If you're a high earner in your 40s, standard-issue retirement advice just won't cut it. Your financial world is more complex, and this is a critical decade where your peak earning power must meet an equally powerful, tax-efficient savings plan. Effective retirement planning for high earners in their 40s isn't just about saving — it's about deploying smart, specific strategies to protect and grow the wealth you're working so hard to build.

The goal? To fund a future that looks a lot like your life today. This requires a mental shift from simply accumulating money to strategically preserving it for the long haul.

Your Financial Wake-Up Call in Your 40s

Welcome to your peak earning years. For high-achievers, your 40s bring a potent mix of maximum income and mounting financial pressures. Generic retirement advice often misses the mark entirely because it wasn't built for the nuances that come with a significant income.

This decade is your make-or-break moment. The financial landscape has changed, and the responsibility for funding your own retirement now rests squarely on your shoulders.

The New Retirement Reality

For many high earners in their 40s, most of whom are part of Generation X, the retirement picture looks vastly different than it did for their parents. The era of cushy, employer-funded pensions is largely gone, replaced by self-directed plans like 401(k)s and IRAs.

Consider the numbers. While 44% of baby boomers had access to a traditional pension, a report from Equitable shows that a starkly lower 14% of Gen Xers have this same safety net. That’s a massive gap, and it highlights just how much more proactive you need to be.

This new reality demands a strategic pivot. It's no longer enough to just save. You have to optimize every dollar you put away.

Balancing Competing Priorities

Being a high earner in your 40s means you’re probably juggling major financial commitments that are all fighting for the same dollars. Sound familiar?

- Supporting a family: This can be anything from daycare and college funds to helping out aging parents.

- Maintaining your lifestyle: A higher income often brings a higher cost of living — mortgages, travel, and other expenses that make it tough to put long-term savings first.

- The urgent need for aggressive saving: You have a shorter runway to retirement than someone in their 20s, which creates immense pressure to save a substantial chunk of your income now. Our guide on how much you should be saving for retirement each month offers a closer look at this.

The challenge for high earners is framing this situation not as a problem, but as an opportunity. Your income is a powerful tool, and with the right plan, you can effectively manage these competing priorities while building a secure future.

To get started, let’s get straight to the point. Here are the most important things you should be doing right now to get your retirement plan on track.

Your Immediate Retirement Action Checklist

This checklist isn't exhaustive, but it's the perfect starting point. Taking these four steps puts you in control and lays the foundation for the more advanced strategies we'll cover. It's all about shifting from pure wealth accumulation to sophisticated, long-term wealth preservation. This guide is your roadmap.

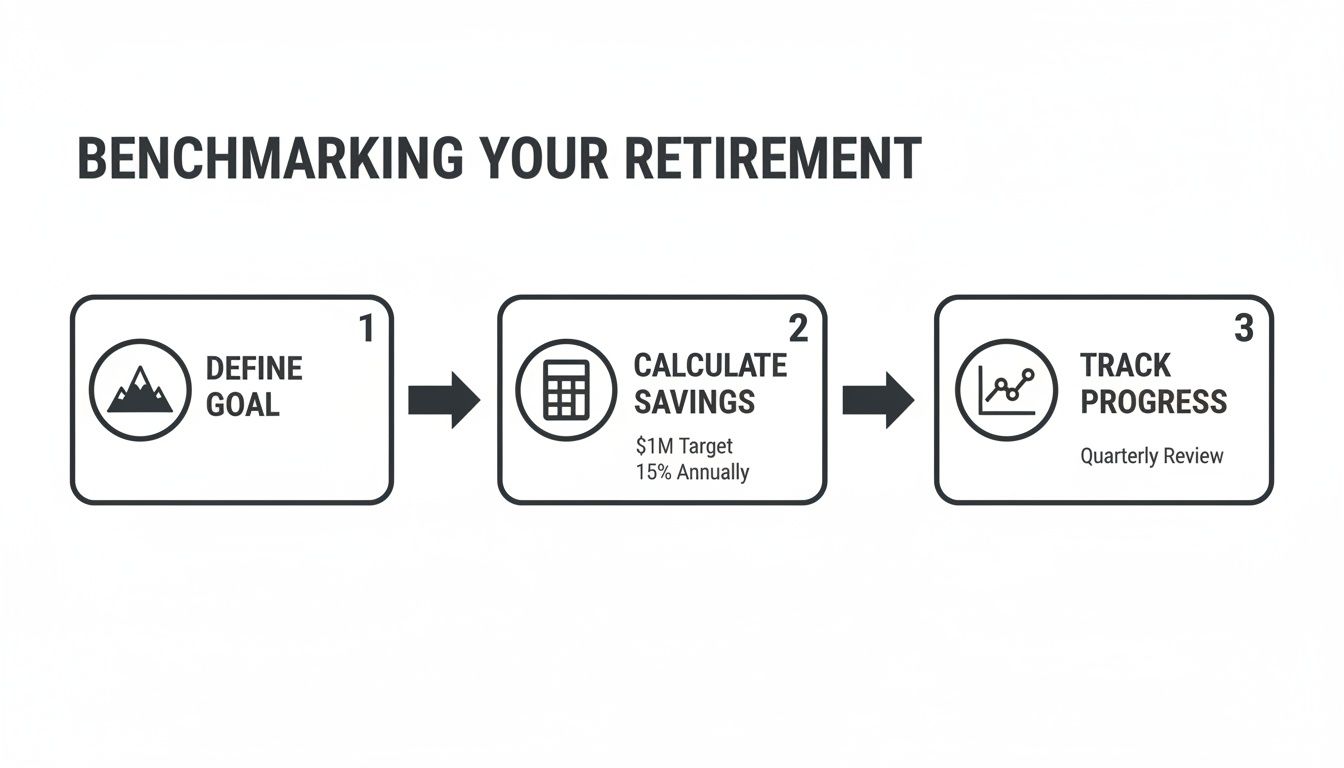

Benchmarking Your Progress for a High-Income Retirement

Those free online retirement calculators are fine for a quick check-in, but they often miss the mark for high earners in their 40s. Your specific goals, higher tax bracket, and lifestyle just don't fit into their simple formulas. This isn’t about just hitting some generic savings number; it's about figuring out exactly what it will take to sustain your standard of living decades from now.

Getting a handle on this number gives you real clarity. It's the difference between guessing and knowing whether you're actually on track. Think of your 40s as the critical base camp for your financial future — it’s where you stock up and plan your final climb to retirement.

From Vague Goals to a Concrete Number

The first real step is to stop thinking in terms of "a comfortable retirement" and start thinking about a specific dollar amount. This number becomes your personal target, the peak you’re aiming for.

A good way to get there is by using the 4% Rule, but flipping it on its head. Instead of just a rule for spending money down, use it to set your goal. For instance, if you picture yourself needing $200,000 per year to live on in retirement, you'll need a nest egg of $5 million ($200,000 divided by 0.04).

Suddenly, that fuzzy idea of "retiring well" becomes a tangible, measurable goal. It’s a powerful reality check and gives you a clear target to build your financial plan around.

Your retirement number isn't just a goal; it's the financial expression of your future freedom. Calculating it is the first real step in making that future a reality.

The Sobering Reality of Retirement Income

Many people, especially high earners, are caught off guard by how sharply their income can drop in retirement. The fall can be much steeper than you'd think. The data shows a stark picture: while median annual income might peak around $103,200 for people aged 55-59, it can plummet by more than 53% to $48,850 by the time they reach 75. For a deeper look at these figures, you can explore the average retirement income statistics.

This drop is usually a combination of savings running low, Social Security payments being fixed, and healthcare costs creeping up. For high-net-worth individuals, who often see a "comfortable" retirement as needing savings north of $823,800, this is a serious call to action. It proves you can’t just pile up assets; you need a smart plan for how you’ll draw down that money.

The High Cost of Delay

Time is your single greatest asset, and the power of compounding is what makes it so valuable. But it's an ally that heavily rewards getting started early. Putting off serious saving, even for just a few years in your 40s, comes with an enormous price tag.

Let's look at a simple example:

- Scenario A: The Early Starter

A 40-year-old starts putting away $50,000 a year for 25 years. With a 7% average annual return, they end up with roughly $3.16 million at age 65. - Scenario B: The Late Starter

Someone else waits five years and starts at age 45. They also invest $50,000 a year, but only for 20 years. At the same 7% return, they’ll have just $2.05 million by age 65.

That five-year delay cost them over $1.1 million in potential growth. It’s not just the contributions they missed; it’s the lost time for their money to grow on its own. Every year you wait makes the climb to your goal that much steeper.

Go Beyond the 401(k): Advanced Tax Strategies to Accelerate Your Savings

For high earners, your biggest opponent in the race to retirement isn't a volatile market — it's taxes. Simply maxing out your 401(k) is a great start, but on its own, it’s not enough to build the kind of wealth you’ll need for a comfortable retirement.

Think of your savings in three buckets: tax-deferred (like a traditional 401(k)), tax-free (like a Roth), and taxable (like a brokerage account). The real key to getting ahead is to aggressively and legally fill that tax-free bucket. That’s where the real growth happens.

The Problem With “Just Maxing It Out”

Once you hit your standard 401(k) contribution limit, the real work begins. Many high earners mistakenly think this is the end of the road for tax-advantaged saving, but several powerful tools are still on the table — if you know where to look.

Unfortunately, many are falling behind. Recent data shows that high earners in their 40s have an average retirement savings of $288,700. That sounds like a lot, but it’s a massive $535,100 shortfall compared to the $823,800 many experts believe is necessary for a comfortable retirement.

With 2026 contribution limits at $24,500 for a 401(k) and $7,500 for an IRA, it's clear that basic contributions alone won't bridge a gap that large. This makes moving on to more advanced strategies non-negotiable.

Unlocking Tax-Free Growth With Roth Strategies

The Backdoor Roth IRA and the Mega Backdoor Roth are two of the most effective tools high-income individuals have to build tax-free wealth. They’re designed specifically for people whose income phases them out of direct Roth contributions.

- The Backdoor Roth IRA: This is the go-to move when your income is too high to contribute directly to a Roth IRA. You simply make a non-deductible contribution to a Traditional IRA and then immediately convert it to a Roth. That money is now positioned to grow completely tax-free.

- The Mega Backdoor Roth: This is an even more powerful option, but it depends on your employer’s 401(k) plan allowing for after-tax contributions. After you max out your normal 401(k) contributions, you can contribute additional after-tax money — up to the combined federal limit (which was $72,000 in 2026) — and then convert those funds to a Roth account.

These Roth strategies are like giving your retirement savings a permanent tax shield. All future growth and every dollar you withdraw from these funds in retirement are completely tax-free. That’s a huge advantage over a standard taxable brokerage account. For a deeper dive, explore our guide on the best tax strategies for high income earners.

The Overlooked Power of an HSA

Often dismissed as just a healthcare account, the Health Savings Account (HSA) is secretly one of the most powerful retirement tools available. It's the only account that offers a triple-tax advantage. For high earners, understanding accounts like a Health Savings Account (HSA) is absolutely essential.

- Tax-Deductible Contributions: Your contributions lower your taxable income for the year.

- Tax-Free Growth: The money in your HSA grows without being taxed.

- Tax-Free Withdrawals: You can pull money out tax-free for qualified medical expenses at any time.

Here's the kicker: after you turn 65, you can withdraw funds for any reason. Those withdrawals are simply taxed as ordinary income, just like a traditional 401(k). This effectively turns your HSA into a "stealth IRA" you can use to supplement your retirement income.

To give you a clearer picture, this table compares the key features of the accounts we've discussed, using 2026 contribution limits as a baseline.

Comparing Tax-Advantaged Retirement Accounts in 2026

These accounts are the building blocks of a sophisticated savings plan. Using them in concert is how you start to make serious progress toward your goals.

Of course, before you dive into these advanced strategies, you need a solid foundation.

This simple process — defining your goal, calculating what you need to save, and tracking it — is the bedrock. Once you have that locked in, these powerful tax strategies can truly accelerate your journey toward financial independence.

Optimizing Your Investment Portfolio for Growth

Once you’ve maxed out your tax-advantaged accounts, it's time to get your investment portfolio firing on all cylinders. This is where the real wealth-building happens. For high earners in their 40s, we’re not just talking about a simple mix of stocks and bonds; we’re talking about constructing a portfolio designed for serious, long-term growth.

The goal isn't to chase the latest hot stock tip. It's about building a durable, diversified portfolio that can handle the market's inevitable ups and downs. Your investment returns will do most of the heavy lifting for the next couple of decades, making this a critical piece of retirement planning for high earners in their 40s.

Crafting Your Asset Allocation Model

Think of asset allocation as the blueprint for your portfolio. It's how you decide to split your money across different investments like stocks, bonds, and alternatives. For someone in their 40s with a high income, the main goal is growth, though protecting what you have starts to become more important.

A common starting point is a fairly aggressive stance, like an 80/20 or even a 90/10 split between stocks and bonds.

- Stocks (80-90%): This is your growth engine. You'll want a globally diversified mix of large, mid, and small-cap stocks from both the U.S. and international markets. This is what gives you the potential for significant returns.

- Bonds (10-20%): This is your portfolio’s shock absorber. High-quality government and corporate bonds offer stability and income, which helps cushion the blow during those inevitable stock market dips.

With decades still to go before retirement, you have time to recover from market downturns. This allows you to take on more calculated risk in exchange for a shot at much higher rewards. For a deeper dive into how this mix should shift as you get older, our guide on the best asset allocation by age lays it all out.

The right asset allocation isn’t a “set it and forget it” decision; it should change as your life does. But in your 40s, your portfolio should be firmly pointed toward growth, using the power of compounding to its fullest.

To really dial in a sophisticated portfolio, it's also crucial to understand the difference between an advisory vs. brokerage account. Working with an advisor often provides the personalized guidance needed to build and manage a complex asset mix that’s truly tailored to your goals.

Exploring Alternative Investments

While stocks and bonds are the foundation, high earners with more than $500,000 in investable assets often qualify as accredited investors. This opens the door to a completely different class of investments — alternatives that aren’t available to the general public.

These investments can add powerful diversification to your portfolio because their returns often don't move in lockstep with the public markets.

Common Types of Alternative Investments

- Private Equity: This means investing directly in private companies, often years before they might go public. The growth potential can be huge, but it comes with higher risk and you can’t pull your money out for long periods.

- Private Credit: Essentially, you're acting like the bank and lending money directly to businesses. This can create a steady stream of high-yield income that isn't tied to the ups and downs of the public bond market.

- Real Estate Syndications: This involves pooling your capital with other investors to buy large commercial properties like apartment complexes or shopping centers. It’s a way to get a piece of institutional-grade real estate without having to manage it yourself.

- Hedge Funds: These are sophisticated investment funds that use a wide range of strategies to try and make money whether the market is going up or down. They are highly specialized and require a lot of homework before jumping in.

Adding a 10-20% slice of these alternatives to your portfolio can help smooth out your returns and open up new avenues for growth. But make no mistake, these are complex, illiquid investments. Getting professional guidance isn't just a good idea; it's essential. The endgame is to build a sophisticated, multi-asset portfolio that can generate the returns you need to fund the retirement you’ve worked so hard for.

Protecting Your Wealth and Securing Your Legacy

You’ve spent years building your career and growing your net worth. That's the hard part, right? Not quite. Building wealth is one thing; keeping it is another challenge entirely. Without a solid defensive strategy, a single lawsuit or health crisis could unravel decades of your hard work.

This is the part of the plan that safeguards everything you’ve built. It’s about looking past your investment returns and focusing on the structures that protect you from the unexpected. For high earners, this isn't optional — it's a critical component of retirement planning for high earners in their 40s.

Fortifying Your Financial Defenses with Insurance

As your income and assets grow, so does your exposure to risk. Your standard home and auto policies just aren't enough. High earners are often seen as "deep pockets" in legal disputes, making them more attractive targets for litigation.

This is where umbrella liability insurance comes in. Think of it as a second, much larger layer of protection. If a lawsuit results in a judgment that exceeds the limits of your primary insurance, the umbrella policy steps in to cover the rest. It stops a legal claim from draining your personal savings and retirement funds.

Key Insurance Policies for High Earners

- Disability Insurance: Your ability to earn a high income is your most valuable asset. A good long-term disability policy replaces a significant chunk of your paycheck if an injury or illness keeps you from working.

- Life Insurance: If you have a family or dependents who rely on your income, term life insurance is a must. It creates a financial backstop to pay off the mortgage, cover daily expenses, and fund future goals like college if you're no longer around.

- Umbrella Liability: This adds $1 million or more in liability coverage on top of your existing policies. It's one of the most affordable and effective ways to shield a growing nest egg from legal threats.

Together, these policies create a safety net that ensures a single catastrophic event doesn't completely derail your financial life.

The Critical Role of Cash Reserves

In a market obsessed with growth, holding cash can feel like you're leaving money on the table. But a healthy emergency fund is the buffer that separates a minor setback from a major financial crisis.

Without enough liquid cash, a sudden job loss or a five-figure home repair could force you to sell investments at the worst possible moment. This not only locks in losses but also interrupts the compounding that builds long-term wealth. Aim for a cash reserve that covers 3 to 6 months of essential living expenses.

Don’t think of your emergency fund as an investment. It’s insurance for your investment plan. It buys you the freedom to stay invested during downturns, which is often when the best long-term gains are captured.

Laying the Groundwork for Your Legacy

Finally, protecting your wealth means deciding how it will be managed and passed on. Estate planning isn't just for billionaires; it’s a fundamental responsibility for anyone with a family and significant assets.

Getting these basic documents in order ensures your wishes are followed and can save your family a world of stress, money, and conflict down the line.

Essential Estate Planning Documents:

- Will: This is your instruction manual for distributing your assets. It also lets you name a guardian for minor children. If you don't have one, the state will make these crucial decisions for you.

- Trust: A living trust is a vehicle for holding your assets. It allows them to pass to your heirs privately, bypassing the often slow and public probate court process.

- Durable Power of Attorney: This document authorizes someone you trust to make financial decisions for you if you become incapacitated and can't manage your own affairs.

- Healthcare Directive: Also called a living will, this outlines your wishes for medical treatment in case you are unable to communicate them yourself.

Putting these legal structures in place is the final piece of your defensive playbook. It secures your legacy and gives you peace of mind that both your family and your wealth are protected.

Your Prioritized 12-Month Action Plan

We’ve covered a lot of ground on the challenges and powerful strategies for high earners in their 40s. But talking about it is one thing; doing something about it is another. It's time to turn all that theory into a concrete, year-long roadmap.

Think of this as your game plan. It’s designed to break down what can feel like an overwhelming task into manageable, sequential steps. Let's move from reading to doing, starting right now.

Immediate Actions: The Next 30 Days

The first month is all about building momentum. We're focused on high-impact, foundational moves that create the clarity and structure for everything that follows.

- Calculate Your Retirement Number: Vague goals are useless. It's time to get specific. Figure out your target annual income in retirement, apply a conservative withdrawal rate (like 3.5%), and work backward to find the total nest egg you need. This number is now your North Star.

- Max Out Your 401(k) Contributions: Don't wait. Log into your company's retirement portal today and adjust your contribution percentage to hit the annual maximum. It’s the simplest, most effective lever you can pull to lower your taxable income while putting your savings on hyperdrive.

- Automate Everything: Set up automatic monthly transfers from your checking account to your brokerage accounts and any other savings vehicles. Automation takes willpower out of the equation and guarantees you're paying yourself first, every single month.

In finance, the most powerful force isn't some complex algorithm — it's consistency. By automating your savings and defining your target in the first 30 days, you lock in the two habits that truly drive long-term success.

Goals For The Next Six Months

With that solid foundation in place, the next six months are for optimization. This is where we start layering in the more advanced strategies we discussed and shoring up your financial defenses.

Key Mid-Term Objectives

- Explore Advanced Tax Strategies: It’s time to do some digging. Find out if your 401(k) plan allows for after-tax contributions, which opens the door to a Mega Backdoor Roth. If you have a high-deductible health plan, open a Health Savings Account (HSA) and start funding it immediately.

- Review and Update Insurance Coverage: Pull out those life and disability insurance policies you haven’t looked at in years. Is the coverage enough for your current income and your family’s needs? While you're at it, call an insurance broker and get quotes for a $1 million to $5 million umbrella liability policy.

- Consolidate Old Retirement Accounts: If you have old 401(k)s collecting dust from previous jobs, it's time to roll them over. Consolidating them into a single IRA simplifies your life, often reduces fees, and gives you far more control over your investment choices.

Objectives For The Year Ahead

The final leg of your 12-month plan is about bringing in the professionals and thinking about the long-term. These steps formalize your strategy and make sure it’s built to last.

- Consult a Financial Advisor: Start scheduling meetings with a few fee-only financial advisors who specialize in working with high-net-worth clients. You're looking for someone who can pressure-test your plan, spot the blind spots you've missed, and guide you through complex investment and tax decisions.

- Draft or Update Estate Documents: This is non-negotiable. Book a meeting with an estate planning attorney to either create or update your will, trust, durable power of attorney, and healthcare directive. Protecting your assets and making sure your wishes are carried out is one of the most important things you'll do.

- Conduct a Full Portfolio Review: At the 12-month mark, sit down with your advisor for a deep dive. Review your asset allocation, rebalance the portfolio back to its target weights, and scrutinize how your investments have performed. Make the necessary adjustments to ensure you're still on the right track for the long haul.

Answering Your Top Retirement Questions

Even the most detailed plan can spark new questions. For high-earners in their 40s, a few specific concerns pop up time and time again as they navigate this critical financial decade. Here are the answers to some of the most common ones we hear.

I’ve Already Maxed Out My 401(k) and IRA. Now What?

First off, congratulations. That's a significant milestone and a common question from the most diligent savers. Once you’ve hit the limits on your primary retirement accounts, it’s time to move to the next tier of investment vehicles.

Your first stop should be to check if your 401(k) plan permits after-tax contributions. If it does, you can put the “Mega Backdoor Roth” strategy to work, potentially funneling a huge amount of extra cash into a Roth account. For many, this is the single most powerful next step.

After that, if you're eligible, fully funding a Health Savings Account (HSA) is a fantastic move. Its triple-tax advantages are unique, making it an incredibly efficient long-term investment account. From there, a taxable brokerage account is your go-to for building additional wealth. Just be sure to focus on tax-efficient funds, like broad-market ETFs, to keep the tax drag on your growth to a minimum.

How Much Do I Actually Need for a Comfortable Retirement?

The old "4% rule" is a decent starting point, but it's not always the best fit for high earners planning a retirement that could easily last 30 years or more. A more conservative withdrawal rate of 3% to 3.5% is often a smarter choice, as it builds in a much larger cushion for market swings and unexpected costs.

To find your baseline number, start with your desired annual income in retirement (say, $250,000). Then, just divide that by your chosen withdrawal rate.

- Example: $250,000 / 0.035 = roughly $7.15 million.

This simple math turns a fuzzy goal into a solid target. Of course, a financial advisor can help you dial in this number with more sophisticated projections that account for inflation, taxes, and future healthcare costs.

Is It Too Late in My 40s to Build a Serious Nest Egg?

Not at all. In fact, your 40s are often your peak earning years, giving you the financial muscle to save at a rate that just wasn't possible in your 20s or 30s. You might have less time for compounding to work its magic, but your ability to save significant, lump-sum amounts can more than make up for a later start.

The key is making every dollar and every account work for you. By consistently maxing out every available tax-advantaged plan and then aggressively funding a brokerage account, building a multi-million-dollar portfolio is still very much on the table. The only mistake is waiting any longer to begin.

Should I Pay Off My Mortgage Before I Retire?

This is a classic debate that pits the math against the emotion of it all. From a pure numbers perspective, if your mortgage rate is low — let's say under 5% — you will likely earn a much higher long-term return by investing your extra cash in the market rather than paying down the loan.

However, many people find the psychological benefit of entering retirement completely debt-free to be invaluable. There’s no single right answer here. A balanced approach often works best: consider making some modest extra payments on your principal while still hitting your primary investment goals. Ultimately, the decision comes down to your mortgage rate, your tolerance for market risk, and how much you personally value the security of owning your home free and clear.

At Commons Capital, we specialize in building personalized financial plans that solve the unique challenges high-net-worth individuals face. If you’re ready to get clear answers and create a definitive strategy for your future, we’re here to help. Contact us to learn how we can guide you toward your retirement goals.