When inflation is running hot, the old playbook of stashing cash and holding traditional bonds just won't cut it. To protect your purchasing power, you must shift your focus toward assets that can hold—or even grow—their value. This guide on how to invest during high inflation will explore strategies centered on real assets (like real estate and commodities), shares in companies with unshakeable pricing power, and specific tools like Treasury Inflation-Protected Securities (TIPS).

This isn't about just weathering the storm; it's about making sure your hard-earned capital doesn't get eroded while you wait for calmer seas. By understanding which investment strategies work in an inflationary environment, you can position your portfolio for resilience and growth.

How to Protect Your Portfolio From High Inflation

High inflation can feel like a direct assault on your wealth. For families and individuals managing portfolios of $500,000 or more, the stakes are even higher, as every percentage point of lost value has a much greater real-world impact. It's not just a number on a screen; it's your financial security.

We're going to skip the generic advice you can find anywhere. Instead, I'll walk you through the practical strategies our team uses to help clients—from entrepreneurs to established families—navigate these tricky economic waters. This is an insider's look at how to diagnose your portfolio's inflation exposure, pick assets that thrive under pressure, and make the advanced adjustments that truly matter.

The goal here is to leave you with a clear, actionable game plan. We want to transform your portfolio from a passive victim of inflation into a resilient engine for long-term growth.

Why Your "Balanced" Portfolio Is Suddenly at Risk

In normal times, a simple mix of stocks and bonds does the job. But high inflation throws a wrench in the works, turning once-safe strategies into potential liabilities.

Here’s a quick look at how high inflation typically impacts the core of most investment portfolios. This can help you spot the potential weak points in your own holdings right now.

How Inflation Affects Your Core Investments

Understanding these dynamics is the first step. For those managing significant wealth, simply knowing this isn't enough—you have to act on it. A solid foundation is understanding the different asset allocation strategies for a volatile market.

This guide will build on those core principles, giving you the specific tools needed to confront the unique challenge of inflation head-on. By the time we're done, you’ll have a much clearer picture of how to position your investments to not only survive this period but to come out stronger on the other side.

Pinpointing Your Portfolio's Inflation Vulnerabilities

Before you make a single move, you have to run a full diagnostic on your current holdings. Think of it as an "inflation stress test" for your wealth. This is about going much deeper than just your stock-to-bond ratio. It's a granular look at which assets will get eaten away by rising prices and which ones might actually hold up.

Without a clear map of your portfolio's specific weak spots, any adjustments you make are just guesswork. And in this environment, guessing is a great way to lose money.

Looking Under the Hood of Your Holdings

Inflation is not a tide that lifts or sinks all boats equally. Some of your assets are built to weather the storm, while others will take on water fast. Your job is to figure out which is which by digging into what you actually own.

Let's start with your stocks. A company's survival in an inflationary world boils down to one thing: pricing power. Can it pass on its rising costs for labor, materials, and shipping to customers without them walking away?

- The Squeezed: Companies fighting for customers in crowded markets with paper-thin margins are in real trouble. If they can't raise prices, their earnings get crushed.

- The Resilient: Businesses with die-hard brand loyalty, must-have products, and light debt loads often do just fine. They can protect their margins and sometimes even increase profits.

This same logic applies to everything in your portfolio, even assets that look rock-solid on paper.

One of the biggest mistakes I see is assuming a long-term contract equals safety. When inflation is high, that fixed income stream is a depreciating asset. Every payment is worth less than the last. You have to identify and quantify that risk.

Stress-Testing Beyond Stocks and Bonds

For the kinds of substantial portfolios we manage, this analysis has to cover alternative and private investments. This is where the risks can be a lot harder to spot.

Take real estate. That commercial property with a 10-year, fixed-rate lease looked like a genius move a few years ago. Today, as inflation chews through the value of that fixed rent, the property's costs—maintenance, taxes, utilities—are all going up. You're left with a shrinking net income, year after year.

The same goes for private equity. You need to take a hard look at those portfolio companies. Are they loaded up with debt? When the Fed raises interest rates to combat inflation, those debt payments can balloon, gutting profits and putting the entire investment at risk.

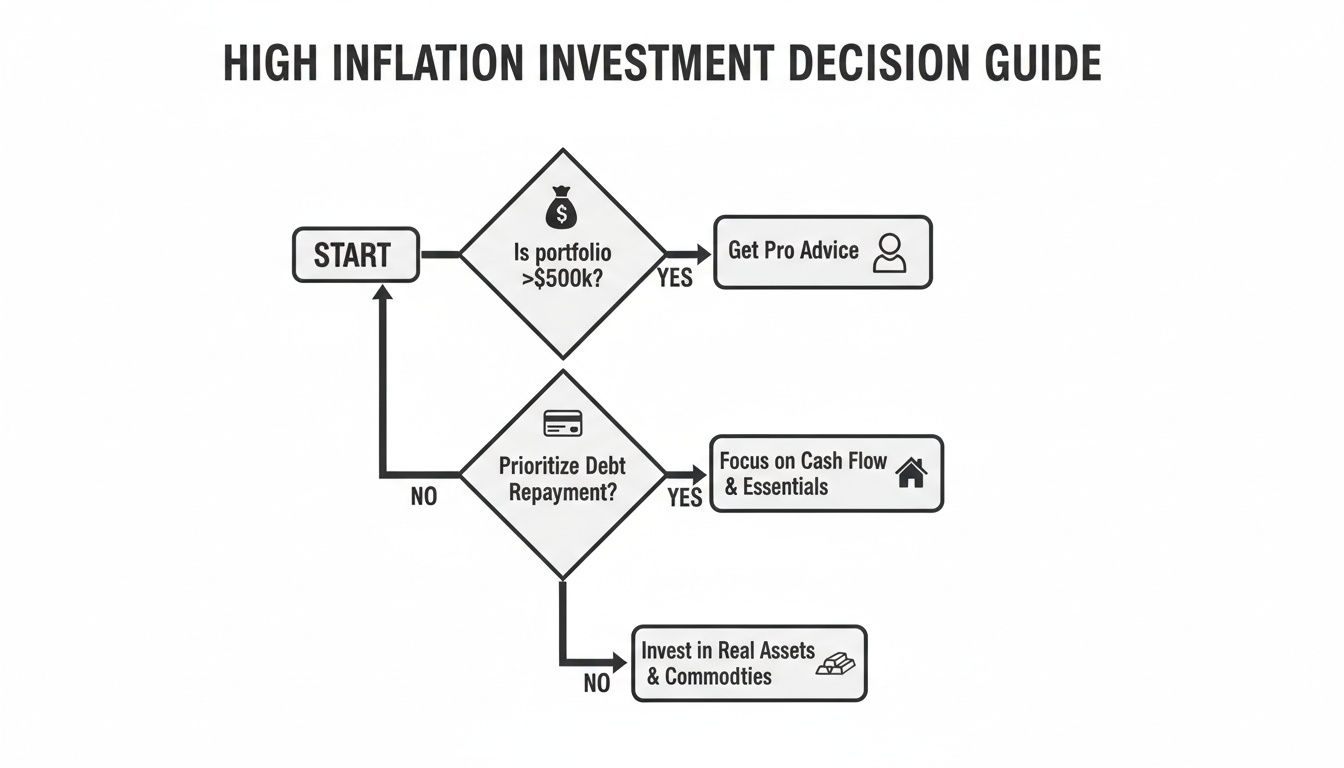

This decision tree gives a good visual of that first critical question high-net-worth investors should be asking themselves.

The flowchart drives home a key point: once your portfolio crosses a certain threshold, like $500,000, the complexity of navigating inflation often means it’s time to bring in professional guidance.

Once you’ve gone through this diagnostic, you’ll have a clear, prioritized list of your portfolio’s weak points. This isn't a moment to panic—it's the foundation for building a smart, durable strategy. Now you know exactly where you need to focus to protect and grow your wealth.

Using Real Assets to Your Advantage

When inflation starts eating away at the value of cash, the most intuitive defense is often the best one: tangible assets. The trick to investing during high inflation is to pivot toward things with physical value—investments you can see and touch, or those whose profits are directly tied to rising prices.

These "real assets" have a built-in hedge, since their prices tend to rise right alongside, or even faster than, the inflation rate.

For high-net-worth families, this strategy goes well beyond just buying another property. The real work is in channeling capital into the right kinds of commercial real estate, specialized REITs, and commodities to build a portfolio that can truly weather the storm.

Rethinking Your Real Estate Exposure

Owning property is a start, but it’s just one piece of the puzzle. To actually protect your wealth, your real estate holdings need to be structured to benefit from rising prices, not get steamrolled by them. As we’ve seen, locking yourself into long-term, fixed-rate leases can be a massive liability in an inflationary world.

The smarter play is to focus on properties with shorter lease durations or, better yet, leases with inflation escalator clauses baked right in. These clauses automatically push rents up based on a metric like the Consumer Price Index (CPI), making sure your income stream doesn’t fall behind.

Some of the most effective real estate strategies we've seen include:

- Commercial Properties: Warehouses, logistics centers, and self-storage facilities are seeing incredible demand, which gives landlords more power to adjust rents frequently.

- Multifamily Housing: Apartment buildings are a classic inflation hedge, giving you the chance to reset rents to current market rates each time a lease turns over.

- Specialized REITs: Look past the standard office and retail trusts. Real Estate Investment Trusts focused on high-demand sectors like data centers, cell towers, and industrial real estate are far more resilient.

A thoughtfully structured real estate allocation can deliver both an inflation-adjusted income stream and long-term capital growth. We've put together a deeper analysis on investment management for real estate that walks through these nuances for sophisticated investors.

The Strategic Role of Commodities

Commodities are the basic ingredients of our economy, so their prices are a direct component of inflation itself. This makes them one of the most effective hedges you can own. This broad category covers everything from precious metals and energy to the food we eat.

When trust in fiat currency erodes, capital has historically fled to assets with intrinsic, time-tested value. Commodities, and gold in particular, represent a fundamental store of wealth that operates outside the confines of the traditional financial system.

For thousands of years, gold has been the go-to inflation hedge. It has served as a reliable store of value and tends to shine when confidence in paper money is low. For anyone looking to protect their wealth during periods of high inflation, a modern guide to investing in gold bullion is a great place to start.

But gold is just one piece of the commodity puzzle. A broader strategy can add another powerful layer of diversification.

- Energy: Since oil and gas prices are a primary driver of inflation, investing in energy producers or ETFs can offer a direct hedge against rising fuel and utility bills.

- Industrial Metals: Copper, aluminum, and other base metals are the building blocks of manufacturing and construction. Their prices often climb during periods of economic growth, even when that growth comes with inflation.

- Agriculture: "Soft" commodities like wheat, corn, and soybeans are essentials. Their prices are directly linked to the cost of food, making them a very practical hedge against your own rising grocery bills.

There are a few ways to get exposure, each with its own risk profile. You can invest in the stocks of commodity-producing companies, whose profits often surge when prices for their materials spike. For simpler, more diversified access, commodity-focused Exchange-Traded Funds (ETFs) can give you broad exposure to a whole basket of raw materials in a single trade.

Selecting Resilient Equities and Bonds

It’s a common—and frankly, expensive—myth that all stocks get hammered during inflation. The real key to investing when prices are spiraling isn't to run from the stock market, but to become far more discerning about what you own.

We’re going to zero in on the specific DNA of companies that can hold their ground, or even thrive, when costs are on the rise. We'll then turn our attention to the other side of your portfolio—fixed income—and explore why your trusty old bonds might actually be a liability right now.

Finding Equities with Pricing Power

When inflation bites, some companies get squeezed. Their costs for everything from labor to shipping go up, and their margins get crushed. But other businesses have a secret weapon: they can simply pass those higher costs on to their customers.

This ability to raise prices without losing business is called pricing power. It is the single most important quality I look for in a stock during inflationary times.

So, what does a company with true pricing power look like? They usually have a few things in common:

- Dominant Market Position: They’re the leader of the pack, with a deep moat and very little real competition.

- Inelastic Demand: They sell things people need, not just want. Customers keep buying, even when the price tag gets a little bigger.

- A Powerful Brand: Think of brands that are so trusted, customers willingly pay a premium. It’s a stamp of quality they won’t trade for a cheaper alternative.

- Low Capital Needs: These are businesses that don't need to constantly pour money into new factories or heavy equipment, insulating them from the rising costs of those assets.

You’ll often find these kinds of businesses in sectors like consumer staples—the companies making the food and household goods we all buy—and healthcare, especially pharmaceuticals and medical device makers. Their products are non-negotiable for most people, giving them a durable edge.

History shows us that abandoning stocks entirely during an inflationary storm is often a mistake. Thoughtful selection is a much smarter play. The goal is to find quality businesses that can protect their profit margins, no matter what the broader economy throws at them.

What History Tells Us About Stocks

It might feel counterintuitive, but equities have proven to be a reliable long-term hedge against inflation. Even when price pressures were intense, strong companies found ways to adapt and keep growing their earnings.

Take the high-inflation era of the late 1970s and early 1980s. When U.S. inflation peaked at a staggering 13.5% in 1980, the S&P 500 still delivered long-term returns that outpaced inflation. Digging into the data reveals there isn't a direct, negative correlation between high inflation and poor stock performance over the long haul. This underscores why maintaining a solid allocation to high-quality companies is so critical, especially for those managing portfolios of $500k or more.

You can dive deeper into how different assets behave in the full analysis on how inflation affects investments.

Swapping Out Traditional Bonds for Smarter Alternatives

While equities call for selectivity, your traditional bond holdings probably need a complete rethink.

Long-term, fixed-rate bonds are one of the most vulnerable assets when inflation is high. As central banks jack up interest rates to cool the economy, your existing bonds with their lower yields suddenly look a lot less attractive. Their market price drops. It’s a painful, but predictable, outcome.

Fortunately, there are much better tools for the job.

Treasury Inflation-Protected Securities (TIPS)

TIPS are government bonds that offer a direct and explicit shield against inflation. It’s right there in the name. Here’s how they work:

- The bond’s principal value adjusts up or down based on changes in the Consumer Price Index (CPI).

- Your interest payments, which you receive twice a year, are then calculated on that new, inflation-adjusted principal.

This one-two punch ensures that both your initial investment and your income stream are protected from being eaten away by rising prices.

Floating-Rate Debt

Another powerful tool for this environment is floating-rate debt. Unlike a traditional bond with its interest rate set in stone, the coupon on a floating-rate instrument resets periodically—say, every 90 days.

It’s typically tied to a benchmark rate like SOFR (Secured Overnight Financing Rate). So when the Federal Reserve hikes rates to fight inflation, the interest you receive automatically floats up with them. This provides a fantastic, natural buffer for your portfolio’s income stream and sidesteps the duration risk that hammers fixed-rate bonds.

Exploring Advanced Inflation-Hedging Strategies

While standard inflation hedges like TIPS and real assets are a solid foundation, for those managing significant wealth, there are more powerful tools in the shed. When you're looking to shield a larger, more complex portfolio from inflation, moving into advanced strategies can add a much-needed layer of both protection and opportunity.

These approaches often lead us into the private markets. They demand a much deeper level of due diligence and expertise, no question. But the payoff can be unique benefits that are simply out of reach in the public markets, making them a critical piece of a serious wealth preservation plan.

Unlocking the Potential of Private Markets

Private markets offer a compelling lane change from publicly traded stocks and bonds, especially when inflation is the main event. These investments are less tethered to the daily mood swings of the stock market and can give you direct access to income streams built to withstand inflation.

For sophisticated investors, two areas really stand out right now: private credit and private equity.

The Power of Private Credit

Private credit is exactly what it sounds like: lending directly to companies. The real advantage here is that the terms are often structured to heavily favor the lender. And in an inflationary world, the most attractive feature is the widespread use of floating-rate loans.

Unlike fixed-rate bonds that get hammered as interest rates climb, these loans have interest payments that adjust upward along with a benchmark rate. This means that as central banks hike rates to fight inflation, the income from these investments automatically rises with them. It's a powerful mechanism.

This strategy brings a few key advantages to the table:

- Direct Inflation Hedge: The floating-rate structure is a natural buffer, helping your income stream keep pace as rates move.

- Higher Yields: To compensate for being less liquid, private credit typically offers higher yields than what you'll find in public debt markets. It’s a significant income boost.

- Strong Covenants: Lenders in private deals can negotiate much stronger protections and terms, which helps reduce risk compared to more standardized public debt.

Strategic Private Equity Investments

In private equity, the game is all about operational control. This is a huge advantage because it allows for direct influence over how a business actually responds to rising costs. Instead of just crossing your fingers and hoping a public company has pricing power, private equity investors can get their hands dirty. They can actively work with management to protect margins, fix supply chains, and pass on costs where it makes sense.

By taking a direct, hands-on role, private equity can transform a portfolio company into a more inflation-resilient business. This is a level of influence that's simply impossible to achieve as a shareholder in a large, public corporation.

Custom-Built Inflation Protection with Structured Notes

For clients with unique situations—like those in sports and entertainment who deal with irregular income—we can get even more creative. This is where tools like structured notes come into play. These are essentially custom-built debt instruments designed to provide very specific inflation protection.

For example, we can create a note where the principal you get back at maturity is directly linked to the Consumer Price Index (CPI). If inflation averages 5% over the life of the note, the principal repayment is adjusted upward to preserve its original purchasing power. It's a precise hedge that can be designed around a specific time horizon and risk tolerance.

Of course, these advanced strategies come with more complexity, higher minimum investments, and less liquidity. They aren't for everyone. They demand a full understanding of the risks and a close partnership with an advisory team that has deep experience in these markets. But when deployed correctly, they represent one of the most effective ways for high-net-worth investors to build a truly robust defense against inflation. Getting the asset mix right is crucial, a topic we touch on in our article exploring the historical correlation between gold and the stock market.

Making the Moves: How to Put Your Inflation Strategy to Work

A great plan is one thing, but execution is everything. We’ve covered the what and the why—the specific assets and tactics to counter inflation. Now, let’s get down to the how. This is where the rubber meets the road, turning our strategy into concrete changes in your portfolio.

The single biggest mistake I see is panic. Knee-jerk reactions, driven by scary headlines, are the enemy of long-term wealth. Instead, we need a disciplined, gradual approach. This isn't about blowing up your portfolio overnight; it's about making smart, incremental shifts toward a more inflation-resilient position.

The Art of the Rebalance

Think of rebalancing as a disciplined process, not just a bit of financial housekeeping. It’s what forces you to sell what's done well (and might be getting pricey) and reinvest in assets that have more room to run. In an inflationary environment, where some assets like commodities can surge dramatically, this is absolutely critical.

A disciplined rebalancing plan looks something like this:

- You’d start by trimming positions that are most vulnerable to rising rates and inflation. Think long-duration government bonds or companies that can't pass on their rising costs.

- Then, you take those proceeds and slowly, methodically, build your positions in the inflation hedges we’ve discussed. This might mean adding to a real estate or commodity fund over several weeks or even months.

- Don't forget to look for opportunities for tax-loss harvesting. Selling a position at a loss might sting, but it creates a valuable capital loss that you can use to offset gains elsewhere in your portfolio. It’s about being strategic even when some investments are down.

The hardest part of executing a strategy isn’t picking the assets—it’s managing your own behavior. A pre-set rebalancing plan takes the emotion out of the equation, which is your best defense when the market gets choppy.

Don't Forget Taxes and Liquidity

As you start making these moves, two very practical issues come to the forefront: taxes and cash. Selling assets that have appreciated in value will trigger capital gains. To soften the blow, always look to make changes inside tax-advantaged accounts (like an IRA or 401(k)) first, where you can buy and sell without an immediate tax bill.

Liquidity is just as crucial. For business owners or families with large, irregular expenses, having cash ready for both needs and opportunities is non-negotiable. Don’t get so focused on optimizing for inflation that you leave yourself cash-poor.

A Powerful Tool: Inflation-Protected Securities

One of the most direct ways to protect a portion of your portfolio is with Treasury Inflation-Protected Securities (TIPS). They are designed to do exactly what their name says: their principal value actually increases with the Consumer Price Index (CPI).

When inflation spiked to 9.1% back in 2022, TIPS were a lifeline for investors looking to preserve capital compared to traditional bonds. For someone with an irregular income, like a professional in the entertainment industry, holding TIPS in a tax-deferred account can provide a reliable, inflation-adjusted income stream. You can see the real-time data on TIPS yields and their historical performance on the FRED website.

This isn't a "set it and forget it" situation. A solid inflation strategy needs constant attention and the flexibility to adjust as the economy shifts. Working with an advisor you trust gives you both the expertise and the discipline to navigate these headwinds, ensuring your wealth doesn't just survive—it continues to grow.

Frequently Asked Questions

When it comes to how to invest during high inflation, a lot of the same questions come up. Let's walk through some of the most common concerns we hear from investors and get you the clear, straightforward answers you need.

Should I Just Sell All My Bonds When Inflation Rises?

This is a question we hear a lot, and it's a tempting thought. But a knee-jerk reaction to sell off all your bonds is almost always a mistake. While it’s true that traditional, long-duration bonds can get hammered when rates rise to fight inflation, completely exiting fixed income can throw your entire portfolio out of balance. You'd be giving up the stability that the right kind of bonds provide.

The smarter play isn't to abandon your fixed-income allocation, but to adjust it for the current environment. We often work with clients to pivot their capital toward instruments that are built for this kind of pressure.

- Inflation-Protected Securities: Think of assets like TIPS, which are specifically designed to shield your principal from getting eaten away by inflation.

- Floating-Rate Notes: These are great because their yields actually reset higher as interest rates climb.

- Short-Duration Bonds: They're simply less sensitive to rate hikes than their longer-term cousins, making them a much more stable hold right now.

A well-diversified, actively managed bond strategy is far more powerful than just running for the exits.

The biggest risk isn't holding bonds; it's holding the wrong bonds. A strategic pivot within your fixed-income allocation is a hallmark of sophisticated inflation-era investing.

Is Holding Extra Cash A Safe Bet During Inflation?

Holding a pile of cash feels safe, but it’s one of the surest ways to lose wealth during an inflationary period. The number on your bank statement doesn't change, but what that money can actually buy is shrinking every single day. If inflation is running at 5%, your cash is effectively losing 5% of its real value, year after year.

Of course, you need a cash reserve. We typically advise clients to keep 3-6 months of expenses on hand for emergencies and to seize opportunities. But any cash beyond that isn't safe—it's idle. It should be put to work in assets with a real shot at outpacing inflation.

Navigating these decisions requires more than just general advice; it demands a clear plan built for your specific financial life. At Commons Capital, we specialize in helping high-net-worth individuals and families build resilient portfolios that can withstand these economic shifts. If you're ready to create a personalized strategy for today's inflationary environment, let's start the conversation. Contact us to learn more.