You may be asking “what does wealth management do” because your financial life no longer fits in one spreadsheet.

That usually happens after a business sale, a major equity windfall, a new executive compensation package, or a contract year in sports or entertainment. What used to be a straightforward question of “How should I invest this?” turns into several harder questions at once. How should assets be titled? Which accounts should hold which investments? When should gains be realized? How do trusts, insurance, retirement income, and family gifting fit together without creating unnecessary tax friction?

A wealth manager’s job is to coordinate those moving parts into one coherent plan. Not just investments. The whole financial architecture.

That need isn’t niche. The global wealth management industry is projected to manage $176.54 trillion by 2030, and the United States is home to 24 million millionaires, four times more than any other country, which helps explain why demand for expert advice keeps rising, according to wealth management industry projections and millionaire demographics.

Beyond Investing Navigating Financial Complexity

A business owner after a liquidity event often makes the same discovery. The transaction closes, cash arrives, and relief lasts about a week. Then the complexity shows up.

There may be concentrated stock positions, estimated taxes, trusts that need review, real estate held in multiple entities, family members with different expectations, and a sudden stream of pitches from banks, brokers, and private investment sponsors. None of those issues is impossible on its own. The problem is that they interact.

An entertainer with a new contract faces a different version of the same problem. Income can be large but uneven. Taxes may hit hard and fast. Spending rises before a long-term plan is in place. Advisors can start working in silos, with one person handling investments, another doing tax returns, another reviewing legal documents, and no one making sure the full strategy fits together.

That’s where wealth management earns its keep. The role is part strategist, part coordinator, part risk filter. Good wealth management acts as the central quarterback for your financial life so decisions in one area don’t undermine another.

A strong wealth plan should reduce decision fatigue, not add another layer of it.

This matters even more when assets cross borders or family structures become more complex. For readers dealing with international holdings, entity planning, or cross-border property exposure, this guide to strategic planning for real estate investments through foreign trusts is a useful example of the kind of specialized planning issue that often sits adjacent to traditional portfolio work.

What clients are usually buying

They’re rarely buying “market access.” Markets are easy to access.

They’re buying:

- Coordination: Making tax, estate, investment, and cash flow decisions work together.

- Judgment: Filtering opportunities that sound impressive but don’t improve outcomes.

- Continuity: Keeping the plan aligned as life changes, laws change, and markets move.

- Clarity: Turning a complex balance sheet into a manageable decision framework.

When done well, wealth management creates peace of mind through structure. That sounds soft. In practice, it’s highly operational.

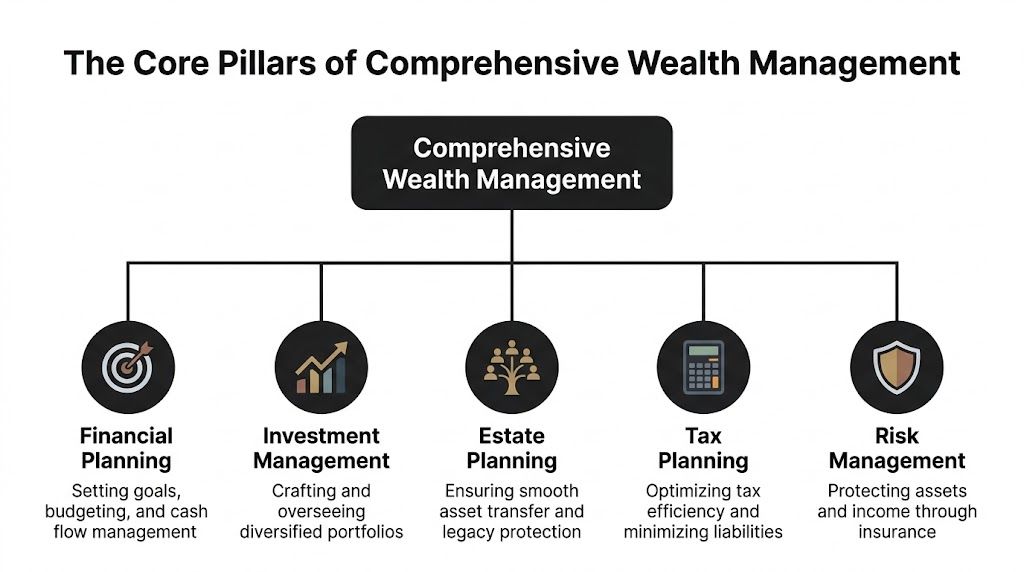

The Core Pillars of Comprehensive Wealth Management

Wealth management works best when you think of it as a load-bearing structure. Each pillar supports the others. If one is weak, the entire plan becomes less efficient.

Investment management

This is the pillar often recognized initially, but it’s only one part of the work.

A core function is applying Modern Portfolio Theory to build portfolios that target returns while controlling risk through diversification. By diversifying across uncorrelated assets such as stocks, bonds, and real estate, portfolio volatility can drop by 20% to 30% compared with concentrated holdings. That systematic approach, which can include strategies such as tax-loss harvesting, can outperform DIY investing by 1% to 3% net annually, according to private wealth management analysis on portfolio construction.

The practical point isn’t academic theory. It’s avoiding fragile portfolios. Many affluent investors don’t have a diversification problem because they don’t know the rule. They have one because they became wealthy through concentration and find it emotionally difficult to diversify away from what made them rich.

Financial planning

A portfolio without a plan is just a pile of accounts.

Financial planning connects assets to actual life decisions. Retirement timing. Lifestyle spending. College funding. Charitable giving. Liquidity reserves. Family support. A good plan forces trade-offs into the open so you can make them deliberately instead of drifting into them.

For that reason, planning has to include cash flow. High net worth doesn’t automatically mean high liquidity. I’ve seen clients with valuable businesses, appreciated real estate, and taxable portfolios still feel cash constrained because income timing and spending patterns weren’t aligned.

Tax strategy

Many investors frequently underestimate the difference between pre-tax returns and after-tax results.

Tax planning isn’t just about filing accurately. It’s about account location, gain realization, charitable strategy, stock compensation planning, withdrawal sequencing, and coordinating investment activity with your broader tax picture. The wrong asset in the wrong account can imperceptibly lower net results for years.

Practical rule: If your investment strategy and tax strategy are being run separately, you probably have avoidable drag in the system.

Tax-loss harvesting is one example, but the bigger issue is integration. The tax plan should influence how the portfolio is managed, not just clean up after it.

Estate and legacy planning

Estate planning answers a simple question with complicated consequences. Where should your assets go, and under what terms?

For some families, that means making transfers efficient and orderly. For others, it means controlling how wealth moves across generations, protecting beneficiaries, or supporting philanthropic goals. The mistake is treating estate documents as a legal formality. They’re part of the operating system of your wealth.

A will, trust structure, beneficiary designations, business succession documents, and powers of attorney need to match. If they don’t, the family usually discovers the mismatch at the worst possible time.

Risk management

Affluent families often focus on investment risk and ignore the other risks that can do more immediate damage.

Those include liability exposure, disability, premature death, property gaps, cybersecurity issues, and concentrated business or real estate exposure. Risk management is less about buying products and more about identifying what would materially disrupt the plan.

That can mean reviewing insurance coverage. It can also mean revisiting ownership structures, umbrella liability, key person protection, or basic operational controls around accounts and family access.

Why integration matters

These pillars are not separate departments in a perfect world. They’re one system.

A concentrated stock position isn’t only an investment issue. It may affect tax timing, charitable planning, estate transfers, and family governance. A retirement income plan isn’t only a planning issue. It changes portfolio liquidity needs and tax decisions.

For a broader look at how these components fit together in practice, Commons provides additional perspective in its wealth management insights library.

Your Journey with a Wealth Management Team

The client experience should feel orderly from the beginning. If the onboarding process is vague, the ongoing relationship usually will be too.

Discovery first

The first phase is diagnosis, not product selection.

A capable team will ask for a complete picture: balance sheet, income sources, tax returns, estate documents, insurance, business interests, compensation structure, and family goals. They’ll also ask questions that don’t show up on statements. What are you trying to protect? Which obligations matter most? What decisions are you avoiding because the choices feel unclear?

This stage often surfaces the core work. Not “pick better investments,” but “untangle multiple objectives that compete with each other.”

Strategy and plan development

Once the facts are clear, the team builds a coordinated plan.

That plan should identify priorities, sequencing, and trade-offs. Which accounts should be repositioned first? Where is liquidity needed? Which legal or tax conversations need to happen before portfolio changes are made? For some clients, the first recommendation is investment-related. For others, it’s pausing action until tax or estate details are sorted out.

Implementation

At this point, many financial relationships fall apart.

A good plan only matters if someone carries it across the line. Accounts need to be opened or consolidated. Beneficiaries updated. Investment allocations executed. Estate attorneys and CPAs looped in. If the plan depends on several professionals, someone has to own the handoff process.

The value of advice often shows up in execution quality, not presentation quality.

Ongoing review and adaptation

Wealth management is not a one-time event.

Markets move. Tax situations change. Families change. Businesses are sold, children mature, spending shifts, health events happen. A useful advisory relationship revisits the plan regularly and adjusts before small misalignments become expensive ones.

The best review meetings don’t just recap performance. They answer a better question: does the current strategy still fit the life it was built to serve?

How Wealth Management Fees Align with Your Success

Most wealth management firms use an assets under management fee model. In plain English, the firm charges a percentage of the assets it manages for you.

That structure is common because it aligns the advisor’s economics with the client’s balance sheet. If your assets grow and remain under management, the firm benefits. If assets shrink or the relationship ends, the firm doesn’t. That isn’t perfect alignment in every circumstance, but it’s usually cleaner than a model that pays only for transactions or product sales.

What the fee is supposed to cover

A legitimate wealth management fee should reflect more than portfolio selection. It should include the integrated work around planning, tax coordination, estate collaboration, rebalancing, cash management guidance, and ongoing decision support.

That’s where clients should be demanding. If a firm charges on assets but mostly delivers performance commentary and quarterly calls, the relationship may be priced like wealth management and delivered like basic portfolio supervision.

Other models you may see

Some advisors use flat annual retainers. Others work hourly. Those models can make sense when the client needs planning without ongoing asset management, or when the relationship is more project-based.

The trade-off is usually one of scope and continuity. AUM fees tend to support continuous oversight. Flat or hourly arrangements can work well for defined planning engagements.

For readers comparing structures in more detail, this wealth management fees comparison guide is a useful starting point.

Wealth Management vs Other Financial Services

Many people use wealth management, financial planning, and asset management as if they mean the same thing. They don’t.

The distinction matters because each service solves a different problem. If you only need a retirement roadmap, a full wealth management relationship may be more than you need. If your balance sheet includes business interests, trusts, concentrated holdings, and multigenerational goals, a narrower service may leave important gaps.

Comparing financial advisory services

The practical difference

Financial planning usually starts with goals. It asks, “What do you want your money to do?” It may produce an excellent roadmap, but implementation can remain with the client or separate professionals.

Asset management starts with the portfolio. It asks, “How should these assets be invested?” That can be highly valuable, especially for institutions or investors who already have planning and tax support elsewhere.

Wealth management starts with the client’s entire balance sheet and decision environment. It asks, “How should all of these moving parts be coordinated so your wealth serves your life efficiently?”

If one advisor manages the portfolio, another handles taxes, and another updates estate documents, wealth management is the discipline that makes sure those decisions don’t conflict.

This is why affluent clients often move into wealth management after a trigger event. A sale, inheritance, retirement transition, or contract cycle creates enough complexity that siloed advice stops being efficient.

Who Truly Needs a Wealth Manager

Not every investor needs wealth management. The service becomes most valuable when complexity, not just asset size, starts driving the risk.

High-net-worth families

Families with meaningful assets often have goals that pull in different directions. They want growth, but also stability. They want to help children, but not undermine responsibility. They want efficient transfers, but also control and privacy.

These are not spreadsheet-only problems. They require decisions about account structure, estate intent, governance, and communication. The need becomes more urgent as wealth moves across generations and family branches.

Business owners

Business owners often look wealthy on paper long before their liquidity matches their net worth.

Their planning questions are different from those of a salaried executive. How much personal risk is tied to the business? When should they diversify? How should a future sale be staged? What happens if a succession plan exists informally but not legally? The portfolio can’t be managed in isolation because the business already dominates the household balance sheet.

Sports and entertainment professionals

This group is one of the clearest examples of why generic advice fails.

For niche clients in sports and entertainment, wealth management is critical. The average NFL career lasts 3.2 years, and 78% of players face financial distress within two years of retirement, according to analysis on financial planning risks for athletes and entertainers. Wealth managers in this context handle cash flow forecasting, tax mitigation for lump-sum contracts, and managing short earning windows.

The challenge is rarely “make this money grow.” It’s “make this income last after the peak earning period ends.” That changes everything from liquidity planning to spending discipline to how endorsement or royalty income is structured and managed.

Retirees with complex distributions

Retirement planning becomes more demanding when wealth sits across taxable, tax-deferred, trust, and real estate buckets.

The key issue is no longer accumulation. It’s sequencing. Which assets should fund spending first? How much risk should remain in the portfolio? Which distributions create unnecessary tax friction? A wealth manager helps retirees balance income needs, family goals, and portfolio durability without letting one decision create avoidable pressure elsewhere.

A simple rule of thumb

You likely need wealth management if several of these are true:

- Your wealth comes from more than one source: business equity, real estate, investments, stock compensation, trust interests.

- Your decisions affect other professionals: CPA, estate attorney, insurance specialist, business counsel.

- Your income is uneven or event-driven: sale proceeds, bonuses, contracts, carried interest, royalties.

- Your family considerations are complex: children, second marriages, aging parents, philanthropic goals, legacy planning.

If your life requires coordination, not just recommendations, wealth management starts to make sense.

How to Evaluate a Wealth Management Firm

Choosing a wealth manager is less about finding the firm with the best marketing and more about finding one that can think clearly across disciplines.

Start with the right questions:

- Are you acting as a fiduciary? You want a clear answer, not a vague one.

- Who are your typical clients? Experience with families like yours matters.

- How do you measure value beyond returns? Weak firms' shortcomings are often revealed here.

- How do you work with CPAs and estate attorneys? Coordination should be operational, not aspirational.

True value often comes from work beyond market performance. “Tax alpha” through strategies such as tax-loss harvesting can add 0.5% to 1.77% in annual returns, while behavioral coaching helps investors avoid emotional decisions that contribute to an average 5.5% underperformance gap, according to Bankrate’s summary of wealth manager value drivers.

Ask a prospective advisor to describe a recent client situation where the value came from taxes, behavior, estate coordination, or cash flow planning rather than security selection.

A practical next step is reviewing a firm’s process and fit criteria in resources like this guide on how to choose a wealth manager.

Frequently Asked Questions About Wealth Management

What’s the typical minimum to work with a wealth manager

It varies by firm. Many private wealth firms focus on clients with substantial complexity and often serve households with at least $500,000 in investable assets, which is a common threshold for more customized planning relationships.

Are wealth managers legally required to act in my best interest

Some are, some aren’t. You should ask directly whether the firm acts as a fiduciary and whether that standard applies to the relationship at all times. Don’t settle for assumptions. Get a clear explanation of how the firm is compensated and whether any conflicts exist.

Is wealth management only for retirees

No. Retirees are one important client group, but wealth management is just as relevant for business owners, executives, inherited wealth recipients, and sports or entertainment professionals with uneven income and compressed earning windows.

How is my financial information protected

A professional firm should use secure client portals, controlled access procedures, privacy policies, and compliance oversight. You don’t need a technical lecture. You do need a direct explanation of how documents are shared, who can access them, and what safeguards exist if a problem occurs.

Do I need to move everything to one firm

Not always. In some cases, consolidated oversight helps. In others, keeping certain relationships or structures in place makes sense. The important question is whether someone has a complete view of the financial picture and authority to coordinate decisions across it.

If you’re sorting through a liquidity event, concentrated holdings, retirement distributions, or the demands of family wealth, Commons Capital works with high-net-worth individuals, families, and specialized clients with complex planning needs. A good first conversation should leave you with more clarity about your options, your trade-offs, and whether a full wealth management relationship is the right fit.