You’ve likely already modeled market volatility, tax drag, sequence-of-returns risk, and longevity. Then Medicare enters the conversation and gets treated like an administrative detail.

It isn’t.

For affluent retirees, medicare supplement insurance options are less about basic insurance shopping and more about deciding how much healthcare liability you want to transfer off your balance sheet. Original Medicare gives broad foundational coverage, but it doesn’t cap annual out-of-pocket spending. That single design feature can disrupt even a carefully engineered retirement cash flow plan.

A useful way to frame the decision is simple: do you want healthcare costs to behave more like a controlled premium expense, or more like a variable claim against your portfolio? If you want a broader context for how medical coverage decisions affect personal finances, this detailed health insurance guide is a practical companion resource.

Retirees who are also thinking about eldercare risk should consider healthcare coverage in parallel with asset protection planning, especially if nursing care is part of the family discussion. That issue intersects with this Commons Capital perspective on https://www.commonsllc.com/insights/protecting-assets-from-nursing-home-costs.

Navigating Healthcare Costs in Retirement

A common scenario looks like this. A couple retires with substantial taxable assets, IRA balances, and no debt. They’ve built income ladders, planned Roth conversions, and set a portfolio withdrawal policy. Then one spouse asks a deceptively simple question: what happens if one of us has a bad health year?

That question matters because Medicare doesn’t work like a corporate executive health plan. It leaves deductibles, coinsurance, and other gaps in place. For many households, those aren’t catastrophic every year. The problem is that you can’t know in advance when they won’t be manageable.

Why affluent retirees still buy supplemental coverage

Medigap exists to turn an open-ended liability into a more predictable one. In 2023, Medigap covered 12.2 million beneficiaries, representing 43% of those in traditional Medicare, and 87% of traditional Medicare enrollees had some form of supplemental coverage, which matters because Original Medicare lacks an annual spending cap and can leave retirees exposed to potentially catastrophic expenses, according to KFF’s snapshot of Medicare supplemental coverage.

That figure tells you something important beyond market size. Well-informed households don’t view supplemental coverage as optional convenience. They use it to remove uncertainty from a core retirement expense category.

Practical rule: If your retirement plan depends on stable annual withdrawals, uncontrolled healthcare exposure is an asset allocation problem, not just an insurance problem.

The primary risk isn’t average spending

High-net-worth clients sometimes assume they can self-insure. In pure net worth terms, many can. But self-insuring healthcare isn’t only about whether you can pay a bill. It’s about whether paying variable bills creates the wrong kind of friction in the broader plan.

That friction shows up in several ways:

- Portfolio timing risk: A large medical year can force withdrawals when markets are down.

- Tax planning interference: Unexpected expenses can disrupt Roth conversion timing, capital gain realization, or charitable funding plans.

- Spousal asymmetry: One spouse’s health profile can alter household cash flow long before it affects the estate.

- Behavioral drag: Clients often become more conservative with travel, gifting, or discretionary spending when healthcare costs feel unknowable.

A Medigap policy won’t solve every healthcare planning issue. It also doesn’t cover long-term custodial care. But for the narrower problem it’s designed to address, it can make retirement cash flow more durable.

The Standardized World of Medigap Plans

A retiree with substantial assets can still make an expensive Medicare mistake here. If two insurers quote different premiums for Plan G, many buyers assume the richer policy must cover more. In Medigap, that assumption is usually wrong.

What standardization means

Medicare standardized Medigap plans in 1990, creating 10 options: A, B, C, D, F, G, K, L, M, and N, as shown in Medicare’s official Medigap plan benefit comparison.

For financial planning purposes, that standardization changes the order of analysis. A Plan G from one insurer carries the same core medical benefits as a Plan G from another insurer. Once you choose the letter, the benefit design is largely fixed.

That shifts the primary underwriting question from product design to counterparty selection. Carriers compete on premium level, pricing discipline over time, underwriting rules where permitted, administrative quality, and claims reliability. For a high-net-worth household, that makes Medigap less like shopping for a custom insurance contract and more like selecting the lowest-cost issuer for a standardized liability hedge.

Why the letter matters first

This structure is unusual in insurance. In many markets, buyers compare contract terms first and insurer quality second. Medigap reverses that sequence.

Choose the risk-transfer structure first. Then compare insurers inside that structure.

That distinction matters because it keeps you from optimizing the wrong variable. Spending hours comparing carrier brochures before deciding whether you want broader first-dollar protection or more retained exposure produces a lot of activity and little clarity. The financially relevant choice is how much volatility you want to remove from future healthcare cash flow. The carrier decision comes after that.

Why Plans C and F matter less for new buyers

The modern Medigap market changed on January 1, 2020, when MACRA barred Plans C and F for people newly eligible for Medicare. As noted earlier, that change pushed many new enrollees toward Plan G and reduced the practical relevance of Plan F for current comparisons.

For new retirees, this narrows the decision set. Legacy discussions around Plan F still matter for grandfathered policyholders evaluating whether to keep existing coverage, but they are often a distraction for households making a fresh election today.

A practical way to read the Medigap alphabet

You do not need to analyze every letter equally. A better framework is to sort plans by the role they play in the balance sheet.

- Broader coverage plans: These transfer more of Original Medicare’s residual cost-sharing to the insurer.

- Cost-sharing plans: These preserve lower premiums by keeping some routine exposure with the retiree.

- Legacy plans: These remain relevant for certain previously eligible beneficiaries but are closed to many new entrants.

- High-deductible versions: These fit households willing to retain predictable first-layer costs in exchange for lower fixed premiums.

The planning value is straightforward. Medigap plan selection is not mainly a health insurance exercise. It is a decision about how much medical cost volatility should remain inside the household balance sheet versus being exchanged for a known premium. For affluent retirees, that affects withdrawal consistency, reserve sizing, and the amount of liquid capital that must stay available for unplanned healthcare claims.

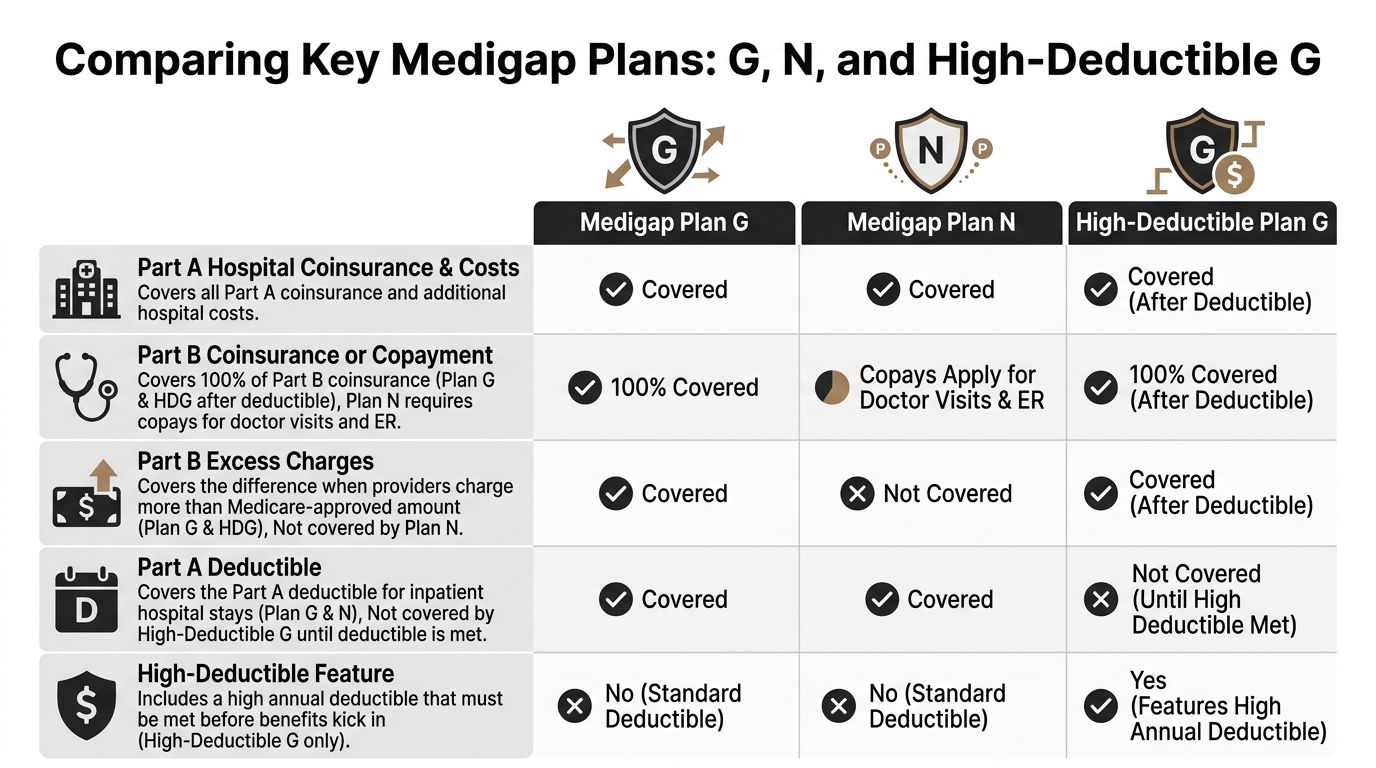

Comparing Plan G, Plan N, and High-Deductible G

A retiree with a large portfolio can still make a poor insurance decision. The mistake usually is not choosing the wrong letter. It is retaining the wrong layer of healthcare risk on the household balance sheet.

For new Medicare enrollees, the three plans that usually merit serious analysis are Plan G, Plan N, and High-Deductible Plan G. They insure the same general problem in three different ways: one converts more spending into a fixed premium, one leaves modest point-of-service exposure in place, and one keeps a larger first-loss layer with the retiree while protecting against bigger claims.

Here is the practical comparison.

Plan G as the modern benchmark

Plan G has become the benchmark for many new enrollees because it leaves only a narrow, defined gap. It covers Medicare-approved costs other than the Part B deductible, which is $283 in 2026, according to Commons’ Medicare supplement plan comparison.

From a financial planning standpoint, that design is straightforward. It converts an uncertain stream of smaller claims into a largely predictable premium structure and leaves only limited annual exposure. For a client building a retirement cash flow plan, that can reduce the need for excess liquidity earmarked for routine medical variance.

Plan G also reduces operational friction. Households that value physician choice, travel flexibility, and low administrative hassle often prefer paying more upfront to avoid repeated billing review later.

Plan N as a measured retention of routine risk

Plan N usually fits retirees who are willing to keep some recurring healthcare costs inside the plan rather than transferring nearly all of them to the insurer. That choice can make sense, but only if the premium savings exceed the extra cost-sharing and the additional monitoring burden.

Two exposures deserve close attention:

- Office and emergency room copayments: routine care is not as cleanly insulated from out-of-pocket costs.

- Part B excess charges: providers who bill above Medicare-approved amounts can create additional liability.

That second point matters more for affluent retirees than many comparison charts suggest. A household may value access to specific specialists or practice groups and may care less about modest copays than about billing unpredictability. If your physician network is stable and you understand how those providers bill, Plan N can be efficient. If you want healthcare spending to behave like a controlled household expense, Plan N introduces more variables.

Plan N is a lower-premium structure with selective retained risk and more administrative attention required.

High-Deductible Plan G for households that self-insure by design

High-Deductible Plan G deserves a more serious look in high-net-worth planning conversations. It requires the enrollee to absorb a substantial deductible before full plan benefits apply, as noted earlier.

That design can be rational for a household with ample liquidity and a clear philosophy around insuring only larger losses. Instead of paying materially higher fixed premiums to eliminate relatively manageable first-dollar costs, the retiree preserves capital and accepts a defined early-year exposure.

Over a long retirement, this can become a capital allocation decision as much as an insurance decision. Lower premiums may preserve funds for tax-efficient withdrawals, gifting strategies, or keeping more assets invested rather than redirecting those dollars toward routine risk transfer. The trade-off is clear. You must be comfortable funding smaller and mid-sized claims without irritation or disruption.

For clients who already carry high deductibles on property coverage, umbrella liability for tail risk, and strong cash reserves, High-Deductible Plan G often fits an established risk framework.

How to choose between the three

The right choice depends on the level of medical spending volatility you want to keep, your tolerance for billing oversight, and the opportunity cost of higher premiums.

Choose Plan G if:

- You want tight budget control: annual uncertainty stays limited.

- You place a premium on convenience: less claims friction has value.

- You expect regular care or specialist use: broader coverage reduces repeated small decisions.

Choose Plan N if:

- You accept some ongoing cost-sharing: lower premiums matter to you.

- You are comfortable monitoring provider billing: excess-charge exposure is manageable only if you pay attention.

- Your care pattern is relatively predictable: surprise costs are less likely to undermine the savings.

Choose High-Deductible G if:

- You have the liquidity to absorb early-year claims: the deductible will not affect spending plans.

- You evaluate insurance through a balance-sheet lens: preserving premium dollars for other uses is part of the objective.

- You insure against larger downside, not routine expenses: the plan is built for that approach.

A more advanced perspective

These three plans map to three different liability-management strategies.

- Plan G shifts more residual healthcare costs to the insurer and supports spending stability.

- Plan N shares the liability between fixed premium and recurring out-of-pocket expenses.

- High-Deductible Plan G keeps the first-loss layer with the retiree and insures the more disruptive tail risk.

For affluent retirees, that framework is more useful than asking which plan is "best." The core question is how each option fits with cash reserves, taxable account drawdowns, portfolio risk tolerance, and the household’s broader preference for transferring or retaining manageable liabilities.

Your Medigap Open Enrollment Window

The best Medigap choice on paper can become irrelevant if you get the timing wrong.

Why timing carries more weight than plan selection

Medigap has a one-time six-month open enrollment period that begins when you are 65 or older and enrolled in Medicare Part B. During that window, insurers must sell you coverage without using medical underwriting. That practical protection is what makes the window so valuable.

If you apply later, insurers may review your health history. Depending on your state rules and situation, that can mean higher costs, fewer available choices, or denial.

For affluent retirees, this issue often appears in a specific pattern. They continue working past 65, keep employer coverage, and delay Part B. That can be a perfectly rational move. The mistake is assuming the Medigap clock started at 65 regardless of Part B timing. It doesn’t. The trigger is Part B enrollment.

The planning mistake I see most often

Many financially organized people think they can revisit supplemental coverage later when they “need it more.” That is backwards.

Medigap is generally easiest to secure when your need feels less urgent and your health may still be viewed more favorably. Waiting until utilization rises can reduce your options at the exact moment you want more protection.

The enrollment window is a strategic option. Once it passes, you may not be able to recreate it on demand.

What to do before the window opens

A disciplined process helps:

- Confirm your Part B start date: This controls the Medigap timetable.

- Decide your risk-transfer preference early: Choose between richer coverage, moderate cost-sharing, or a high-deductible structure before enrollment pressure arrives.

- Line up carrier comparisons in advance: Since benefits are standardized, rate and pricing structure review should happen before the clock starts.

- Coordinate with employment coverage decisions: If you’re still working, make sure your employer plan, Medicare timing, and Medigap strategy all fit together.

This is one of the few Medicare decisions where timing can matter more than optimization around the margins. Missing the window can turn a clean financial choice into a constrained one.

Decoding Medigap Premiums and Carrier Selection

Standardized benefits simplify one part of the decision. They don’t simplify pricing.

Same plan letter, different premium path

One carrier’s Plan G can cost meaningfully more than another’s Plan G even though the medical benefits are the same. That’s why shopping Medigap like a consumer product often leads to poor decisions. You need to shop it like a long-term liability contract.

The first premium you see is not the whole story. What matters is the pricing method behind it and how that method may affect your future costs.

The three pricing models

Most Medigap premium structures fall into three broad categories.

Community-rated

In a community-rated design, the insurer doesn’t base the premium on your current age. The appeal is stability. The drawback is that the starting premium may not look cheapest.

This model often suits retirees who care more about long-run predictability than about winning the first-year quote comparison.

Issue-age-rated

Issue-age pricing ties the premium to the age when you buy the policy. Buying younger can lock in a lower starting basis than buying later.

This structure can reward decisive enrollment. It may appeal to clients who expect to keep the policy for a long period and want the economics of early action to matter.

Attained-age-rated

Attained-age pricing rises as you get older. It can look attractive at the beginning, which is why many retirees focus on it first.

But a low entry premium can be misleading if the long-run cost path is steeper. That doesn’t make attained-age pricing bad. It means you should evaluate it with a longer horizon than the quote screen invites.

A Medigap premium is not just a monthly expense. It is a future cash flow stream with its own inflation behavior.

What discerning buyers evaluate beyond price

High-net-worth retirees should look at Medigap premiums through three lenses.

- Cash flow design: Do you want a higher fixed premium and lower claims variability, or the reverse?

- Tax interaction: As noted in Mutual of Omaha’s discussion of plan selection, high-net-worth individuals can coordinate Medigap premiums and medical expenses with IRC Section 213, so the trade-off between higher premiums and retaining more out-of-pocket spending can become a meaningful planning variable in how to choose the right Medicare supplement insurance plan.

- Underwriting risk: If you’re applying outside a protected enrollment period, health status can matter. That raises the value of acting while guaranteed access is still available.

How to compare carriers without overcomplicating it

A practical carrier review usually includes:

- Current premium level: Useful, but not decisive by itself.

- Pricing method: This affects the slope of future costs.

- Household fit: Some households prefer richer coverage for one spouse and greater retained risk for the other, depending on utilization and cash reserves.

- Administrative competence: Billing accuracy, service responsiveness, and policy maintenance matter more than marketing.

For readers who want a tool-based way to compare letters before narrowing carriers, Commons Capital offers a Medicare Supplement Plan Comparison tool for 2026 that compares Medigap plans including G, N, M, F, and others. Used properly, a tool like that helps isolate plan design before you evaluate insurer pricing.

Medigap vs Medicare Advantage for HNW Retirees

For many retirees, the first question isn’t which Medigap letter to choose. It’s whether Medigap is the right path at all.

The alternative is Medicare Advantage. The strategic difference is clear. Medigap supplements Original Medicare. Medicare Advantage replaces the Original Medicare delivery model with a private plan structure.

Why wealthy retirees often care about freedom more than bundled extras

Medicare Advantage can look attractive because it often packages multiple benefits into one plan. For some retirees, that simplicity works well.

But high-net-worth households usually weigh a different set of priorities:

- Provider flexibility: Many want broad access without worrying about plan networks.

- Multi-state living: Seasonal residence patterns can make network constraints more disruptive.

- Travel patterns: Frequent domestic travel can increase the value of a more portable coverage structure.

- Cost predictability: Some clients would rather pay more in fixed premiums than sort through changing utilization rules.

That’s why the Medigap route often aligns with retirees who view healthcare as a planning variable to be controlled, not merely a benefit to be purchased at the lowest visible cost.

The trade-off in plain terms

A simple comparison helps.

The better answer depends on what kind of retiree you are.

If you like integrated packages, don’t travel much, and are comfortable adapting to network rules, Medicare Advantage may be sufficient. If you want freedom of movement and cleaner liability planning, Medigap often fits better.

For retirees comparing these choices within a broader wealth framework, this Commons Capital resource on choosing a https://www.commonsllc.com/insights/retirement-financial-advisor is useful because the Medicare decision is rarely isolated from the rest of retirement planning.

Integrating Medigap into Your Financial Plan

A retired couple with an $8 million balance sheet can absorb a deductible. What often causes more damage is irregular cash flow, forced portfolio sales in a down market, and higher taxable withdrawals triggered by medical bills that were never built into the plan. Medigap belongs in the same conversation as withdrawal strategy, reserve design, and estate objectives because it changes how healthcare liabilities show up on the household balance sheet.

Treat premiums as a liability management decision

Medigap converts part of an uncertain expense stream into a scheduled premium. For affluent retirees, that is less about minimizing medical spending and more about controlling variance.

In retirement modeling, healthcare costs usually fit best in one of two structures:

- Fixed obligations funded through recurring income

- Retained risk backed by designated liquid assets

Problems arise when neither structure is explicit. A client then funds care costs from whatever account is convenient at the time, which can lead to inefficient withdrawals, avoidable tax friction, and portfolio disruption during weak markets.

Fit Medigap to the rest of the balance sheet

The planning question is straightforward. Which Medigap design produces the cleanest interaction with your income sources, taxable accounts, and legacy plan?

Horizon’s overview of Medicare supplement plans notes that higher-income households should evaluate Medigap in the context of cash flow projections and other uncovered care exposures, particularly long-term care. That distinction matters. Medigap can reduce volatility in routine medical spending, but it does not address custodial care risk, so the remaining liability still needs its own funding plan.

A sound integration usually includes several separate decisions:

- Cash flow design: Classify Medigap premiums as a recurring retirement expense, not an incidental bill.

- Reserve policy: If you choose High-Deductible Plan G, hold enough liquid capital to absorb early-year out-of-pocket costs without disturbing the investment allocation.

- Spousal planning: Two spouses do not always need the same trade-off between premium efficiency and claim predictability.

- Long-term care funding: Keep Medigap analysis separate from custodial care planning so one decision does not create false confidence about the other.

- Legacy strategy: Model healthcare spending, gifting, and trust distributions together because each affects the amount and timing of wealth transfer.

The objective is not solely lower claims volatility. The objective is to keep healthcare costs from forcing changes elsewhere in the plan.

Use Medigap to support broader retirement strategy

For some households, Plan G supports a higher premium with fewer billing surprises, which can make annual withdrawal planning easier. For others, High-Deductible G is more efficient because they prefer to self-fund a manageable first layer of expense and keep more capital compounding. Plan N can fit clients who accept some utilization-based cost sharing in exchange for lower premiums, provided they understand how that choice affects budgeting discipline.

The right selection depends on how you want the rest of the financial system to operate. A retiree funding core spending with pensions, Social Security, and other guaranteed retirement income strategies may value stable healthcare costs because they fit more cleanly into an income floor. A retiree drawing opportunistically from taxable and tax-deferred accounts may accept more retained risk if that approach improves premium efficiency over time.

For a broader framework, this resource on detailed financial planning for retirees is useful because Medicare decisions rarely stand alone. They interact with tax sequencing, liquidity management, and the degree of flexibility you want to preserve for family transfers or future care needs.

Commons Capital works with high-net-worth individuals, families, and institutions facing complex planning decisions, including how healthcare coverage choices affect retirement cash flow, tax strategy, and long-term asset protection. If you want help evaluating how Medicare supplement insurance options fit into your broader financial plan, you can learn more at Commons Capital.