Imagine turning a risky startup investment into millions of dollars in tax-free gains. It sounds too good to be true, but it's a very real possibility thanks to Section 1202 of the tax code, better known as the QSBS tax exemption rules.

This powerful tax incentive was created to reward founders, early employees, and investors for taking a chance on and fueling the growth of innovative American companies. For anyone in the startup ecosystem, understanding these rules is critical for maximizing financial outcomes.

Your Guide to QSBS and Tax-Free Growth

For anyone involved in the startup world, understanding Qualified Small Business Stock (QSBS) isn't just helpful — it’s absolutely essential for maximizing your financial outcome. Think of it as a government-backed reward for taking on the high risk that comes with backing an early-stage venture. When that bet pays off and the company succeeds, this rule can completely eliminate federal capital gains taxes on a huge chunk of your profits.

Of course, a benefit this good isn't handed out automatically. A strict set of QSBS tax exemption rules dictates exactly who qualifies and how much they can save. Missing even a single requirement can be the difference between a tax-free windfall and a massive tax bill.

This guide will give you a clear, quick overview of the core eligibility rules, basically a checklist to see if your stock might be on the right track.

What Makes QSBS So Powerful?

The main attraction of QSBS is its potential for a 100% federal capital gains tax exclusion. For stock acquired after September 27, 2010, you can potentially shield gains up to the greater of $10 million or 10 times your initial investment (your adjusted basis). This creates a phenomenal opportunity for wealth creation, especially for those who get in on the ground floor of a breakout success.

To unlock this powerful benefit, you have to satisfy three main pillars of qualification:

- The Issuer: The company itself must be a U.S. C-corporation with gross assets of $50 million or less when the stock is issued.

- The Stock: Your shares must have been acquired directly from the company at their original issuance, and you have to hold them for more than five years.

- The Shareholder: The tax break is designed for non-corporate taxpayers, meaning individuals, trusts, and estates.

The QSBS exclusion is, at its heart, a tax-free exit strategy for the people who invest in and build America's next generation of great companies. It's a critical tool for driving innovation and rewarding risk-takers.

To give you a quick reference, here's a simple breakdown of these core requirements.

QSBS Qualification At a Glance

This table provides a high-level checklist for investors and founders to quickly assess whether an investment might qualify for the valuable QSBS tax exclusion.

Meeting these tests is the first, and most important, step on the path to a tax-free exit.

For small business owners, integrating QSBS into your bigger financial picture is crucial. It’s smart to look into comprehensive Estate Planning for Small Business Owners to make sure your business and personal goals are aligned. Properly structuring your assets from the start ensures you can take full advantage of powerful incentives like Section 1202. Navigating these rules requires careful planning from day one.

To unlock the powerful tax breaks under Section 1202, you can't just cross your fingers and hope for the best. It's more like a three-part harmony where the company, the stock, and the shareholder all have to be perfectly in tune.

Getting these specific QSBS tax exemption rules right is the most critical first step for any founder or investor. If even one part is off-key, the entire tax exclusion can be lost. Think of it as a series of gates you must pass through: one for the company, another for the stock itself, and a final one for you, the shareholder.

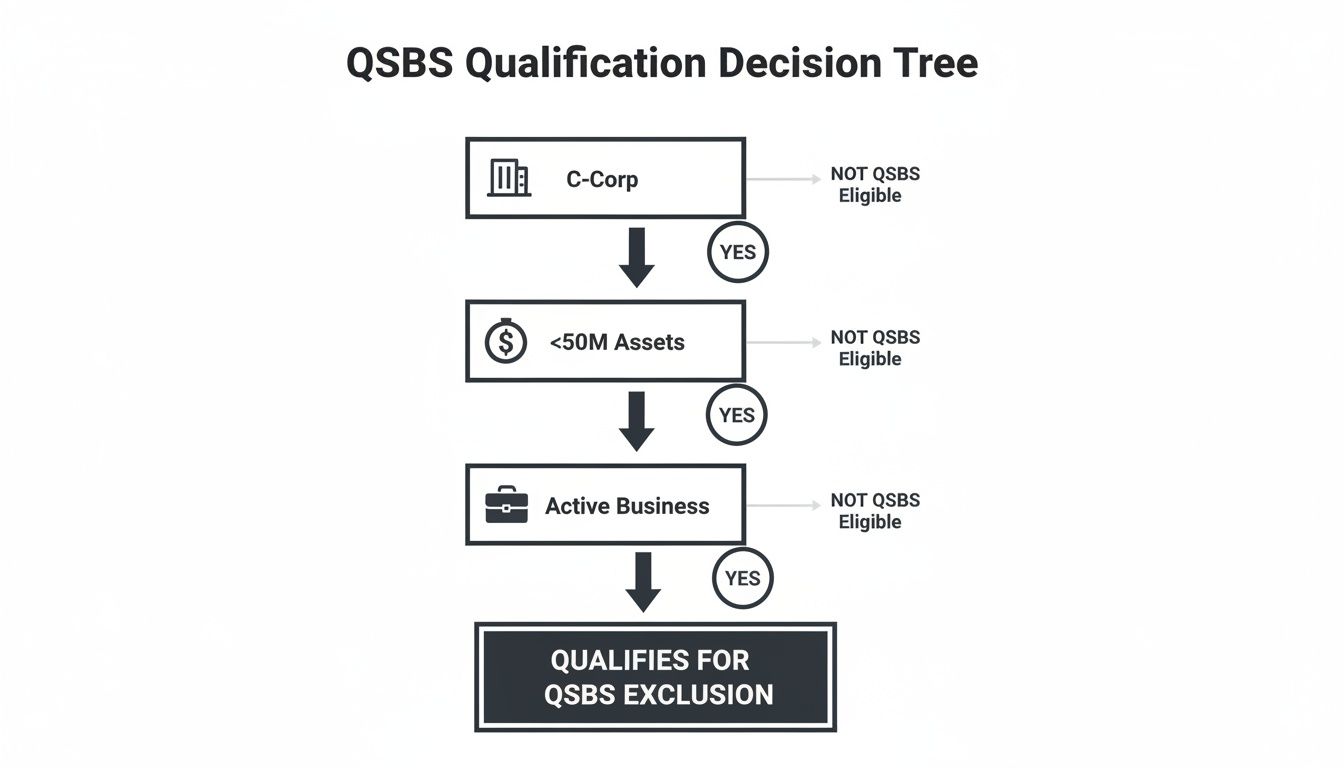

Issuer Requirements: The Company-Level Test

The entire foundation of a QSBS claim rests on the company that issues the stock. The rules are strict here, designed to make sure the tax benefits flow to real, U.S.-based small businesses, not just any investment. For its stock to qualify, a company has to pass a couple of key tests right when you get your shares.

First, the company absolutely must be a domestic C-corporation. This is a deal-breaker. Stock from S-corporations or LLCs simply won't work. When you're just starting out, thinking about how to choose business structure is a crucial decision that can have huge tax implications down the road.

Second, the company must pass the $50 million gross asset test. This is a snapshot in time. Right after the stock is issued to you, the company's total gross assets can't be more than $50 million. The good news? Once your shares are issued and qualified, the company can grow well past this limit without messing up your stock's QSBS status.

This decision tree gives you a quick visual of these core company-level hurdles.

As you can see, being a C-corp under the asset limit and running an active business are the first gates every company has to clear.

Shareholder Requirements: The Investor-Level Test

Once you've confirmed the company is on the right track, the spotlight turns to you, the shareholder. The main rule to remember here is the original issuance requirement. You have to get the stock directly from the company — not from another investor on a secondary market.

This rule is all about rewarding the people who put capital or sweat equity into the business during its risky early days. This usually happens in a few ways:

- Cash Investment: An angel investor writes a check to a startup for seed funding and gets equity in return.

- Property Contribution: A founder transfers valuable intellectual property, like a patent, into the new corporation in exchange for founder shares.

- Services Rendered: An early employee or founder gets stock as part of their compensation for helping build the company.

The "original issuance" rule is the cornerstone of the shareholder test. It ensures that the tax incentive benefits those who directly capitalize and build the business from the ground up, rather than those who buy in after the initial risk has been taken.

Stock Requirements: The Share-Level Test

Finally, we get to the stock itself. The most important rule here is the five-year holding period. To get the Section 1202 exclusion, you must hold the stock for more than five years before you sell it.

This is by design. The government wants to encourage patient, long-term investment, not quick flips. If you sell before that five-year clock runs out, you typically lose the tax break on that sale, though there might be other options like a Section 1045 rollover.

Here’s a quick example:

- Founder A gets her shares on January 1, 2020. She can sell them on January 2, 2025 (five years and a day later) and potentially pay zero federal tax on her gains.

- Investor B buys those same shares from Founder A on January 1, 2024. It doesn't matter how long Investor B holds them; the shares aren't QSBS for him because he didn't get them at original issuance.

This shows why it's not just what you own, but how and when you got it. For anyone new to this world, it’s worth understanding the broader ins and outs of private company investing to avoid these kinds of pitfalls.

How to Calculate Your QSBS Gain Exclusion

To really grasp the financial power of QSBS, you have to get comfortable with the math. The good news is that figuring out your potential tax savings is a straightforward, two-step process. First, you pinpoint the exclusion percentage based on when you got the stock. Second, you apply the overall cap.

For any founder or early investor trying to project their real, after-tax returns from a company exit, these two steps are absolutely essential.

The QSBS tax exemption rules weren't always as generous as they are today; they’ve changed quite a bit since the law was first created. This history directly affects how much of your gain you can shield from federal taxes, and it all comes down to one thing: when you acquired your shares.

Your Acquisition Date Determines Your Exclusion Rate

The path to the 100% exclusion we have today was gradual. Congress tweaked the law over the years, making the incentive increasingly attractive for those willing to make long-term bets on small businesses.

Here’s a quick breakdown of how the exclusion percentage works based on when you acquired your stock:

- Stock acquired between August 11, 1993, and February 17, 2009: You can exclude 50% of your eligible gain. The other half was historically subject to a higher capital gains rate, and part of the excluded gain was considered an Alternative Minimum Tax (AMT) preference item.

- Stock acquired between February 18, 2009, and September 27, 2010: The benefit got a nice bump. The exclusion jumps to 75% of your gain, and a smaller portion was flagged as an AMT preference item.

- Stock acquired after September 27, 2010: This is the game-changer. You can exclude a full 100% of your eligible gain, up to the cap. Even better, none of the excluded gain is subject to the AMT, making it a true tax-free home run.

The original Qualified Small Business Stock tax break was enacted on August 10, 1993. It started by letting investors in qualifying C-corporations write off up to 50% of their capital gains on stock held for over five years, creating a powerful tax advantage right from the get-go.

Understanding the Exclusion Cap: The Greater of Two Numbers

Even if you qualify for the 100% exclusion, your tax-free gain isn't unlimited. The IRS places a cumulative cap on how much gain you can exclude per company. This is where the QSBS tax exemption rules get really interesting and can create massive opportunities.

Your maximum excludable gain for stock from a single company is the greater of two amounts:

- $10 million, or

- 10 times (10x) your adjusted basis in the stock.

This "greater of" rule is what can turn a great tax break into a truly phenomenal one. It's especially powerful for founders and early investors who often have a very low initial cost basis in their shares.

Let's walk through a quick example to see this in action.

Founder Example

Imagine a founder, Alex, who starts a tech company. Alex contributes some intellectual property and a little cash, establishing an initial aggregate basis of $200,000 in founder shares. Nailing down this initial value is critical; our guide on understanding what a 409A valuation is offers more context on that process.

Years later, the company is acquired. Alex sells all of their shares for $35 million, realizing a total gain of $34.8 million. Let's assume Alex held the stock for more than five years and ticked all the other QSBS boxes.

Now, we apply the exclusion cap:

- Cap 1: The flat $10 million limit.

- Cap 2: The 10x basis limit, which is 10 x $200,000 = $2 million.

Alex gets to use the greater of these two figures. In this case, the $10 million cap is the clear winner. So, of the $34.8 million total gain, Alex can exclude $10 million from federal capital gains tax. The remaining $24.8 million would be taxed as a capital gain. While that's still a hefty tax bill, it's far smaller than it would have been without QSBS. This simple example shows both the incredible power and the clear limits of the standard calculation.

Advanced QSBS Strategies for Savvy Investors

Getting the basics of QSBS down is a great start. But for serial entrepreneurs and sophisticated investors, the real magic happens when you master the advanced planning strategies that live in the fine print.

These more complex rules are where you can defer huge tax bills, multiply your exclusion benefits, and weave QSBS into a much larger wealth strategy. It's about looking beyond a single exit and planning for a lifetime of investing.

The Section 1045 Rollover: A Powerful Deferral Tool

So, what happens when a fantastic buyout offer lands on your desk, but you're shy of the five-year holding period? This is exactly where a Section 1045 rollover becomes your best friend. It lets you sell your QSBS, pocket the proceeds, and defer the capital gains tax — as long as you reinvest that money into a new qualified startup.

This rule is a genuine lifesaver for investors who want to lock in gains from one successful venture and immediately redeploy that capital into the next big thing without a massive tax hit.

To pull off a Section 1045 rollover, you have to follow the playbook precisely:

- Hold the Original Stock: You must have held the first round of QSBS for more than six months before the sale.

- Reinvest Promptly: This is the big one. You have to buy your replacement QSBS within a strict 60-day window from the date you sold the original stock.

- Tack the Holding Period: The best part of the rollover is that your original holding period gets "tacked on" to the new stock. This is huge for hitting that critical five-year mark.

For instance, say you held your first QSBS for three years. After a 1045 rollover, you only need to hold the new stock for two more years to qualify for the full Section 1202 exclusion.

QSBS and the Alternative Minimum Tax (AMT)

Back in the day, the Alternative Minimum Tax (AMT) was a real headache for QSBS investors. A slice of the excluded gain from older QSBS stock was considered a "preference item," which could trigger the AMT and claw back some of those hard-won tax savings.

Thankfully, this is mostly a history lesson for anyone investing today.

For any QSBS acquired after September 27, 2010, the 100% excluded gain is not considered an AMT preference item. This change was a game-changer, cementing the QSBS benefit as a truly tax-free opportunity at the federal level for those who qualify.

While the AMT is off the table for the 100% exclusion, it’s a detail worth remembering if you’re holding onto older stock that only qualifies for a 50% or 75% exclusion. This table shows how the federal rules have evolved.

QSBS Federal Exclusion Rates Over Time

The federal capital gains exclusion for QSBS has improved significantly over the years, culminating in the 100% benefit that investors enjoy today. This table breaks down the changes based on when the stock was acquired.

As you can see, the post-2010 rules eliminated the AMT concern entirely for new QSBS investments, making the tax break much more straightforward and powerful.

Gifting and Estate Planning with QSBS

QSBS can also be a powerhouse for transferring wealth to the next generation with incredible tax efficiency. When you gift QSBS to someone else — like a child or grandchild — or place it in an irrevocable trust, the recipient gets to step into your shoes.

They inherit your original holding period and cost basis.

This means if you've held the stock for three years before gifting it, the recipient is credited with those three years. They only need to hold it for two more years to meet the five-year requirement. When they eventually sell, they can claim their own, separate $10 million (or 10x basis) exclusion. This popular strategy is known as "stacking."

This technique lets a family multiply the total tax-free gains from a single, highly successful block of stock. It's become a cornerstone of advanced estate planning for founders and high-net-worth families, but it requires careful coordination with your tax and legal team to execute correctly.

Understanding State Tax Rules for QSBS Gains

Nailing that 100% federal tax exclusion on your startup gains is a huge win, but it's only half the story. The QSBS tax exemption rules are a federal creation, and your home state gets its own say. It’s a common and costly mistake for founders and investors to forget this, and it can gut an otherwise tax-free exit.

How states handle QSBS gains is all over the map. Some follow the federal government's lead, others offer a partial break, and some tax the entire gain. This patchwork of rules means your final take-home number is directly tied to your zip code when you sell.

States That Conform to Federal QSBS Rules

A handful of states make things easy by fully conforming to Section 1202. If you live in one of these states and your gain is 100% free from federal tax, it’s also 100% free from state tax. These "conformity states" simply adopt the federal exclusion, which is the best-case scenario for any QSBS holder.

But state laws are not set in stone; they can and do change. You absolutely have to check your state’s current status when you’re planning your taxes, especially as a sale gets closer. A state that conforms today might not tomorrow.

States with Partial or No QSBS Conformity

This is where the real planning comes in. Several major states either partially conform or completely ignore the federal QSBS tax break, which can leave you with a massive tax bill.

Here’s the breakdown:

- Non-Conformity States: These states act like Section 1202 doesn't exist. Your federally tax-free gain is fully taxable at the state's going rate for capital gains or income.

- Partial-Conformity States: These states might give you some benefit, but it’s usually not as good as the federal deal. For example, a state might only recognize the old 50% exclusion or have its own set of unique and restrictive rules.

California is the most famous example of a non-conformity state. If you're a California resident, you could have a $10 million gain that’s 100% federally exempt, but the state will still tax every penny of it at its high income tax rates. To get a better handle on this specific problem, take a look at our guide on understanding capital gains tax in California.

This is a big reason why some research suggests QSBS disproportionately helps the ultra-wealthy, who can afford sophisticated residency planning. The 2017 TCJA's cut to the corporate rate to 21% also made C-corps (the only type eligible for QSBS) more popular. Still, hurdles like California's 13.3% tax on gains remain a major roadblock for many. You can see more on how the benefit flows to top earners in the full research from the Equitable Growth foundation.

The Importance of Residency Planning

With such wild differences in state taxes, your legal state of residence when you sell can become a multimillion-dollar decision. An investor living in a state like Florida or Texas might pay zero state tax on their QSBS gain. That same investor living in California or Pennsylvania would get hit with a huge state tax bill for the exact same transaction.

This has made residency planning a critical part of any advanced QSBS strategy. For founders and investors staring down a major exit, moving to a tax-friendly state well before a sale can save millions. But this isn't as simple as forwarding your mail. Establishing legal residency is a tricky process that demands careful documentation to hold up against scrutiny from high-tax states. You'll want to talk to a financial advisor to navigate these differences and make sure your exit is as profitable as possible.

Your Top QSBS Questions, Answered

As founders and investors dive into the QSBS tax exemption rules, a lot of practical questions pop up. The details can feel a little dense, but walking through a few common scenarios will bring a ton of clarity and help you make much smarter moves with your equity.

Let's tackle some of the most frequent questions we hear.

Does My Stock Lose QSBS Status if the Company Grows Past the $50 Million Limit?

No, it doesn’t. This is a critical point that trips many people up. The $50 million gross asset test is just a snapshot in time — it only matters at the moment the stock is issued to you.

Once those shares are in your hands, the company can grow well beyond that limit without putting your stock's QSBS eligibility at risk. In fact, this is central to the entire incentive. It's designed to let early-stage investors reap the full rewards of a company's high-growth journey down the road.

What Happens if I Sell My QSBS Before the Five-Year Mark?

If you sell your shares before hitting that five-year holding period, you won't get the Section 1202 gain exclusion for that sale. Any profit will be taxed as a standard capital gain.

But you might have another powerful play: the Section 1045 rollover. This rule allows you to push back the tax on your gain by reinvesting the sale proceeds into a different qualified small business stock. You have to act fast, though — the reinvestment must happen within 60 days of the sale. This strategy lets you "tack" the holding period of your first stock onto the new one, helping you get to the five-year finish line much faster.

A Section 1045 rollover is a go-to tool for serial entrepreneurs and active angel investors. It gives you the flexibility to exit an investment early without a huge tax bill, as long as you put that capital right back to work in another promising startup.

Can Stock I Received for My Work as a Founder Qualify for QSBS?

Absolutely. This is one of the most common ways founders and key employees get their hands on QSBS. Stock you get in exchange for your services — often called "sweat equity" — is definitely eligible.

The fair market value of your work when you receive the stock typically becomes your cost basis. From there, you just need to meet all the other QSBS requirements. That includes holding the stock for more than five years after it has fully vested and your holding period officially starts for tax purposes.

Sorting through the maze of QSBS rules and advanced strategies really benefits from an expert eye. The team at Commons Capital specializes in helping high-net-worth individuals, business owners, and founders build and keep their wealth. We can help you weave QSBS into your bigger financial picture to maximize what you take home after taxes.