What if you could access the value tied up in your investment portfolio without selling a single stock? This is the central promise of securities-based lending (SBL), a powerful financial tool that offers a unique way to generate liquidity. For many investors, the main attraction is gaining flexible, low-cost capital while allowing their long-term investment strategy to continue uninterrupted. However, understanding the securities-based lending risks and benefits is crucial, as market volatility can lead to a "margin call," potentially forcing a sale at an inopportune time.

The Power and Peril of Securities-Based Lending

A securities-based line of credit lets you borrow against the value of eligible stocks, bonds, and ETFs in your portfolio. This financial instrument essentially unlocks the liquidity dormant in your investments, providing cash for new opportunities or unexpected expenses without derailing your wealth-building goals. But like any sophisticated financial tool, it must be handled with care.

The appeal is clear. You gain access to cash, often at more favorable interest rates than an unsecured loan, and avoid creating a taxable event that would occur from selling appreciated assets. This structure allows your investments to potentially continue growing even as you deploy the borrowed funds elsewhere.

Key Considerations at a Glance

For most investors, the decision to use an SBL comes down to a careful balance of opportunity against risk. The flexibility is remarkable, but its value is directly linked to the performance of the stock market. This introduces a type of risk that simply doesn't exist with traditional financing like a home mortgage.

Securities-based lending connects your liquid assets to your liquidity needs. It can be a brilliant strategic move for seizing an opportunity, but a gamble you shouldn't take without fully understanding the market-driven risks involved.

To put this trade-off into perspective, here’s a high-level look at the pros and cons you must carefully balance.

Securities-Based Lending at a Glance

The table below breaks down the fundamental give-and-take. On one side, you have significant strategic advantages. On the other, you have risks that are directly tied to market performance and require careful management.

Ultimately, an SBL can be an incredibly effective part of a sophisticated financial plan, but it’s not a set-it-and-forget-it solution.

Now that we have covered the basics of securities-based lending risks and benefits, let's explore how these credit lines function, examine real-world applications, and — most importantly — outline strategies to manage the inherent risks.

How Securities-Based Lending Actually Works

If you've ever navigated the traditional bank loan process, you’re familiar with the extensive paperwork and lengthy approval times. A securities-based line of credit (SBL) is fundamentally different, designed for investors who need liquidity without disrupting their portfolio.

The process begins when a lender evaluates your investment portfolio. Unlike a mortgage lender, their primary focus isn't on your income or credit score. Instead, they are concerned with which of your assets are eligible to be used as collateral.

Lenders typically prefer highly liquid, diversified holdings, such as publicly traded stocks, bonds, and exchange-traded funds (ETFs). After reviewing your portfolio, they will establish two key figures: the total size of your credit line and the advance rate. This rate is the percentage of your portfolio's value that you are permitted to borrow.

Determining Your Credit Line

The advance rate is the most critical factor, as it directly determines your borrowing power. For a standard, well-diversified portfolio, you can typically expect an advance rate between 50% to 70%. For highly stable assets, such as U.S. Treasury bonds, that rate can climb as high as 95%.

Let's illustrate with an example. Suppose you have a $2 million diversified portfolio. If the lender offers a 60% advance rate, you could secure a line of credit for up to $1.2 million. This isn't a one-time loan; it’s a flexible line of credit, similar to a home equity line of credit (HELOC), which you can draw from as needed.

One of the most powerful features of an SBL is that it's "non-purpose" for most uses. This means you can use the funds for almost anything — buying a vacation home, funding a new business, or covering a large tax bill. The one major exception is you can't use the money to buy more securities.

This flexibility is a significant part of what makes an SBL such a compelling tool for many investors.

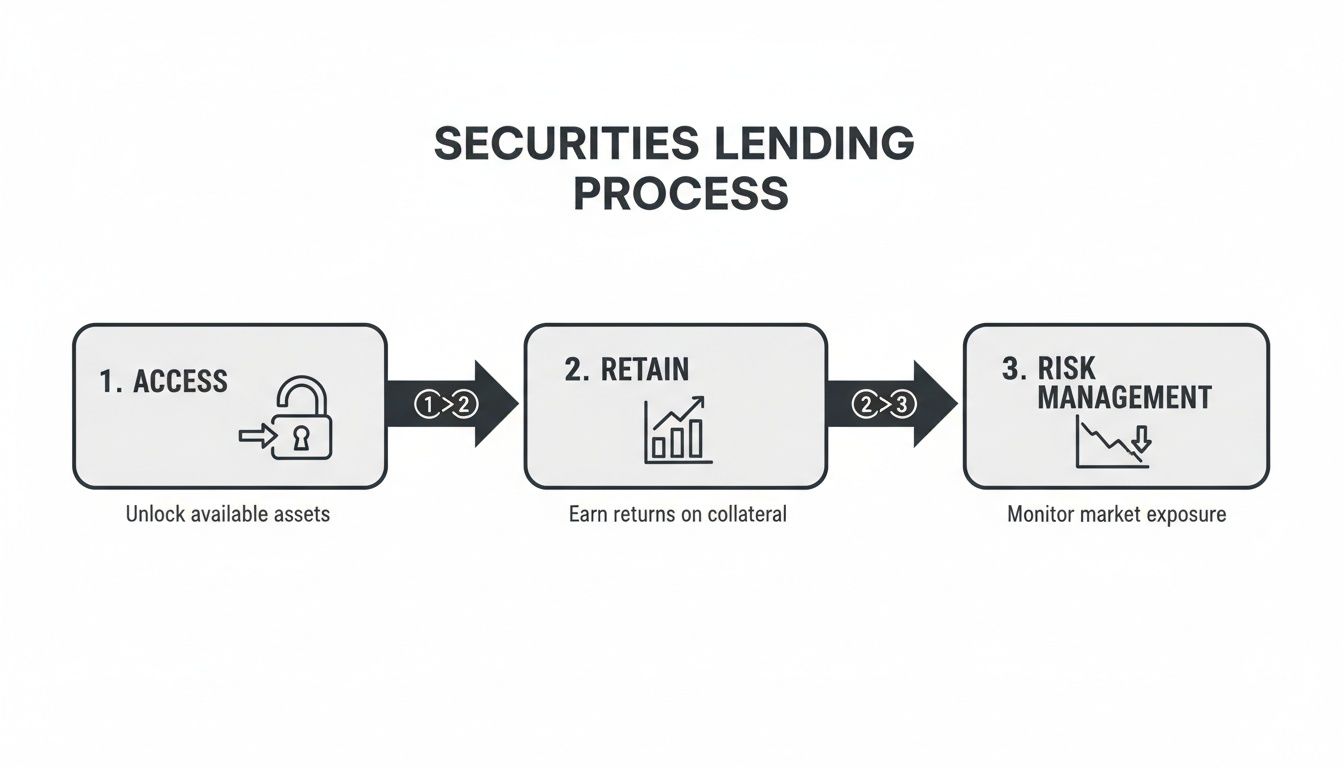

At its core, the process is a straightforward, three-step flow: you access cash, retain ownership of your assets, and manage the associated risk.

As the visual illustrates, you receive immediate access to capital while your investments remain in the market, hopefully continuing to appreciate. However, this also highlights the central tension of an SBL: balancing instant liquidity against the constant presence of market risk.

Understanding Interest Rates and Repayment

Another significant advantage of SBLs is their interest rate structure, which is often more attractive than rates for unsecured loans or even some mortgages. The rates are almost always variable, pegged to a benchmark index like the Secured Overnight Financing Rate (SOFR), plus a margin set by the lender.

Here’s how it typically works:

- Variable Rate: Your interest payments will fluctuate along with the benchmark index.

- Interest-Only Payments: Most SBLs provide the option to pay only the interest each month, which enhances cash flow.

- No Fixed Repayment Schedule: You can often repay the principal on your own timeline. It's important to remember, however, that the loan is technically callable by the lender at any time.

This structure offers incredible flexibility but comes with its own risks. If benchmark rates rise, your borrowing costs will increase as well. This is a crucial factor to consider, especially if you plan to carry a balance for an extended period. The entire system is built for speed and efficiency, turning your portfolio’s paper value into real-world cash with minimal friction.

Strategic Uses of Securities-Based Lending

When utilized correctly, a securities-based line of credit (SBL) is more than just a backup plan. For a savvy investor, it's a proactive tool for capitalizing on opportunities without derailing long-term financial goals. It effectively transforms your on-paper gains into real, usable capital.

For example, a business owner could use an SBL to fund a crucial expansion or acquire a competitor, all without issuing new stock and diluting their ownership. Similarly, a real estate investor might use it to make a quick, all-cash offer on a desirable property, bypassing the slower mortgage process that can cause deals to fall through.

Capitalizing on Tax Deferral

One of the most significant draws of SBLs is the tax advantage. By borrowing against your portfolio instead of selling appreciated assets, you can defer paying capital gains taxes. This allows your carefully constructed investment strategy to continue operating, compounding, and growing while you use the cash for other objectives.

The concept is simple, but its impact is huge: you get the cash value of your assets without actually triggering a taxable sale. This means your capital stays in the market, working for you and potentially growing enough to outpace the cost of the loan itself.

This tax-deferral strategy is particularly beneficial for clients holding highly appreciated stocks or those with strategies for a concentrated stock position. Needing cash doesn't have to mean facing a substantial tax bill, and an SBL is often a critical part of the solution.

This approach means you don't have to interrupt your portfolio's momentum just to achieve liquidity. It’s a way to have your cake and eat it, too — maintaining your market exposure while putting cash to work elsewhere.

How It Works in the Real World

To truly grasp the power of SBLs, let’s examine a few common scenarios where they provide a distinct advantage.

- Real Estate Investments: An investor identifies a distressed property at auction that requires a fast, all-cash purchase. An SBL provides the immediate funds needed to close the deal. The property can later be refinanced with a traditional mortgage, repaying the SBL and freeing it up for the next opportunity.

- Business Growth: A founder needs $1 million for new equipment to scale production. Instead of seeking venture capital and giving up equity, they draw on their SBL, maintaining full control of the company.

- Major Life Purchases: An individual wishes to buy a yacht or a second home. Using an SBL provides the necessary cash without liquidating a portion of their retirement portfolio, keeping their long-term financial plan intact.

- Managing a Large Tax Bill: An executive exercises a large block of stock options, resulting in a significant tax liability. They can use an SBL to pay the IRS promptly and then repay the loan over time without a forced sale of other investments at an inconvenient moment.

These examples demonstrate how an SBL can bridge the gap between your long-term wealth and short-term cash needs. It's an essential component that can be integrated into a broader strategic financial planning framework.

An Extra Layer: Earning Income on Your Collateral

While the primary purpose is borrowing, there is another angle to consider. The securities used as collateral can also be utilized in a separate income-generating strategy.

The securities lending market is a financial powerhouse, projected to generate US$14.9 billion in revenue in 2025. With average balances reaching US$3.25 trillion and a lendable asset pool of US$46.7 trillion, this opportunity is hard to overlook.

High-net-worth investors can lend their securities to institutions and earn additional income, which can boost portfolio yields by an average of 0.50%. This shows that the assets backing your SBL aren’t just sitting idle; they can remain productive parts of your overall wealth strategy.

Navigating the Key Risks of Borrowing Against Your Portfolio

While the benefits of tapping your portfolio for cash are powerful, they are not without risk. The potential downsides are very real and can cause significant financial damage if you are not prepared.

At the top of the list of securities-based lending risks is the margin call, a term that can send a shiver down the spine of even the most seasoned investor.

A margin call occurs when the value of your collateral — your investment portfolio — drops below a specific level set by the lender, known as the maintenance requirement. When your account breaches this threshold, the lender demands that you resolve the shortfall, leaving you with a few highly undesirable options.

You will have to either deposit more cash, pledge additional securities, or sell some of the very assets you borrowed against. The last option is often the most painful, as it forces you to lock in losses during a market downturn — the exact opposite of a sound investment strategy.

The Anatomy of a Margin Call

To understand how quickly a manageable loan can become a financial headache, let's walk through an example.

Imagine you have a $1,000,000 portfolio. You take out a $500,000 loan, starting with a 50% loan-to-value (LTV) ratio. Your lender sets the maintenance requirement at 70% LTV, meaning you will receive a margin call if your LTV ever rises above that level.

Here’s how a downturn can play out:

- Market Correction: The market experiences a sharp 30% decline, and your portfolio's value drops from $1,000,000 to $700,000.

- LTV Breach: Your loan amount is still $500,000, but your collateral is now worth significantly less. Your new LTV is calculated as ($500,000 loan / $700,000 portfolio), which equals 71.4%.

- The Margin Call: At 71.4%, you have crossed the 70% threshold. The lender immediately issues a margin call, and you are now on the clock to resolve the issue.

In this scenario, you are forced to act, either by providing more cash or selling assets at a market bottom. A forced sale can permanently impair your portfolio's ability to recover and grow, disrupting your long-term financial plan.

Concentration and Interest Rate Risks

Beyond a general market decline, two other major factors can threaten your loan: concentration risk and interest rate risk.

Concentration risk arises when a significant portion of your collateral is tied up in one or a few stocks. If that single company faces challenges — such as a poor earnings report, a regulatory hurdle, or a new competitor — its stock could plummet. This can trigger a margin call on its own, even if the broader market is stable. Diversification is not just for growing wealth; it's a critical shield when you borrow.

A diversified portfolio acts as a shock absorber. When you borrow against a concentrated position, you are removing those shock absorbers and exposing yourself directly to the performance of a single asset.

Interest rate risk is equally important. Most SBLs have variable interest rates pegged to a benchmark like SOFR. If the Federal Reserve raises rates to combat inflation, your borrowing costs will increase accordingly. A loan that seemed affordable at 5% can quickly become a heavy burden at 8% or more, straining your cash flow and altering the entire financial equation. This is why it is essential to understand not only your assets but also how to protect your assets from legal challenges and other financial pressures.

The bigger picture also matters. The private credit market's projected surge to $224.25 billion in fundraising by 2025 creates ripple effects. With these loans often fueling nonbank lending, a rise in corporate defaults from the projected 3.25% floor in September 2026 could set off a domino effect, sparking margin calls across the market. Staying informed on these global private credit market dynamics on S&P Global is crucial for managing these interconnected risks.

Choosing Between SBL and Other Liquidity Options

When you need cash, a securities-based loan offers incredible speed and flexibility. But it’s far from your only choice. It's crucial to weigh it against other common liquidity tools, like a traditional margin loan or a HELOC, to see what truly fits.

Each one has its own set of trade-offs. The right option for you will always come down to your specific financial picture, your comfort with risk, and exactly what you plan to do with the money.

SBL vs. Traditional Margin Loan

On the surface, an SBL and a margin loan can look almost identical. Both allow you to borrow against your investment portfolio. The real difference, however, lies in what they’re designed to do.

A traditional margin loan is part of your brokerage account and really only has one job: to buy more securities. It’s a tool for increasing your exposure to the market. That direct link means it amplifies both your potential gains and your risks.

An SBL, by contrast, is set up as an entirely separate line of credit. The funds are explicitly non-purpose, which is a formal way of saying you can’t use them to purchase securities. This structure makes an SBL a liquidity tool for life outside the market — funding a real estate purchase, covering a tax bill, or investing in a business.

Think of a margin loan as extra fuel for your investment engine, meant to increase its power inside the market. An SBL is more like a generator that taps into that engine's power to run equipment completely separate from your portfolio.

SBL vs. Home Equity Line of Credit (HELOC)

Another popular way to access a large sum of cash is a Home Equity Line of Credit, or HELOC. By using your home’s equity as collateral, a HELOC offers one major advantage: the collateral value is stable. It isn’t tied to the daily swings of the stock market, which completely eliminates the risk of a margin call.

That security comes at a price, though — primarily in time and convenience.

- Application Process: Getting a HELOC is a slow-moving process. It involves a mountain of paperwork, from income verification and credit checks to a formal home appraisal that can take weeks or months to complete. An SBL, on the other hand, is often approved in days, with cash available almost right away.

- Collateral Link: With a HELOC, there is a lien on your personal residence. If you default, you could lose your home — a deeply personal risk that many find unacceptable.

- Tax Implications: Interest paid on a HELOC might be tax-deductible, but only if you use the money to buy, build, or make significant improvements to your home. SBL interest is typically treated as an investment interest expense, which follows a different set of tax rules. We dive deeper into this in our guide on how to offset capital gains.

The decision here is a clear trade-off. A HELOC is slower but walled off from market risk, while an SBL is fast and flexible but directly exposed to your portfolio’s performance.

A Smart Framework for Using SBL Safely

Understanding the securities-based lending risks and benefits is one thing; applying that knowledge to protect your wealth is another. Using a securities-based line of credit (SBL) safely requires a disciplined, defensive game plan, not a reactive approach to market movements.

This means setting clear, personal rules before you draw a single dollar. The goal is to build a buffer so substantial that even a severe market correction won't place you anywhere near a margin call. This is how you maintain control, regardless of market volatility.

Building Your Personal Safety Net

The most effective way to manage SBL risk is to be conservative with your borrowing. A lender might offer a loan-to-value (LTV) ratio of 70%, but a prudent borrower should never approach that limit. We advise clients to establish a personal LTV cap around 25-30%. This creates a significant cushion against market turbulence.

Think of the lender’s LTV limit as the absolute edge of a cliff. Your job is to build your strategy so far from that edge that you're never even in danger of seeing it, let alone falling off. A low LTV is your first and best line of defense.

Beyond this core principle, a solid safety framework includes several other key pillars. These are practical steps you should review with your advisor to ensure an SBL works for you without adding unnecessary risk.

A Checklist for Responsible Borrowing

Before committing to an SBL, work through this checklist. It will help pressure-test your strategy and force you to create a clear plan for any scenario.

- Stress-Test Your Portfolio: What would happen to your portfolio and LTV in a 20%, 30%, or even a 40% market downturn? Run the numbers to see where your personal LTV would stand in a severe correction.

- Confirm Collateral Diversification: Is the collateral you’re pledging spread across different assets and sectors? Never pledge a highly concentrated stock position, as a downturn in a single company could be enough to trigger a margin call.

- Define Your Exit Strategy: How will you repay the loan? Have a clear and realistic plan from day one, whether through future income, the sale of another asset, or a planned refinancing event.

- Establish a Review Cadence: Markets and your financial situation are constantly changing. As you use an SBL, it’s critical to regularly review your loan and its terms. We recommend scheduling quarterly or semi-annual check-ins with your advisor.

By proactively managing these moving parts, you can transform an SBL from a potential landmine into a dependable financial tool, providing both confidence and genuine peace of mind.

Your Top Questions About Securities-Based Lending, Answered

Even after understanding the broader concepts, many practical questions arise when considering a securities-based loan (SBL). Here are some of the most common inquiries we receive, with straightforward answers.

What Types of Securities Work Best for an SBL?

Lenders are quite particular about the collateral they will accept. They don't just accept any asset; they have a strong preference for portfolios that are:

- Highly Liquid: Think publicly traded stocks, bonds, and ETFs. These are assets a lender can sell quickly without significantly impacting the price if necessary.

- Well-Diversified: A portfolio spread across different sectors and industries is always safer than one heavily concentrated in a single stock. Pledging a balanced portfolio dramatically reduces the risk that a poor earnings report from one company will trigger a margin call.

- Relatively Stable: While all assets experience volatility, lenders prefer those with a history of lower price swings. A collection of blue-chip stocks, for instance, is far more attractive as collateral than a portfolio of speculative small-cap stocks.

Attempting to use a highly concentrated or illiquid position as collateral is a risky strategy that almost always results in a much lower loan offer — if one is offered at all.

Do I Still Get Dividends from My Pledged Securities?

Yes, absolutely. This is a crucial point that is often misunderstood. Pledging your securities is not the same as selling them. You retain beneficial ownership.

This means you continue to collect every dividend and all interest payments your assets generate. Your portfolio keeps working for you, just like it did before the loan.

You remain exposed to the market’s potential upside (and downside), and that dividend income can continue to compound or even help cover the interest payments on your SBL.

How Fast Can I Get Funds from an SBL?

Speed is one of the biggest advantages. Compared to the weeks or even months it can take to get a home equity line of credit approved, an SBL moves at lightning speed.

Once your account is set up, which often takes only a few days, you can typically access your funds within one to two business days. This makes an SBL an excellent tool for seizing time-sensitive opportunities, such as making a compelling all-cash offer on real estate or injecting capital into a business at a critical moment.

What Happens If I Can’t Meet a Margin Call?

This is the most critical risk to understand. Failing to meet a margin call has immediate and serious consequences. If you are unable to deposit more cash or pledge additional securities to bring your loan-to-value (LTV) ratio back into compliance, the lender has the right to liquidate your assets.

They will begin selling your pledged securities to reduce your loan balance until the LTV is back within the agreed-upon limits. The worst part is that they can do this without your permission and at the absolute worst time — in a down market. This forces you to sell low, locking in losses and potentially derailing your long-term financial plan for good.

At Commons Capital, we help our clients navigate the complexities of securities-based lending, ensuring it aligns with their broader wealth management strategy. To discuss how you can use liquidity tools safely and effectively, contact us today.