A liquidity event changes the conversation fast. One quarter you’re focused on earning, saving, and making smart decisions. The next, you’re staring at concentrated stock, tax exposure, family expectations, charitable goals, and a balance sheet that has become materially harder to manage.

That’s where the question of wealth manager vs financial planner stops being a vocabulary exercise and becomes a strategic one. High earners, founders, executives, retirees, and families with inherited assets often ask the wrong first question. They ask, “What’s the difference?” The better question is, “What problem am I trying to solve right now, and how complex is it becoming?”

If your main need is direction, accountability, and a coordinated plan for retirement, insurance, education, debt, and lifestyle decisions, a planner may be the right lead professional. If your situation now includes investment execution, tax-sensitive portfolio decisions, estate coordination, succession issues, or multi-entity complexity, a wealth manager may be the better fit. In many affluent households, the answer is not one or the other forever. It’s one first, then the other, or both at the same time.

The Crossroads of Wealth Navigating Your Next Financial Step

A familiar version of this story shows up after success. A business owner sells part of a company. A senior executive sees restricted stock vest into real wealth. An athlete signs a major contract. A family receives an inheritance and suddenly has investable assets, property decisions, tax questions, and requests from multiple relatives.

At that point, many individuals don’t lack intelligence. They lack structure. They may already have a CPA, an estate attorney, a benefits consultant, and someone handling investments. Yet the advice often sits in separate silos. One professional talks about taxes. Another talks about returns. Another talks about protection. No one is clearly responsible for the whole balance sheet.

That gap is expensive in ways that don’t always show up immediately. You can have a well-built portfolio and still have poor estate coordination. You can have a tax strategy and still have no real retirement cash flow plan. You can have a planner who understands your goals and still lack the portfolio execution needed for a more complex household.

The real risk for affluent families isn’t only bad advice. It’s fragmented advice.

The right decision depends on timing. Early wealth often needs planning discipline. Mature wealth usually requires more integrated management. Transitional wealth, such as a sale, inheritance, or contract windfall, often needs both.

What usually changes the decision

Three triggers tend to force clarity:

- Your assets become harder to manage: A brokerage account is one thing. A concentrated position, multiple entities, deferred compensation, or illiquid holdings create a different level of responsibility.

- Your goals begin to affect other people: Once children, parents, business partners, or future generations are part of the equation, personal finance becomes family governance.

- The cost of getting it wrong rises: Tax mistakes, poor distribution timing, weak estate coordination, and unmanaged risk matter more when the dollar stakes are higher.

Defining the Roles and Core Missions

A family that has done well often reaches a specific decision point. The questions stop being “Am I saving enough?” and become “Who is coordinating the moving parts, and when do I need that coordination to start?”

That is the practical divide between a financial planner and a wealth manager.

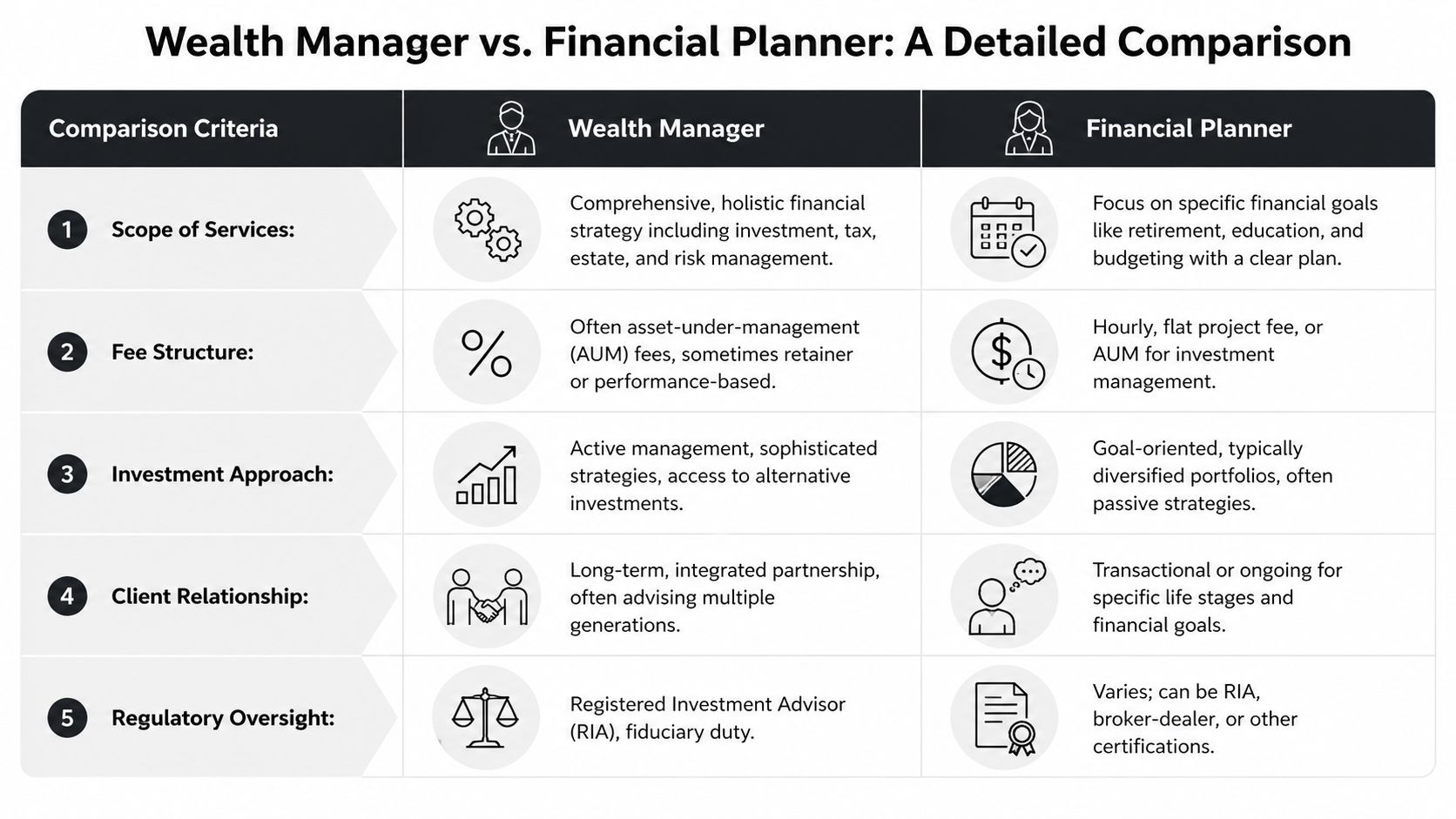

What a financial planner is built to do

A financial planner is usually engaged first, especially before complexity outruns the household’s decision-making process. The planner’s job is to bring structure to personal financial choices. That work often includes retirement projections, spending strategy, insurance analysis, education funding, stock option planning, debt decisions, and the sequence of major life goals.

The starting point is your priorities. The planner asks what you want the money to do, what trade-offs are acceptable, and which decisions need to happen now versus later.

For affluent professionals and business owners, that work matters earlier than many expect. I often see households with strong income and growing assets, but no real framework for how compensation, taxes, risk, and long-term goals fit together. A planner closes that gap by turning intentions into a usable plan.

The CFP designation is the credential clients most often associate with this role. It signals formal training in personal financial planning and fiduciary standards, but the bigger issue is fit. If your main need is clarity, prioritization, and a plan for the next stage of life, a planner is often the right first hire.

For a closer look at how this planning role can fit into a broader advisory relationship, see what a wealth planner does.

What a wealth manager is built to do

A wealth manager is usually engaged when the balance sheet becomes harder to coordinate and the cost of poor execution rises. The role centers on managing capital across multiple dimensions at once: investments, taxes, trusts and estates, business interests, liquidity planning, charitable strategy, and family governance.

The starting point is not just your goals. It is the structure of the assets themselves and the consequences attached to them.

That distinction matters. A household with concentrated stock, multiple entities, private investments, deferred compensation, or trust planning needs more than recommendations. It needs ongoing execution, coordination with attorneys and CPAs, portfolio decisions that reflect tax realities, and someone accountable for how those pieces interact over time.

Many wealth managers have investment credentials such as the CFA, and strong firms work in close coordination with tax and legal advisors. Titles matter less than operating model. A wealth manager is responsible for putting strategy into effect across a more demanding financial structure.

The right role often depends on timing

High-net-worth clients do not always need to choose one professional forever. The better question is which role fits the current stage of wealth.

If your financial life is still centered on earnings, savings, and personal goals, a planner is often the right entry point. If a liquidity event is approaching, family wealth is spreading across generations, or asset coordination has become materially more complex, wealth management becomes less optional.

Sometimes the answer is both. A planner helps define the household’s priorities and cash flow choices. A wealth manager handles investment execution, tax-sensitive structuring, estate coordination, and long-range oversight once complexity reaches a level where fragmentation becomes expensive.

That is the core mission difference. A planner helps you decide. A wealth manager helps you structure, implement, and supervise.

A Detailed Comparison of Services Fees and Philosophies

A high-income executive can often get by with planning alone for years. Then one event changes the equation. A business sale, a large vesting schedule, a new trust structure, or inherited assets can turn a straightforward plan into an ongoing coordination job.

That is the practical dividing line in a wealth manager vs financial planner decision. The question is not only who does what. The better question is when your financial life shifts from advice-driven to execution-driven.

Services differ in scope, depth, and accountability

A planner usually answers finite questions. Can retirement start at 60 instead of 65? How should stock options fit into the savings plan? Is current spending consistent with long-term goals? For many affluent households, that work has real value and can be the right first step, especially if the primary need is a structured financial planning process for high-net-worth individuals.

A wealth manager takes responsibility for what happens after those decisions are made. That includes placing assets in the right account types, managing concentrated risk, coordinating with the CPA on gains and income timing, aligning trust structures with investment policy, and adjusting the strategy as family or business circumstances change.

That difference matters because errors at the implementation stage are expensive.

Fees usually reveal the real service model

In practice, fee structure tells a prospective client how the relationship is built. An hourly or flat-fee planner is usually selling analysis, recommendations, and decision support. An AUM-based wealth manager is usually selling ongoing management, execution, monitoring, and coordination.

Industry overviews from Kitces on financial advisor fee models note that planners commonly work on hourly, project, retainer, or subscription arrangements, while investment and wealth management relationships often use AUM pricing. The trade-off is straightforward. If you need periodic planning work, paying only for advice can be efficient. If your portfolio, tax profile, and estate structure need constant attention, a one-time plan may be the cheaper option upfront and the more expensive option over time.

I tell clients to look past the label and inspect the actual workload. If the advisor is rebalancing portfolios, coordinating with outside counsel, planning around liquidity events, and managing tax-sensitive distributions, an ongoing fee can be justified. If the work stops at a projection report and a few recommendations, ongoing asset-based pricing deserves more scrutiny.

Philosophy separates advice from stewardship

Financial planning is usually organized around personal goals. The planner helps define priorities, model trade-offs, and keep choices aligned with the life the client wants to fund.

Wealth management is usually organized around stewardship. The assignment is broader. Preserve purchasing power. Reduce avoidable tax drag. Control risk that comes from concentration, illiquidity, family transfers, or poor coordination. Keep the financial structure workable as assets and obligations spread across accounts, entities, and generations.

Neither philosophy is superior in every situation. The right fit depends on timing.

If the next 12 to 24 months are mainly about choosing among competing goals, planning may be enough. If the next 12 to 24 months include a sale, inheritance, retirement income transition, trust funding, or a major shift in net worth, wealth management becomes much more relevant because the cost of fragmented execution rises quickly.

A practical way to decide

Use the fee model and service model together.

- Choose a planner first if the main need is advice, prioritization, and a clear sequence of decisions.

- Choose a wealth manager first if assets already require active oversight across taxes, investments, estate structures, or family governance.

- Use both when one professional is setting the strategy and another is executing specialized investment or balance-sheet work, provided responsibilities are clearly divided.

The strongest relationships are clear about accountability. Who is giving advice. Who is implementing it. Who is coordinating the tax and legal implications. High-net-worth families do best when those answers are explicit before complexity forces the issue.

Key Scenarios for Hiring a Financial Planner

A financial planner is often the right choice when the core need is decision clarity. The issue isn’t that your finances are unimportant. It’s that they still respond well to a structured planning process rather than a full wealth management infrastructure.

Early success with competing goals

Consider the executive whose compensation has climbed quickly. Cash flow is strong, but decisions are stacking up. Max retirement plan contributions. Review equity compensation. Build an emergency reserve. Adjust insurance. Start a college plan. Evaluate whether the current lifestyle is sustainable.

That person doesn’t necessarily need a complex investment platform first. They need a planner who can turn scattered priorities into a coherent sequence.

A strong planner is especially useful when you need to answer practical questions such as:

- Retirement timing: What savings rate supports the lifestyle you want later?

- Benefit optimization: How should you handle workplace retirement plans and stock awards?

- Risk protection: Are insurance decisions aligned with your actual family obligations?

- Spending discipline: Is your wealth growing because of income, or despite your habits?

For affluent households dealing with these foundational questions, financial planning for high-net-worth individuals is a useful starting point.

Family milestones that need structure

Planning becomes especially valuable when life changes faster than your systems.

A couple buying a larger home while preparing for private school tuition needs trade-off analysis. A family welcoming a child needs updated estate basics, beneficiary reviews, and insurance decisions. A professional moving toward retirement needs to test whether current savings behavior supports the desired withdrawal strategy.

In each of these cases, the planner’s value is less about beating a benchmark and more about reducing confusion.

A good financial planner helps you decide in the right order. That alone prevents costly mistakes.

Situations where planning is usually enough

Some households assume they need a wealth manager because they’ve crossed a certain income or asset threshold. Often they don’t, at least not yet.

A planner may be the right lead advisor if your situation looks like this:

- You need a roadmap more than portfolio complexity: The pressing issue is what to do next, not how to manage multiple asset structures.

- Your assets are still relatively straightforward: Retirement accounts, taxable savings, and employer benefits dominate the picture.

- You want project-based help: You need guidance around a major transition, but not continuous integrated management.

- Behavior is the main variable: Saving, spending, risk tolerance, and family alignment matter more than advanced execution.

Where planners are strongest

The best planners are often strongest in four areas:

- Clarifying goals when couples or family members have different assumptions.

- Building accountability around savings, spending, and deadlines.

- Stress-testing lifestyle decisions before they become permanent.

- Creating a plan you can follow, not a document that sits in a binder.

That’s why planning shouldn’t be treated as a lesser service. For many people, it’s the essential first layer. The problem begins when a family outgrows planning-only support and doesn’t recognize the shift.

Complexity Triggers for Engaging a Wealth Manager

A family sells a company, receives eight figures of cash, and assumes the hard part is over. In practice, that is often the point where risk increases. Cash has to be allocated. Taxes have to be managed. Estate documents, trusts, insurance, and investment policy all need to work together on a timeline that usually feels compressed.

A planner can help define priorities. A wealth manager becomes the right lead when the family needs ongoing execution across investments, taxes, entities, and advisors, and when a delay or a poorly sequenced decision can cost real money.

Trigger one is a liquidity event

A business sale, equity vesting cycle, inherited portfolio, or large compensation shift changes the job immediately. The question is no longer only how much to save or what goals matter most. The question becomes how to deploy capital, control concentration risk, preserve flexibility, and avoid preventable tax drag.

The practical work is detailed. It often includes transition planning for low-basis assets, short-term liquidity buckets, revised portfolio construction, trust funding, gifting strategy, and coordination with your CPA and estate attorney. Families preparing for that level of due diligence should review these questions to ask a wealth manager before choosing who will lead the process.

Trigger two is asset complexity

Asset complexity tends to build gradually, then all at once.

A household may start with retirement accounts and a brokerage account. Later, it adds employer stock, deferred compensation, private funds, multiple custodians, rental real estate, a family limited partnership, or a closely held business interest. Each new layer creates interaction effects. Selling stock changes taxes. A charitable gift affects cash flow and estate planning. A refinance or real estate sale may alter liquidity needs and investment risk at the same time.

At that stage, technical knowledge matters, but coordination matters more.

You may also need to account for family members with different levels of financial experience, which changes how assets are titled, governed, distributed, and explained. Wealth management earns its value when someone is responsible for the whole picture, not just one recommendation at a time.

Trigger three is family and legacy complexity

An individual earner can often operate well with a planner for years. A multi-generational family usually reaches a different threshold.

Legacy decisions create management problems, not just planning questions:

- Transfer structure: Should wealth pass outright, in trust, or through a staged distribution framework?

- Family governance: Who makes decisions, who gets informed, and how are responsibilities taught over time?

- Philanthropy: Should giving stay informal, or should it be coordinated with taxes, family values, and long-term grantmaking?

- Business succession: If the family owns an operating company or illiquid asset, who controls it next, and under what terms?

This distinction is reinforced by this summary of Kitces Research benchmarks, which found better five-year goal attainment for families working with wealth managers than for planner-only clients, and attributed part of that gap to tighter coordination around estate taxes and business succession.

Those numbers do not matter to every household. They matter when one decision affects beneficiaries, trustees, tax filings, business continuity, and family relationships at the same time.

Trigger four is a specialized professional profile

Some clients need wealth management earlier because their income pattern creates planning pressure faster. I see this regularly with founders, executives, physicians in private practice, athletes, and entertainment professionals.

The issue is usually not status. It is concentration, timing, and complexity. Irregular cash flow, equity compensation, short peak-earning windows, liability exposure, entity structures, and extended family obligations can overwhelm a planning-only relationship. Families with significant trust and transfer concerns may also benefit from reviewing resources on advanced wealth management for Texans while evaluating legal and fiduciary coordination.

What wealth management solves that planning alone often does not

Wealth management becomes necessary when someone must actively direct the moving parts:

- Investment implementation and oversight: Account structure, manager selection, rebalancing, cash management, and risk control.

- Tax sequencing: Deciding which assets to sell, gift, hold, or transfer, and in what order.

- Professional coordination: Keeping the CPA, estate attorney, insurance specialist, trustee, and family decision-makers aligned.

- Ongoing adaptation: Updating the strategy as markets change, laws change, and family priorities change.

The timing question is simple. If your next financial decision will affect only your budget, savings rate, or retirement timeline, a planner may still be enough. If your next decision will also affect taxes, legal structures, family governance, or multiple pools of capital, that is usually the point to bring in a wealth manager, or to build a team that includes both.

Your Decision Framework Questions to Ask

A title tells you very little. The interview tells you how your money will be handled.

A family can have a planner, an investment advisor, a CPA, and an estate attorney and still have no one clearly accountable for sequencing decisions. I see that problem often after a liquidity event, a major inheritance, or a late-career compensation change. The advisor selection process should test for fit, scope, and timing. You are not just deciding who to hire. You are deciding what type of relationship your next stage of wealth requires.

Questions to ask a financial planner

Use these when your immediate need is direction. A good planner should help you set priorities, weigh trade-offs, and make decisions with a defined time horizon.

- How do you build and update the plan? Look for a disciplined process, including data gathering, scenario testing, recommendations, and scheduled reviews.

- Which planning areas do you cover directly? Retirement, cash flow, insurance, taxes, education funding, estate basics, and equity compensation should be addressed clearly.

- What is outside your scope? This question matters. It shows whether you are hiring a planner for advice only or expecting broader implementation support than the engagement covers.

- Do you manage investments or coordinate with the person who does? You need a direct answer here, especially if portfolio decisions affect the plan.

- How are you paid? Hourly, flat fee, subscription, and asset-based models create different incentives.

- Who follows through on recommendations? Some planners produce strong analysis and leave every next step to the client.

Questions to ask a wealth manager

Use these when your next decision affects more than one domain at once. Wealth management should cover execution, coordination, and judgment across a more complicated balance sheet.

- What types of clients do you advise most often? Relevance matters. An advisor who works regularly with founders, executives, multigenerational families, or retirees with concentrated holdings will usually spot issues faster.

- How do you coordinate investment, tax, and estate decisions in practice? Strong answers describe meetings, workflows, and who is responsible for each action.

- Who handles liquidity planning and cash needs? Large portfolios still fail families if no one plans for spending, capital calls, taxes, and distributions in the right order.

- How do you work with outside CPAs and attorneys? Referrals are easy. Coordination is harder. Ask how often they communicate, what they share, and who drives follow-through.

- What happens when family members want different things? Wealth management often includes governance, boundaries, and decision rights, not just portfolio oversight.

- What does your ongoing service include each quarter and each year? You should hear specifics about reviews, reporting, plan updates, investment changes, and issue management.

For live meetings, a practical interview list helps. Review these questions to ask a wealth manager before you sit down with any firm.

If an advisor cannot explain their process clearly, expect confusion later when money is in motion.

A timing checklist for choosing the relationship

This is the part affluent families often miss. The right answer depends on what is happening now, not just on your net worth.

The decision rule I use with clients

Start with a planner when the main problem is decision clarity.

Move to wealth management when the main problem is execution across complexity.

Use both, or choose an integrated firm, when a life event changes the consequences of getting the order wrong. That is usually the moment the relationship needs to shift.

The Commons Capital Approach Integrated Financial Mastery

For high-net-worth clients, the cleanest solution is often not choosing between planning and wealth management as separate silos. It’s working with a firm that treats planning as foundational and wealth management as the execution layer built on top of it.

That model fits how affluent lives work. A family’s retirement objectives affect the portfolio. Liquidity needs affect tax decisions. Estate structures affect gifting and investment policy. Executive compensation affects risk exposure. Business ownership affects succession and legacy planning. These aren’t separate projects. They’re connected responsibilities.

Why an integrated model works better for HNW households

A fragmented advisory structure can still function when finances are simple. Once complexity rises, the gaps become obvious.

An integrated approach helps solve three recurring problems:

- Conflicting recommendations: The tax advisor, investment advisor, and attorney may all be competent, but their advice can still clash if no one is coordinating.

- Execution drift: Planning decisions lose value when no one owns follow-through.

- Timing mistakes: The order of transactions matters when wealth, taxes, and estate issues intersect.

This is especially relevant for clients with $500,000 or more in investable assets, business owners, family offices, retirees, and professionals in sports and entertainment. Those clients don’t just need a plan document or a model portfolio. They need a relationship that can absorb complexity without losing sight of real family goals.

What sophisticated clients should expect

An effective private wealth relationship should give you more than access to investments. It should provide:

- Strategic planning discipline: Your goals, obligations, and values stay at the center.

- Portfolio oversight: Someone is responsible for implementation and ongoing review.

- Coordination across specialists: Tax, estate, business, and risk issues are addressed together.

- Adaptability: The strategy changes as your family, assets, and responsibilities change.

That’s the practical answer to the wealth manager vs financial planner question for affluent families. The most durable solution often combines both mindsets. Planning tells you what matters. Wealth management helps ensure your capital is aligned around it.

If your financial life has become more successful and more complicated at the same time, it may be time for a more integrated approach. Commons Capital works with high-net-worth individuals, families, business owners, and sports and entertainment clients who need both strategic planning and advanced wealth management under one roof.