For high-net-worth investors, an investment portfolio is more than just a path to retirement — it's a dynamic financial engine. But what happens when a prime opportunity requires immediate cash? Selling assets triggers taxes and disrupts long-term strategy. This is where securities-based lending comes in, a sophisticated tool a skilled wealth advisor uses to unlock liquidity without liquidation.

This strategy treats your portfolio like high-value real estate. Instead of selling the property to get cash, you borrow against its value. It’s a flexible line of credit secured by your stocks, bonds, and other eligible investments, giving you access to cash without ever having to hit the "sell" button.

Unlocking Liquidity Without Selling Your Portfolio

For high net worth families and business owners, it's a constant balancing act. You need cash flow, but you also need to keep your investments in the market and working for you.

Selling a highly appreciated stock to fund a new venture or cover a major expense comes with a steep price — a potentially large capital gains tax bill. Even worse, you permanently lose that asset and all its future growth potential. This is exactly the kind of costly dilemma a securities-based lending wealth advisor helps you sidestep.

How Securities-Based Lending Works

At its core, SBL is a straightforward collateralized loan. A private bank or other financial institution gives you a revolving line of credit, with your non-retirement investment account acting as the security. This setup, often part of comprehensive private banking services, offers game-changing advantages.

- You Keep Your Assets: Your securities stay in your account, in your name. You continue to collect any dividends and interest and benefit from any market appreciation.

- It’s Tax-Smart: Because you’re borrowing, not selling, you don’t trigger a taxable event. This lets you defer, and in some cases avoid, capital gains taxes on positions you’ve held for years.

- It's Fast and Flexible: Once the line is open, you have cash on demand. Funds can often be wired in as little as one business day, which is perfect for jumping on time-sensitive opportunities.

This is fundamentally different from other financing options, like unsecured business loans, where the lender has no direct collateral. With SBL, the portfolio securing the loan is what drives the favorable terms, interest rates, and overall structure.

The real power of securities-based lending is that it completely separates your need for cash from your investment decisions. It turns a static portfolio into a dynamic financial tool.

This strategy is a lifeline for investors with concentrated stock positions or anyone who needs to make a large purchase without derailing a meticulously built financial plan. A good advisor can help you figure out if this strategy is the right fit, ensuring it works for you without adding unmanaged risk. The key is to structure the line of credit intelligently, always keeping your long-term financial health front and center.

Use Cases: How HNW Investors Use Portfolio-Backed Loans

For a high net worth investor, a securities-based loan is much more than just another financial product. It’s a tool that turns a static investment portfolio into a dynamic source of cash, creating financial agility without derailing long-term wealth goals. Savvy investors use these portfolio-backed loans for all kinds of sophisticated financial moves. The applications are incredibly diverse, tailored to the unique situations of entrepreneurs, executives, and even retirees. This flexibility is a huge part of why SBLs have become so popular.

Seizing Time-Sensitive Opportunities

Imagine a perfect, off-market commercial real estate deal lands in your lap, but the seller needs a firm commitment in 48 hours. A traditional loan application would take weeks, and you’d miss out completely. This is a classic scenario where a securities-based lending strategy shines.

- Speed: Once a line of credit is in place, you can often have the funds wired in a single business day. That speed allows you to act decisively when opportunities won't wait.

- Flexibility: The money can be used for almost anything — a real estate down payment, seed money for a new venture, you name it. That’s far more freedom than you’d get with a typical mortgage or business loan.

By using an SBL, you could secure that property without selling a single share from your portfolio. You get to keep your market positions intact and avoid a big capital gains tax bill, all while closing the deal.

Tax-Efficient Liquidity and Estate Planning

One of the most powerful uses for an SBL is handling large, often unpredictable, financial obligations without triggering a taxable event. Think of a family facing a substantial estate tax bill or a large estimated quarterly tax payment.

Selling assets to raise that cash forces a tough choice: which of your winning investments do you have to part with, and how much will you owe in capital gains? An SBL offers a much cleaner path. By borrowing against the portfolio, the family can pay the tax liability on time while their assets hopefully continue to grow. It’s a way to manage cash flow needs strategically, defer taxes, and stick to your investment plan.

An SBL lets you solve a short-term cash need without making a permanent — and often costly — long-term investment decision.

This approach is also incredibly useful for investors with a large, concentrated position in a single company's stock. Instead of selling and facing a massive tax bill, they can use an SBL for liquidity. For a deeper dive into managing concentrated positions, investors might also look into options like an exchange fund to diversify without an immediate tax hit.

Bridging Income Gaps and Funding Major Purchases

The utility of an SBL also extends to personal finance, especially for wealthy clients with lumpy income streams. Professional athletes or business owners who get large, infrequent distributions are great examples.

An SBL can provide steady cash flow during an off-season or between big business deals, smoothing out that income volatility. This ensures they can maintain their lifestyle and meet financial commitments without being forced to sell assets at a bad time.

It’s the same logic for major life purchases — buying a yacht, acquiring fine art, or funding a destination wedding. An SBL offers a smarter way forward. It avoids the need to disrupt a carefully built investment portfolio, giving you the funds you need while your assets stay invested for the long haul. This strategic use of personal leverage has become a cornerstone of modern wealth management for HNW individuals.

How Interest Rates and Margin Calls Work

To fully leverage the power of securities-based lending, you must understand the key mechanics: interest rates, Loan-to-Value (LTV) ratios, and the possibility of a margin call. Mastering these concepts transforms what might seem like an intimidating financial tool into a predictable and manageable part of your strategy.

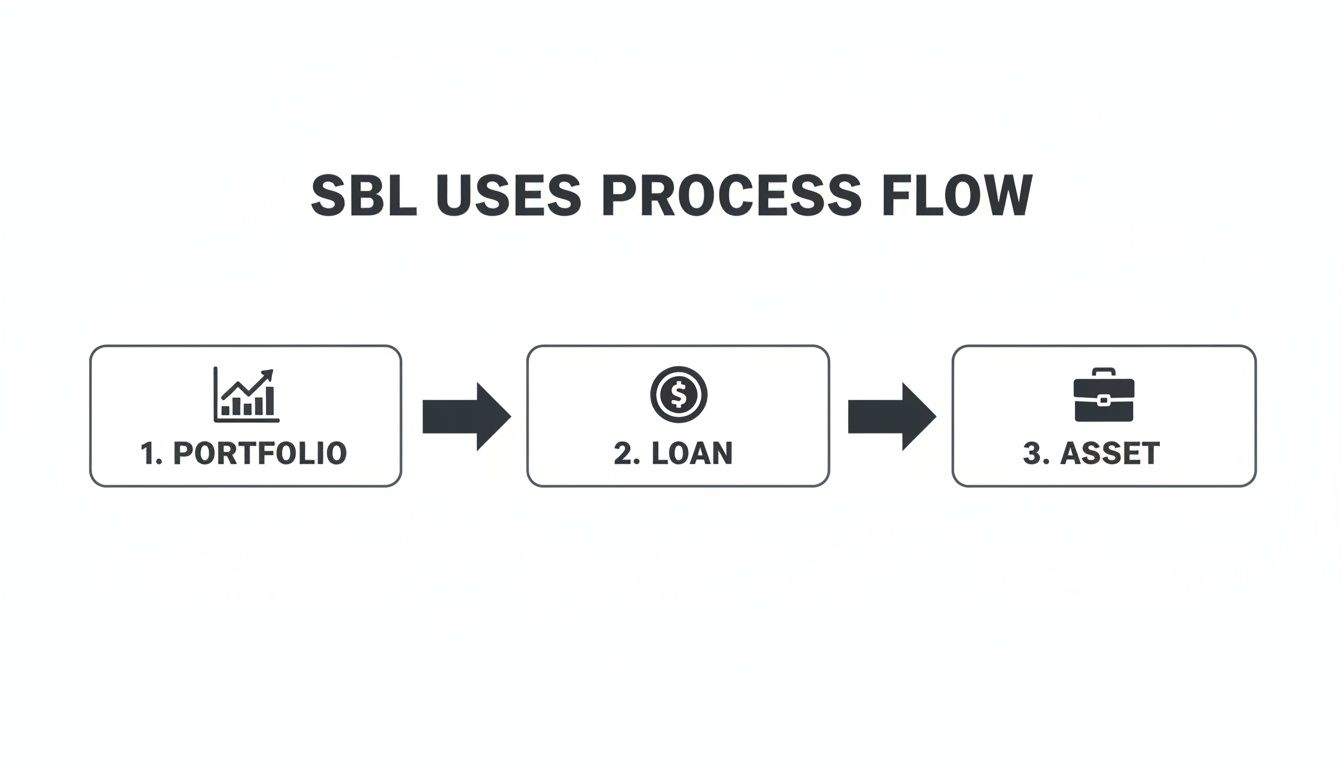

The process itself is quite simple. This graphic shows how you can unlock liquidity from your existing investments.

As you can see, your portfolio acts as the collateral that backs a new loan, giving you cash to acquire assets or meet other financial goals without disrupting your investment plan.

How Interest Rates Are Set

Unlike a fixed-rate mortgage, the interest on a portfolio-backed loan is almost always variable. This means the rate you pay can, and will, change over time. Lenders typically set the rate by taking a benchmark index — the Secured Overnight Financing Rate (SOFR) is a common one — and adding their own margin, or spread. That spread can depend on factors like the loan size and your overall relationship with the bank.

So, a rate might be quoted as "SOFR + 2.0%." If SOFR is currently at 5.0%, your effective interest rate would be 7.0%. If the benchmark rate drops, so do your borrowing costs. But the reverse is also true — if the benchmark climbs, your rate will rise with it. A good securities-based lending wealth advisor can help you stress-test your plans against potential rate hikes.

Understanding Loan-To-Value (LTV) Ratios

The Loan-to-Value (LTV) ratio dictates exactly how much you can borrow against your portfolio. Lenders assign an "advance rate," or LTV percentage, to every type of asset based on its perceived risk and liquidity. A stable, well-diversified portfolio will always unlock a higher LTV than a concentrated bet on a single, volatile stock.

Here’s a practical look at how that plays out:

- Diversified Stock and ETF Portfolios: Often receive an LTV of 50% to 75%. For a $2 million portfolio, that means a potential credit line between $1 million and $1.5 million.

- Investment-Grade Bonds: Due to their stability, these assets can command a very high LTV, sometimes up to 90%.

- Concentrated Stock Positions: A large holding in one company is riskier. The LTV for that position might be reduced to just 25% to 50%, or it may not be assigned any borrowing value at all.

The Risk of a Margin Call

A "margin call" is a risk-control measure for the lender. It happens when your collateral's value drops to a point where your loan balance breaches the maximum LTV threshold.

Let's walk through an example:

Say you have a $1 million portfolio and have borrowed $500,000 against it — a 50% LTV. If a market downturn causes your portfolio’s value to fall to $800,000, that $500,000 loan now represents 62.5% of your collateral’s value ($500,000 ÷ $800,000). You've now exceeded your 50% LTV limit.

When this happens, the lender issues a margin call. You can resolve it by:

- Depositing cash to pay down the loan balance.

- Adding more securities to the account to increase the collateral value.

- Selling some securities within the collateral account to reduce the loan.

A proactive advisor helps you avoid this situation entirely by setting conservative borrowing limits far below the maximum LTV, creating a cushion to absorb market swings.

Risks and How Fiduciary Advisors Manage Them

Leverage is a double-edged sword. While securities-based lending offers incredible flexibility, it introduces risks that must be managed with care. This is where a fiduciary wealth advisor becomes an indispensable partner, ensuring the loan serves your long-term goals without jeopardizing your financial future.

Fiduciary Duty Versus Bank Objectives

It’s crucial to understand the difference between a fiduciary advisor and the bank offering the loan. A bank profits from the interest it charges you; their business is built on lending money.

A fiduciary, however, has a legal and ethical duty to always act in your best interest. This creates a completely different relationship and adds a vital layer of protection.

A bank asks, "How much can this client borrow?" A fiduciary wealth advisor asks, "How much should this client borrow to safely achieve their goals?"

That shift in perspective is everything. Your advisor succeeds when your overall financial health improves, not by how large your loan balance is. This alignment ensures every decision about your portfolio-backed loan is made with your best interests at heart.

Proactive Risk Management Strategies

A good wealth advisor doesn't just react when the market gets choppy; they plan for it from the start. Managing the risks of leveraged investing requires a disciplined, forward-thinking approach. This is what separates a strategic asset from a potential liability.

Here are a few of the key strategies used to build a strong defensive buffer:

- Portfolio Stress-Testing: Before opening a line of credit, an advisor will run simulations to see how your collateral would hold up under extreme market conditions, like a steep recession or sector-specific downturn.

- Conservative LTV Buffers: A lender might offer a 70% LTV, but a prudent advisor will recommend borrowing far less. By setting a much lower personal limit — say, 40% to 50% — you create a significant cushion that can absorb market volatility.

- Developing a Margin Call Action Plan: Your advisor will work with you to build a clear, pre-determined playbook for a margin call scenario. This plan outlines exactly what steps to take, ensuring you never make a panicked decision in a downturn.

This disciplined approach ensures that securities-based lending remains a tool for creating opportunities, not a source of sleepless nights. For high net worth (HNW) families, that peace of mind is priceless.

SBL vs. HELOC vs. Margin Accounts

While a securities-based line of credit is a fantastic tool, it’s not the only one. For high net worth investors, strategic advantage comes from knowing when to use an SBL versus other options like a Home Equity Line of Credit (HELOC) or a traditional margin loan.

Securities-Based Lending vs. HELOCs

A HELOC lets you borrow against your home's equity. It’s a solid option, but it differs from an SBL in key ways. The biggest is speed and paperwork. A HELOC involves property appraisals and a full underwriting process that can take 30 to 60 days. An SBL is built for speed; because it’s secured by liquid assets, the line can be ready in just one or two weeks.

Furthermore, a HELOC puts your family home on the line. Many wealthy clients prefer the peace of mind that comes from separating their primary residence from their financing needs, which an SBL achieves by using the investment portfolio as collateral instead.

SBLs vs. Traditional Margin Loans

On the surface, an SBL and a margin loan look similar as both are secured by your investment portfolio. However, they are designed for completely different purposes. A traditional margin loan is for leveraged investing — borrowing money specifically to buy more securities within the same brokerage account.

An SBL is a non-purpose loan, meaning you can use the funds for almost anything except buying more securities. This is its key strength. You can move the cash out of your brokerage account to fund a business, purchase real estate, or handle a major personal expense. It’s about creating liquidity for your life, not just your portfolio.

Comparing Liquidity Options: SBL vs. HELOC vs. Margin Loan

Seeing these options side-by-side clarifies where each one shines. The best choice always depends on your specific goals.

For fast, flexible capital to seize opportunities outside the stock market, securities-based lending offers a combination of speed and versatility that the others simply can't match. A securities-based lending wealth advisor can help you navigate these trade-offs to make the smartest decision for your financial picture.

Common Questions About Securities-Based Lending

Here are some of the most common questions we hear from clients as they consider how this tool fits into their financial world.

Do I Still Receive Dividends from My Pledged Securities?

Yes, absolutely. You retain full ownership of your assets. That means you continue to collect all dividends, interest payments, and any capital gains distributions. Your voting rights also remain intact. Your portfolio is simply acting as collateral; your long-term investment strategy keeps working for you.

What Types of Securities Can Be Used for an SBL?

Lenders prefer collateral that's easy to value and sell. The quality of your portfolio directly impacts how much you can borrow.

- Top-Tier Assets: A well-diversified portfolio of blue-chip stocks, investment-grade bonds, and major ETFs will secure the best possible Loan-to-Value (LTV) ratio.

- More Complex Assets: Large concentrated positions, restricted securities, or certain alternative investments may still be usable, but expect a much lower LTV.

A securities-based lending wealth advisor can help position your collateral to unlock maximum borrowing power safely.

By retaining full ownership of your pledged assets, you ensure your investment strategy continues to work for you. An SBL provides liquidity without forcing you to sacrifice future growth, dividends, or voting rights.

Is the Interest Paid on an SBL Tax-Deductible?

The answer depends on how you use the money. If you use SBL funds for another investment — like purchasing an income-producing property — the interest you pay may be tax-deductible as an investment expense. If you use the loan for personal expenses like a vacation, the interest is generally not deductible. Always consult with your tax advisor to understand how these rules apply to your specific situation.

How Quickly Can I Access Funds from an SBL?

Speed is a major advantage. While initial setup can take a week or two, accessing your money afterward is remarkably fast. Once the line is open, you can typically draw funds via a simple wire transfer, with cash available in your account within a single business day. This agility is why SBLs are a powerful tool for high-net-worth (HNW) investors who need to deploy capital quickly.

At Commons Capital, we specialize in integrating sophisticated strategies like securities-based lending into your complete financial picture. We provide the fiduciary oversight needed to unlock liquidity while rigorously managing risk.