A personal financial plan is often called a "roadmap for your money." It’s a good starting point, showing you where you are and outlining the steps to get where you want to go.

But for high-net-worth individuals and families, a standard map just won't cut it. When you're navigating complex terrain with goals that span generations, a simple road atlas isn't just insufficient—it's a genuine risk to your long-term wealth and legacy. A comprehensive personal financial plan is the cornerstone of preserving and growing substantial assets.

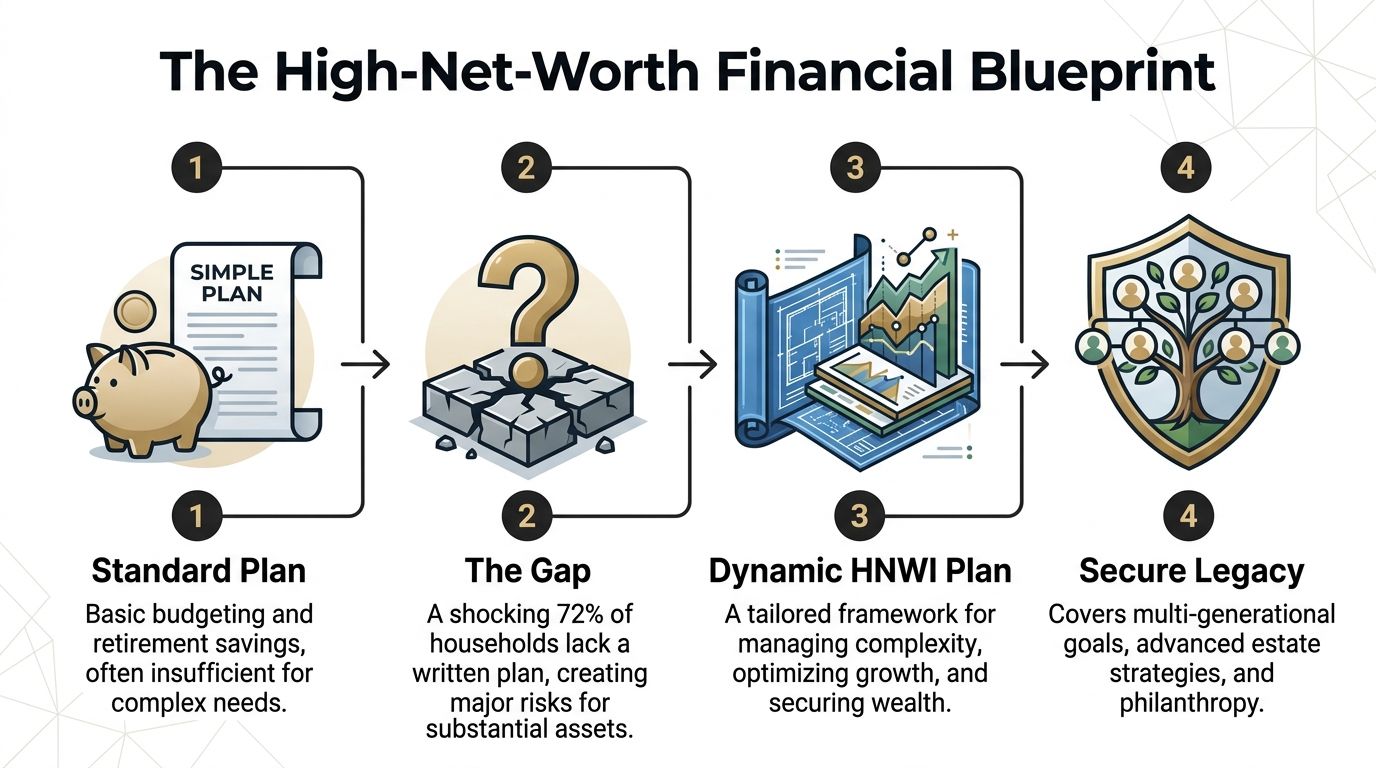

Why a Standard Financial Plan Falls Short

Most financial planning is built around the basics: budgeting, saving for retirement, and paying off a mortgage. Those are crucial habits, but they only scratch the surface of the realities faced by people with substantial assets, complex income streams, and goals that span generations.

It’s surprising how many people operate without any plan at all. Research from Savology.com found that a staggering 72% of American households don’t have a written financial plan. That means fewer than one in three have a documented strategy guiding their financial lives.

The Critical Gap Between a Basic Plan and a True Blueprint

When your financial world includes private equity stakes, concentrated stock positions from an IPO, or the sale of a business on the horizon, a generic plan crumbles. It simply can't account for the unique tax burdens, risk exposures, and succession questions that come with significant wealth.

Following a one-size-fits-all template can leave you exposed to market swings, create tax inefficiencies that quietly erode your net worth, and lead to missed opportunities for strategic growth.

This is where a personalized financial blueprint becomes non-negotiable. It’s a framework that moves beyond simple savings goals to build a durable, sophisticated structure for managing complexity and protecting what you’ve worked so hard to build.

The journey from a basic plan to a multi-generational legacy strategy looks something like this:

This evolution is about integrating advanced strategies for growth, tax optimization, and legacy, turning a simple plan into a powerful tool.

To illustrate the difference, here’s a look at how the core components of a plan are approached differently for high-net-worth clients.

Core Components of a High-Net-Worth Financial Plan

PillarFocus for High-Net-Worth IndividualsConventional ApproachGoal SettingMulti-generational wealth transfer, legacy projects, philanthropic ambitions.Retirement savings, college funds, mortgage payoff.Tax PlanningProactive strategies for capital gains, estate taxes, and income sheltering.Maximizing annual retirement contributions and standard deductions.InvestmentDiversification across public and private markets, managing concentrated positions.Mutual funds and ETFs in a 401(k) or brokerage account.Estate PlanningComplex trust structures, business succession, and charitable giving vehicles.A basic will and power of attorney.Risk ManagementAsset protection, personal liability, and specialty insurance coverage.Standard life and disability insurance.

This table only scratches the surface, but it highlights the shift in mindset and complexity required.

Building Your Comprehensive Financial Blueprint

A truly effective financial plan acts more like a constitution for your wealth. It's a living document that ensures every financial decision—from a major investment to a philanthropic gift—is aligned with your most important, long-term objectives.

This guide is designed to give you that advanced framework. We’re moving past the conventional advice to show you how to build a plan that confronts the specific challenges and unlocks the unique opportunities you face.

This guide isn't about basic budgeting. We're here to show you how to construct a dynamic personal financial plan that serves as a blueprint for managing complexity, optimizing growth, and securing your wealth for generations to come.

These strategies are fundamental to sophisticated financial stewardship. To see how they fit into a broader service model, you can learn more about what private wealth management entails.

Throughout this guide, we'll dive deep into the essential pillars of an effective high-net-worth plan, including:

- Setting goals that span multiple generations

- Designing advanced estate and philanthropic strategies

- Implementing sophisticated tax and risk management

- Establishing governance to manage family dynamics

This structure is what ensures your wealth not only grows but, more importantly, serves its ultimate purpose.

Establishing Your Financial Foundation

A real personal financial plan doesn’t kick off with hot stock tips or clever tax loopholes. It starts with getting an uncomfortably honest look at your complete financial picture. For families with significant wealth, this is so much more than a simple spreadsheet of what you own and what you owe.

We have to build a 360-degree view of your financial world, one that truly gets the complexity of your situation. This is all about building your personal balance sheet and mapping your cash flow with total precision. It’s time to move past rough estimates and get to the real numbers.

Analyzing Your Complete Balance Sheet

Think of your balance sheet as a snapshot of your net worth at this very moment—your assets minus your liabilities. The thing is, for most successful people I work with, the "assets" part is rarely straightforward. A bank statement or a Schwab portfolio is just the beginning.

Getting an accurate number requires a much deeper dive, especially in a few key areas:

- Valuing Illiquid Assets: This is almost always the trickiest part. How do you value your stake in a private company, your venture capital fund, or the family business? There's no daily stock ticker for these. It takes specialized analysis to land on a fair market value.

- Real Estate Portfolios: Your family home is just one piece of the puzzle. We need to look at every property—investment rentals, vacation homes, commercial buildings—and understand its unique debt, cash flow, and growth potential.

- Complex Compensation: For executives, founders, and entertainers, pay isn't just a salary. We have to account for deferred comp plans, restricted stock units (RSUs), and various stock options, all of which have a real value that must be integrated.

The most common mistake I see is people glossing over or completely ignoring these complex assets. An accurate balance sheet is the foundation of everything. If it's wrong, every decision you make from that point on is built on a faulty premise.

Deconstructing Your Cash Flow

With a clear balance sheet in hand, we can turn to cash flow—the money flowing in and out of your life. Again, this is much more than just income minus expenses. We need to analyze the sources of your cash and the uses of it to spot both opportunities and risks.

For instance, a business owner might see huge, but irregular, cash distributions from their company. That requires a different strategy than that for a pro athlete, who has an incredibly high but very short earning window. Their plan has to be laser-focused on converting that short-term income into lifelong wealth.

When you're laying this groundwork, picking the right account structure is critical. Learning the key differences between an advisory vs brokerage account is a good first step to see which aligns with your long-term goals.

Translating Goals into Financial Targets

This is where the plan stops being a set of numbers and starts becoming truly yours. Abstract goals like "leave a legacy" or "give back" don't mean much until we attach real dollars to them.

We start asking very specific questions:

- Philanthropic Ambitions: What does giving back look like for you, year after year? Do you want to set up a foundation or a donor-advised fund? A goal of donating $100,000 annually is a world away from endowing a $5 million charitable trust.

- Multi-Generational Wealth Transfer: What does "taking care of your family" actually involve? Are we funding education for grandkids? Helping with down payments on their first homes? Planning a business transfer? Putting numbers to these goals tells us exactly how much capital you'll need.

- Lifestyle and Liquidity: What kind of cash do you need on hand for your life, now and in retirement? This covers everything from major purchases and travel to simply maintaining your standard of living without worry.

By getting this foundation right—documenting the balance sheet, mapping the cash flow, and tying it all back to your core values—we build the solid ground upon which every other strategy will stand.

Building Your Investment and Growth Engine

With a clear picture of your financial foundation, it’s time to build the engine that will actually grow your wealth. This is where we shift from analysis to action, creating a plan that puts your capital to work for you. It's about designing a portfolio built for both resilience and opportunity.

The absolute cornerstone here is the Investment Policy Statement (IPS). This isn't just another piece of paperwork; it’s your personal constitution for every single investment decision. It’s what keeps emotion and impulse out of the picture, making sure every move you make lines up with the life goals we’ve already defined. It's a critical step that, frankly, too many investors skip.

Your Investment Policy Statement is your North Star. It sets out your objectives, constraints, and guidelines, giving you a disciplined framework to navigate your portfolio through any market cycle.

This document forces you to get honest about the tough questions before a single dollar is invested. What’s your real appetite for risk? What’s your timeline for needing the money? And what returns do you actually need to hit your targets?

Defining Your Investment Philosophy

Before we even think about specific investments, we need to get your core philosophy down on paper. This means having a frank discussion about what you want your money to do and how much volatility you can stomach. For many high-net-worth families, the goal isn’t just about chasing aggressive growth; it's about striking a careful balance that also preserves the capital you've worked so hard to build.

We'll pin down several key parameters:

- Return Objectives: Are you looking for returns that simply maintain your current lifestyle, or do you need more significant growth for something big, like funding a foundation or a business succession?

- Risk Tolerance: This is more than a simple questionnaire. We need to talk about what you would really do if the market suddenly dropped 20%. Would you see a buying opportunity, or would the panic set in?

- Time Horizon: Different goals have different timelines. Money you need for a child's college tuition in five years has to be managed completely differently than funds meant for multi-generational wealth transfer.

- Liquidity Needs: How much cash needs to be readily available for emergencies, business opportunities, or just life? This directly impacts how much we can allocate to less liquid, potentially higher-return assets.

For a much deeper dive on this, our guide on creating an Investment Policy Statement walks through all the specifics.

Structuring a Diversified Portfolio

Using the IPS as our blueprint, we can start structuring your asset allocation. For high-net-worth investors, real diversification goes way beyond the classic mix of stocks and bonds. We aim to build a portfolio that can hold its own in a variety of economic climates.

This often means bringing in asset classes that most retail investors simply can't access:

- Private Markets: Allocating to private equity and venture capital can unlock higher growth potential, but it comes with longer lock-up periods and, of course, higher risk.

- Alternative Investments: This is a broad category that includes things like hedge funds, which can offer returns that don't move in lockstep with the public markets, and private credit, which provides income streams outside of traditional bonds.

- Strategic Real Estate: Looking beyond your personal home, direct ownership of commercial or residential properties—or investing in real estate funds—can provide both steady income and a hedge against inflation.

- Digital Assets: For investors with a higher risk tolerance, a small, strategic allocation to cryptocurrencies is becoming more common. For anyone exploring this space, using a dedicated Crypto Portfolio Tracker is essential for keeping a handle on these volatile assets.

Managing Concentrated Stock Positions

A common "problem" for executives, early tech employees, and business founders is having a massive chunk of their wealth tied up in a single company's stock. While this is often how significant wealth is created, having more than 10-15% of your net worth in one stock is a huge, uncompensated risk. One bad earnings report or a shift in the industry could be devastating.

Protecting the wealth you've already built while managing this concentration is a crucial part of any robust financial plan. We don't want to kill the potential for more upside, but we have to put safeguards in place.

There are a few proven techniques we use to manage this risk:

- A Disciplined Selling Plan (10b5-1): For corporate insiders, this is a pre-scheduled, automated plan to sell company stock over time. It takes the emotion and guesswork out of the equation and serves as a defense against any accusations of insider trading.

- Hedging with Options: Using a strategy like a "costless collar" can put a floor under your stock's value while still letting you participate in some of the upside. Think of it as an insurance policy against a major crash.

- Exchange Funds: These specialized funds allow you to swap your concentrated stock position for a diversified portfolio of other stocks, all while deferring the capital gains tax you would have triggered from an outright sale.

By methodically building this growth engine—grounded in a strong IPS and diversified across public, private, and alternative markets—you turn your financial foundation into a powerful vehicle for achieving your most important long-term goals.

Integrating Advanced Tax and Estate Strategies

You’ve worked hard to build your wealth. The real challenge now is keeping it.

For many successful families, the two greatest threats to their legacy aren't market crashes, but taxes and a poorly planned estate transfer. This is where a good financial plan shifts from simply growing your assets to truly protecting them for generations.

Let's be clear: hunting for deductions on your annual return isn't a strategy. It's a basic, reactive task. Real tax planning is a proactive, year-round discipline that looks decades into the future, structuring your assets to ensure your wealth is working for your goals, not just the IRS.

Maximizing Tax Efficiency Beyond the Basics

Advanced tax planning is all about making smart decisions before a taxable event happens. For anyone managing substantial assets, these techniques aren't just nice to have; they are fundamental.

A couple of the most powerful strategies we see work time and time again include:

- Tax-Loss Harvesting: This is more than a year-end scramble to sell a few losers. It’s an ongoing, systematic process. By realizing losses, you can offset capital gains and even up to $3,000 of your ordinary income each year, which can dramatically lower your tax bill without knocking your long-term investment strategy off course.

- Strategic Asset Location: This is a surprisingly potent, yet often overlooked, strategy. The concept is simple: put your most tax-inefficient assets (like corporate bonds or high-turnover mutual funds) inside tax-advantaged accounts like IRAs. Your more tax-friendly investments (like index funds you plan to hold forever) can sit in your taxable accounts, where they'll benefit from lower long-term capital gains rates.

When applied thoughtfully, these methods can add a significant layer of after-tax return to your portfolio over the long run. We explore more of these concepts in our guide on high-net-worth tax strategies.

Designing Your Estate Plan for a Smooth Transition

An estate plan is so much more than a will. Think of it as a complete playbook that directs how your assets are managed if you can't, and how they’re distributed when you're gone. A well-built plan ensures your wishes are honored, slashes potential estate taxes, and shields your assets from lawsuits or other challenges.

Without a clear plan, your wealth could be tied up in probate court for years, shrinking due to legal fees and taxes, and ultimately distributed in a way you never intended. It's one of the most critical backstops in any personal financial plan.

A few of the core tools we use in estate planning are:

- Wills and Powers of Attorney: The will is the foundation, naming an executor and spelling out how assets should be divided. Just as important are the durable power of attorney for finances and a healthcare power of attorney, which appoint trusted people to make critical decisions if you become incapacitated.

- Trusts: These legal structures are the workhorses of modern estate planning. A revocable living trust is fantastic for avoiding the costly and public process of probate. Irrevocable trusts, on the other hand, can be used to move assets outside of your taxable estate entirely, offering incredible asset protection. We can even use specialized versions like Charitable Remainder Trusts (CRTs) to create an income stream for you, generate a current tax deduction, and leave a meaningful gift to charity.

Case Study: A Family Business Sale

Imagine a family gearing up to sell their manufacturing business, which has a current value of $30 million. If they just sold it outright, they’d face a staggering capital gains tax bill. The remaining proceeds would then sit in their estate, where they could be hit with a 40% federal estate tax.

Instead, we worked with them on an integrated plan:

- Pre-Sale Gifting: Years before the sale, they began gifting shares of the company into an irrevocable trust for their children. This strategy moved all the future growth of those shares out of their taxable estate.

- Charitable Remainder Trust: They also moved a portion of their shares into a CRT prior to the sale. When the business was sold, the trust itself paid no immediate capital gains tax. The parents got a major charitable deduction and will receive an income stream for the rest of their lives.

- Life Insurance: Using some of the gifted funds, they established another irrevocable trust to purchase a life insurance policy. When they pass away, the death benefit will be paid out completely free of income and estate taxes, giving their heirs the immediate cash needed to pay any remaining estate taxes without having to liquidate other assets.

This cohesive approach didn't just save millions in taxes. It shielded the family's core wealth and ensured their legacy would be transferred exactly how they wanted. It’s a perfect example of how tax and estate planning aren't separate checklist items—they are deeply intertwined parts of a truly comprehensive financial plan.

Fortifying Your Wealth: Risk, Legacy, and Family Governance

A truly comprehensive financial plan does more than just grow your wealth—it has to protect it and give it a clear purpose. Once we've dialed in your investment engine and tax strategy, the next critical step is to build a strong defense through sophisticated risk management and define what your legacy will look like. This is where we move beyond basic insurance policies and simple wills.

We're talking about creating a durable framework that shields your family from the unexpected while thoughtfully preparing to transfer not just wealth, but your core values, to the next generation. This is how a financial plan matures into a lasting legacy.

Beyond Basic Insurance: Sophisticated Risk Management

For high-net-worth families, risk management isn't just about ticking a box with a life insurance policy. It’s about strategically deploying different types of insurance as powerful financial tools, designed to solve specific problems and protect your balance sheet from a catastrophic hit.

The goal is to create a formidable shield for your assets against creditors, lawsuits, and life’s unpredictable turns. We do this by taking a 360-degree look at your exposure and layering in the right kind of protection.

Some key strategies we often put in place include:

- Life Insurance for Estate Liquidity: We often use a large, permanent life insurance policy held within an Irrevocable Life Insurance Trust (ILIT). This creates a tax-free pool of cash that becomes available at precisely the right moment, allowing heirs to cover estate taxes without a fire sale of illiquid assets like the family business or real estate.

- Disability Insurance for Top Earners: Off-the-shelf disability policies usually have benefit caps that are laughably low for high-income professionals. We look at supplemental "own-occupation" policies that are designed to protect your specific income level and career, not just any job.

- Property & Casualty (P&C) Coverage: A high-limit umbrella liability policy is non-negotiable. This provides a crucial extra layer of protection on top of your standard home and auto insurance, safeguarding your entire net worth from a single major lawsuit.

Building Your Philanthropic Blueprint

With your wealth properly protected, you can shift your focus to its ultimate purpose. For many of our clients, this means aligning their philanthropic giving with their deepest-held family values. It’s not about haphazardly writing checks; it's about engineering a measurable impact in a way that’s both tax-smart and deeply fulfilling.

When you see data showing that only 39% of U.S. adults have even tried to plan for retirement, as reported by OppLoans, it highlights a massive need for financial foresight. That same intentionality is just as critical when planning your philanthropy.

A legacy isn't just about what you leave behind; it's about the values you instill and the structures you build. Effective philanthropy is a powerful way to translate financial success into a lasting, positive impact on the world.

There are several vehicles we use to make our clients' giving more effective:

- Donor-Advised Funds (DAFs): Think of a DAF as your family’s private charitable savings account. You can make a single large, tax-deductible contribution today, and then recommend grants to your favorite non-profits over many years.

- Private Foundations: For families looking to make a more substantial, multi-generational statement, a private foundation offers the ultimate control. It allows the family to be hands-on in the grant-making process and can become a central pillar of your family's identity and mission.

Nurturing the Next Generation: Family Governance

This might be the toughest—and most critical—piece of the puzzle: preparing your heirs to receive their inheritance. The old saying "shirtsleeves to shirtsleeves in three generations" is a cliché for a reason. Without a plan, inherited wealth can quickly become a destructive force rather than a blessing.

Family governance is simply the process of creating a structure for having productive, open conversations about wealth, values, and responsibility. It’s about arming the next generation with financial literacy and a sense of stewardship.

Some proven strategies we use to guide this process are:

- Drafting a Family Mission Statement: This isn't a corporate document. It’s a collaborative effort to put on paper the family's shared values and the guiding purpose of its wealth.

- Holding Regular Family Meetings: We often facilitate these meetings to create a dedicated forum for financial education, business updates, and philanthropic planning. It turns money from a taboo topic into a tool for collaboration.

- Involving Heirs Gradually: Instead of a surprise inheritance, we encourage clients to involve their children and grandchildren in smaller financial decisions, like helping manage a portion of the family's DAF or simply sitting in on investment review meetings.

This intentional process helps ensure your legacy is about far more than just money. It’s about preparing your family to be wise stewards of the resources and opportunities they've been given for generations to come.

Some Lingering Questions About HNWI Financial Planning

Even the most thorough roadmap can leave you with a few questions. We get it. Here are some of the most common things we're asked by clients navigating the world of high-net-worth planning.

How Often Should My Financial Plan Be Updated?

Your financial plan isn't something you can just set and forget. Think of it as a living document that needs to adapt as your life and the world around you change.

At a minimum, you should be sitting down for a full review once a year. But certain moments in life demand a more immediate look.

Think of it this way: your annual review is a routine check-up, but these life events are reasons for an urgent care visit.

- Major Life Changes: Getting married or divorced, a new baby, or the death of a family member all have massive financial implications.

- A Shift in Your Career: This could be a big promotion, launching a new business, selling one, or finally stepping into retirement.

- Significant Financial Events: Coming into a large inheritance, seeing your net worth jump or fall, or even a major swing in your investment portfolio.

- Changes in the Law: New tax codes or estate planning rules can pop up, and your plan needs to adjust accordingly.

Proactive adjustments are what keep a plan relevant—and powerful—over the long haul.

How Do I Find the Right Financial Advisory Team?

Picking the right team is, without a doubt, one of the biggest financial decisions you'll ever make. It's not just about chasing returns; it's about finding a true partner who gets the whole picture of your life.

The best advisors for high-net-worth families almost always work under a fiduciary standard. That’s not just jargon—it’s a legal obligation for them to act in your best interest, period.

When you're meeting potential advisors, you need to ask some direct questions:

- Are you a fiduciary? Don't settle for a complicated answer. It should be a clear and simple "yes."

- What’s your background? Look for designations like Certified Financial Planner™ (CFP®) or Chartered Financial Analyst (CFA). More importantly, ask about their experience with clients who look like you.

- How do you get paid? You need to know their fee structure inside and out. Are they fee-only, taking a percentage of the assets they manage? Or are they fee-based, which could mean they earn commissions on products they sell? Full transparency here is non-negotiable.

What Is a Family Office and Do I Need One?

A family office is basically your family’s private headquarters for managing its financial and personal affairs. As wealth scales, the complexity often outgrows what a traditional financial advisor can handle on their own.

A multi-family office (MFO) does this for a handful of affluent families, while a single-family office (SFO) is built to serve just one. You might start thinking about this path when your needs expand into areas like:

- Consolidated Reporting: Getting one clear picture of everything you own—from your stock portfolio and real estate to private equity and art collections.

- Administrative Heavy Lifting: Things like bill pay, managing a private jet, or coordinating household staff.

- Family Governance and Education: Help with running family meetings and preparing the next generation to be responsible stewards of the family’s wealth.

For most, a family office becomes the logical next step when the sheer administration of wealth starts getting in the way of actually enjoying it.

Building and maintaining a truly robust personal financial plan is the bedrock of your family's future. At Commons Capital, we specialize in bringing the clarity and strategic thinking that high-net-worth individuals need to master their complex financial lives. If you're ready to build a plan that truly reflects your unique vision and legacy, we invite you to connect with our team.