tax sequence of withdrawals, reduce assets left compounding, and create avoidable friction for a surviving spouse or adult child managing finances later.

A Medigap premium is easier to model than open-ended claims exposure. That difference affects several parts of a financial plan:

- annual cash flow forecasting

- liquidity bucket sizing

- tax-aware withdrawal sequencing

- charitable giving schedules

- estate liquidity for heirs and trustees

The result is that poor medical decisions can become poor financial decisions later. Households that are unsure what a specialist visit, outpatient procedure, or hospital follow-up may cost are more likely to delay care or choose based on billing uncertainty rather than clinical fit.

Predictability has portfolio value

For affluent retirees, the relevant comparison is rarely premium versus no premium. It is fixed cost versus variable draw on investable assets.

That distinction matters most in years when markets are down and healthcare usage is up. Selling appreciated positions can create tax drag. Selling depressed positions can lock in losses and increase sequence risk. Pulling extra cash from a concentrated stock position can disrupt a long-term diversification plan. A stronger Medigap structure reduces the odds that healthcare spending becomes the reason those decisions happen on a bad timetable.

This also affects access. Households that want treatment at major academic centers, prefer nationally recognized specialists, or split time between states usually place a high value on provider flexibility. Medigap can support that objective while keeping the cost-sharing side of the equation more stable.

For broader context on insurance as part of total balance-sheet defense, Commons Capital’s discussion of wealth preservation strategies offers a useful framework.

The often-overlooked family office benefit

Medigap can also simplify administration. Predictable coverage reduces claim surprises, lowers the chance that family members must sort through unexpected bills during a health event, and makes ongoing cash management cleaner for a spouse, trustee, or advisory team.

That administrative clarity has economic value. Retirement healthcare planning works better when the portfolio remains focused on income, growth, and legacy goals instead of absorbing avoidable cost shocks from Medicare gaps.

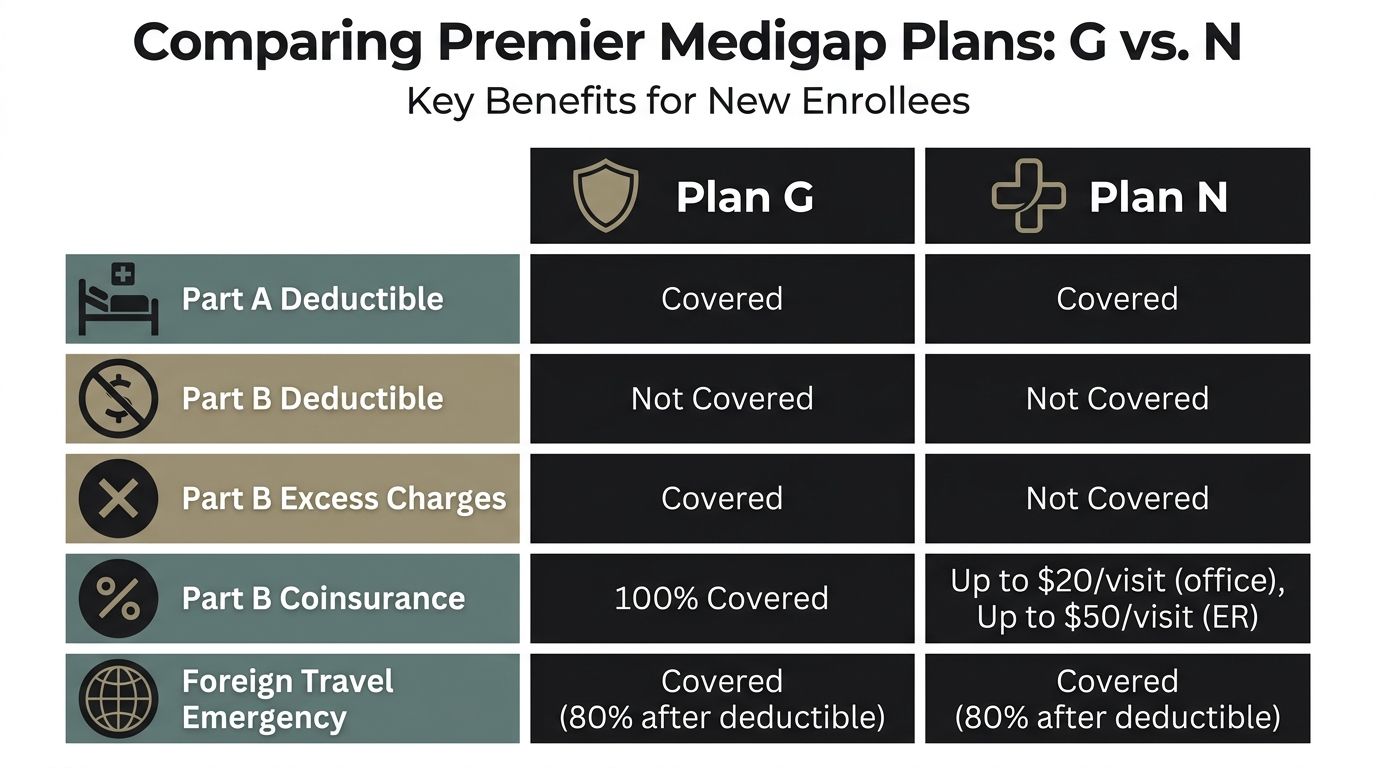

Comparing the Premier Medigap Plans G and N

If you’re newly eligible for Medicare, the market has already made one major decision for you. Plans that covered the Part B deductible stopped being sold to newly eligible enrollees after the 2020 MACRA change. That shift helped push Plan G to 5.7 million enrollees, making it the dominant high-coverage option for new buyers, as noted in this Mark Farrah Associates enrollment review.

That popularity isn’t accidental. Plan G sits near the top of the market because it offers broad protection with relatively simple budgeting.

Here’s the fast comparison first.

| Feature | Plan G | Plan N | High-Deductible Plan G |

|---|---|---|---|

| Part A hospital coinsurance and hospital costs | Covered | Covered | Covered after deductible threshold is met |

| Part B deductible | Not covered | Not covered | Not covered, and you satisfy the high deductible before plan payments begin |

| Part B excess charges | Covered | Not covered | Covered after deductible threshold is met |

| Part B coinsurance and copays | Covered | Office and ER copays can apply | Covered after deductible threshold is met |

| Foreign travel emergency | Covered at 80% after deductible, up to lifetime max | Covered at 80% after deductible, up to lifetime max | Covered after deductible threshold is met |

| Best fit | Retirees who want maximum simplicity | Retirees comfortable with some usage-based cost sharing | Retirees with strong liquidity who want lower premiums |

Plan G for households that want near-frictionless coverage

Plan G is often the cleanest answer for clients who don’t want medical billing complexity inserted into retirement.

Under the standardized 2026 Medicare comparison structure on Medicare.gov’s Medigap plan benefits chart, Plan G covers:

- Part A coinsurance and hospital costs, including up to 365 additional days after Medicare benefits are used

- Part B coinsurance and copayments

- blood

- Part A hospice care coinsurance or copayment

- skilled nursing facility coinsurance

- the Part A deductible

- foreign travel emergency at 80% after a $250 deductible, with a $50,000 lifetime limit

For newly eligible buyers, the main thing Plan G doesn’t cover is the Part B deductible. The verified benchmark cited in the source material places that deductible at $283 for 2026.

That leaves a simple planning model. Premium plus one small known annual deductible, then broad protection after that.

For retirees who value simplicity, Plan G can turn healthcare from a volatile category into a routine operating expense.

Plan N for premium-sensitive clients who still want broad protection

Plan N is often misunderstood. It is not a stripped-down product. It preserves many of the same core protections as Plan G, but shifts more outpatient friction back to the policyholder.

Plan N includes the major hospital protections and foreign travel emergency benefit structure. The trade-off appears in outpatient usage and excess charges.

Under the standardized benefit design, Plan N can require:

- up to $20 copays for office visits

- up to $50 copays for emergency room visits, waived if admitted

- payment exposure for Part B excess charges because Plan N doesn’t cover them

That means Plan N tends to work better when the retiree:

- doesn’t expect frequent office visits

- is comfortable tracking copays

- confirms their physicians don’t generate problematic excess charges

- wants to reduce premium spend without abandoning traditional Medicare plus Medigap

High-Deductible Plan G for liquidity-rich retirees

There’s a very different type of buyer who should consider high-deductible Plan G.

This structure asks you to retain more initial risk in exchange for lower premiums. For 2026, the high-deductible Plan G threshold is $2,950, based on the benchmark information in the verified data and Medicare plan comparison framework.

That sounds unattractive until you evaluate it through a portfolio lens.

If a retiree has ample liquid reserves and strong risk tolerance for routine medical variability, high-deductible Plan G can act like a self-insured first-loss layer. The plan still provides catastrophic structure after the deductible threshold, but it allows the household to keep monthly insurance spend lower.

Decision criteria that matter more than premium alone

Total out-of-pocket exposure

Plan G usually wins on pure predictability. After the deductible, there’s very little left to manage for Medicare-covered services.

Plan N introduces more moving parts. That may be perfectly acceptable for a healthy retiree with modest outpatient usage, but it creates more variance.

High-Deductible Plan G creates the largest retained first-dollar exposure. It makes sense only if that retained exposure feels operationally trivial relative to your liquid assets.

Premium efficiency

Plan N often appeals to buyers who believe they won’t use much care. That logic can be sound, but only if the savings are meaningful and the household remains comfortable with outpatient copays and excess-charge risk.

High-Deductible Plan G can produce a much stronger premium reduction for the right client. The key is discipline. If lower premiums free cash for consumption, the structure may not improve overall planning. If they preserve investable cash flow or reduce fixed retirement burn, the math gets more compelling.

Administrative burden

Many affluent households underprice their own time.

Plan G is usually the easiest to live with. Fewer surprise bills. Fewer coverage questions. Less billing cleanup.

Plan N requires more attention. High-Deductible Plan G requires the most psychological comfort, because the household must absorb early-year spending before the policy begins paying under its high-deductible design.

A practical way to choose

Use this framework.

| If this sounds like you | Usually the strongest fit |

|---|---|

| “I want the cleanest billing experience and broadest protection available to new enrollees.” | Plan G |

| “I’m comfortable with office visit copays and I want to trim premium outlay.” | Plan N |

| “I have strong liquidity, low debt, and I’m happy to self-fund a larger deductible.” | High-Deductible Plan G |

The core insight is that these aren’t just health plan choices. They are risk-retention choices. Plan G transfers more medical cost volatility to the insurer. Plan N shares more of it. High-Deductible Plan G retains more of it inside your household balance sheet.

For a multimillion-dollar portfolio, that framing is the one that matters.

Decoding Medigap Costs and Medical Underwriting

Two people can buy the same standardized Medigap plan and have very different long-term experiences. The benefits are standardized in most states. The pricing path and underwriting outcome are not.

That’s where many otherwise discerning retirees make avoidable mistakes.

Why the cheapest quote can be the wrong quote

Insurers generally price Medigap policies using one of three methods:

- Community-rated: the premium is not based on your age

- Issue-age-rated: the premium is based on your age when you buy

- Attained-age-rated: the premium rises as you get older

For a high-net-worth retiree, the lowest introductory premium isn’t automatically the best answer. Stability often matters more than a short-term discount.

A retirement that may last decades needs cost structures you can live with in your late seventies and eighties, not just in your first year on Medicare. If an insurer’s pricing method introduces more age-related drift, the policy may look efficient at purchase and less attractive later.

The right way to evaluate Medigap pricing is the same way you’d evaluate any long-duration liability. Focus on durability, not just entry price.

Underwriting is where timing becomes money

Medical underwriting is the point where insurance planning stops being theoretical.

According to Medicare.gov’s Medigap guidance, outside guaranteed issue periods, insurers can deny coverage or charge materially higher premiums based on health status. The verified data also notes that conditions such as diabetes or heart disease can increase the risk of denials for late applications.

That changes the entire decision calculus.

A retiree may think delaying Medigap keeps options open. In practice, delaying can remove options.

The financial cost of waiting

When people apply outside protected windows, several bad outcomes can occur:

- A denial: You lose access to the plan design you wanted.

- A rating-up: You’re offered coverage, but at a price that permanently weakens retirement cash flow.

- A waiting period issue: Pre-existing condition concerns can complicate the start of meaningful protection.

This matters even more for globally mobile households. A business owner with overseas residences, an entertainment client working seasonally, or a recently retired executive staying on employer coverage may assume they can handle Medigap later. Sometimes they can. Sometimes that assumption becomes expensive.

Questions worth asking before you apply

Use a disciplined checklist:

What rating method does this carrier use?

You’re not just buying today’s premium.Am I still inside a guaranteed issue or open enrollment window?

If yes, that can be more valuable than any premium discount.Do I have pre-existing conditions that could change carrier decisions?

If yes, timing is critical.Will my travel or employer transition create a gap in proof of prior coverage?

Documentation can matter.

The larger point is simple. For Medigap, eligibility strategy and price strategy are inseparable. The best plan on paper has no value if you wait long enough to lose access to it on favorable terms.

Mastering Enrollment Windows and Guaranteed Issue Rights

Most costly Medigap mistakes don’t come from choosing the wrong lettered plan. They come from choosing at the wrong time.

That’s especially true for affluent households with nonstandard retirement paths. Selling a company, phasing out of a law practice, ending executive group coverage, or spending part of the year abroad can all create enough complexity to make a protected enrollment window easy to miss.

The window that matters most

Your one-time Medigap open enrollment period is usually the cleanest opportunity to buy coverage because insurers generally can’t use your health history to block the purchase during that protected period.

For practical planning, that means you should treat Medicare Part B timing as a strategic event, not an administrative footnote.

If you’re approaching retirement from an employer plan, don’t wait until the last minute to coordinate:

- Medicare Part B effective date, employer coverage end date, Medigap application timing, and Part D planning if you’ll need standalone drug coverage

HNWI scenarios that need advance planning

Leaving an executive group health plan

Many senior executives carry extensive employer coverage and assume they can “switch later.”

That can work, but only if the transition is coordinated carefully. A delayed Part B enrollment can shift when your Medigap protections begin. If there’s confusion around when employer coverage ends, the clean protected path can become messier than expected.

Selling a business

Business owners often focus on liquidity, tax consequences, and succession terms. Health coverage gets pushed down the list.

That’s a mistake. Once the business sale closes and employer-related coverage changes, you need a documented path into Medicare and Medigap. Waiting because “we’ll handle insurance next quarter” can create underwriting exposure.

International travel or split residency

Affluent retirees who spend substantial time outside the United States often delay domestic insurance decisions because they feel healthy or carry other coverage.

That creates risk. Medigap planning depends on timing and proof. If you’re moving between countries or maintaining several residences, paperwork discipline matters.

Keep copies of employer coverage notices, termination letters, and any proof of prior creditable coverage in one place. Those documents can be as important as the application itself.

The mistake that feels harmless

A brief lapse in attention can become a permanent pricing problem.

People often assume they can shop for Medigap whenever they’re ready, the same way they might shop for auto or homeowners coverage. That isn’t how this market works. Protected rights are strongest in specific windows. Outside those windows, health status can shape the result.

A working checklist for enrollment execution

- Start early: Review Medicare and Medigap timing before your current coverage ends.

- Document coverage transitions: Save every notice related to employer, COBRA, or other prior coverage.

- Align spouses deliberately: Two people in the same household may not have the same enrollment timeline.

- Confirm plan availability in your state: Standardization is broad, but not identical across every state structure.

- Coordinate with the rest of the retirement plan: Enrollment timing affects cash flow, provider access, and risk management.

This is one area where precision matters more than optimization. The right move, executed on time, is usually worth more than chasing a slightly lower premium after protections disappear.

Medigap vs Medicare Advantage for Asset Protection

A retired executive with an $8 million portfolio can absorb a higher monthly premium. What is harder to absorb is a care delay, an out-of-network cancer center, or repeated prior authorization disputes during a year when health risk rises and decision quality matters most.

This is the fundamental divide between Medigap and Medicare Advantage for affluent retirees. The comparison is not mainly about advertised premiums. It is about which structure better protects liquidity, provider choice, and the family’s ability to make medical decisions without insurer-imposed friction.

Medicare Advantage can work well for retirees who are comfortable with managed care rules and local provider networks. A high-net-worth household often has a different objective. It wants to reduce the odds that a medical event turns into a forced financial decision, especially when the retiree spends time in more than one state, uses major referral centers, or values direct access to top specialists.

Original Medicare with Medigap generally offers broader provider flexibility because any physician or hospital that accepts Medicare can be used without building the care plan around a private network. That freedom has financial value. It can preserve continuity of care after a move, make second opinions easier to obtain, and reduce the risk that treatment decisions are shaped by network design rather than clinical judgment.

For asset protection, the hidden cost of a lower-premium Medicare Advantage plan is not always the out-of-pocket maximum on paper. The larger risk is constraints. A restricted network, referral rules, or prior authorization can introduce delay at exactly the point when a retiree is trying to secure the best available care. For a family with substantial assets, the problem is less about whether a claim is covered and more about whether the plan interferes with fast access to preferred physicians and institutions.

That distinction matters more at higher wealth levels. Households that have spent decades building capital usually insure against low-frequency, high-severity disruptions. Medigap fits that logic. It converts a larger share of healthcare spending into a known premium and reduces exposure to operational surprises that can disrupt travel plans, relocation decisions, or complex treatment coordination.

Medical coverage also sits inside a broader asset-defense structure. A retiree who wants freedom to choose providers may also need parallel planning for long-term care exposure, estate administration, and incapacity risk. Commons Capital’s perspective on protecting assets from nursing home costs is relevant because healthcare funding decisions and long-term custodial care planning affect the same balance sheet. The legal side matters too, especially for families using trusts to protect your family’s legacy.

Medigap often serves affluent retirees better because it protects optionality. In wealth management, optionality is rarely cheap. It is often valuable precisely when conditions become difficult.

Integrating Your Medigap Choice into a Cohesive Financial Plan

Once you’ve chosen among your medicare supplement insurance options, the work isn’t finished. The plan has to be integrated into the household balance sheet.

That means treating the premium as a non-discretionary protection cost, not a lifestyle expense. It belongs in the same category as property insurance, umbrella coverage, and essential tax payments.

Match the plan to the portfolio

The most useful way to integrate Medigap is by matching the plan design to the household’s liquidity profile and tolerance for retained risk.

For some retirees, standard Plan G will be the cleaner fit because it minimizes surprise medical billing. For others, High-Deductible Plan G can reduce monthly premiums by 30% to 50% for affluent retirees with more than $500k in assets who can comfortably self-fund the deductible, according to Mutual of Omaha’s discussion of choosing a Medicare supplement plan. The verified data also places the 2026 high-deductible Plan G threshold at $2,950.

That opens a planning opportunity.

A liquidity-rich household can reserve the deductible in cash or short-duration instruments, then redirect the lower premium burden toward investment, gifting, travel, or other retirement priorities. The key is intention. Don’t choose the high-deductible structure unless that deductible is easy for the household to absorb.

Coordinate healthcare planning with estate planning

Healthcare cost control supports estate efficiency.

A retiree who removes medical cost volatility from the annual budget has a clearer framework for gifting, trust funding, charitable commitments, and survivor income planning. That’s one reason healthcare choices shouldn’t sit outside the estate conversation. If you’re reviewing broader legacy structures, this overview of trusts to protect your family’s legacy is a practical companion resource.

Put the decision into the advisory process

A Medigap decision should flow into:

- annual retirement income planning

- cash reserve policy

- spousal coverage coordination

- estate liquidity planning

- family communication around healthcare preferences

If you want that choice reflected inside a larger planning framework, Commons Capital’s perspective on working with a retirement financial advisor is one useful place to start.

The right Medigap plan doesn’t maximize bragging rights on premium savings. It protects flexibility, reduces balance-sheet surprises, and helps the rest of the wealth plan function as intended.

Commons Capital works with high-net-worth individuals, families, business owners, and retirees who need healthcare decisions aligned with broader wealth strategy. If you want help evaluating how a Medigap choice fits into retirement cash flow, portfolio risk, and long-term asset protection, you can learn more at Commons Capital.