High income doesn’t protect you from bad money architecture. It often hides it.

A Goldman Sachs report found that 40% of households earning $500,000+ annually still live paycheck to paycheck, largely because lifestyle inflation absorbs raises before they become wealth (Financial Aha). That should get your attention if you’re focused on combating lifestyle inflation 2026, because this isn’t a middle-market budgeting problem. It’s a wealth preservation problem.

If you earn well, own a business, work in sports or entertainment, or oversee family capital, the risk isn’t that you spend irresponsibly in obvious ways. The risk is that your financial life becomes structurally expensive. Better house. Better travel. Better schools. Better staff support. Better everything. Then one year you wake up and realize your income grew faster than your net worth.

That’s where many affluent households also run into money dysmorphia. You have real resources, but your fixed obligations and social environment make you feel financially constrained anyway. That feeling can push spending higher, not lower, because people often use visible upgrades to reassure themselves they’re doing well.

The High-Earner's Paradox in 2026

The affluent version of financial stress rarely looks chaotic from the outside. It looks polished. The home is beautiful. The calendar is full. Cash flow is tight.

That’s the paradox. A high earner can look wealthy, earn like a top performer, and still run a fragile personal balance sheet. If that sounds harsh, good. You should be hard on this issue because lifestyle inflation doesn’t announce itself with one reckless decision. It usually arrives as a series of upgrades that all seem justified.

Inflation isn't the same as lifestyle creep

You need to separate economic inflation from lifestyle creep.

Inflation means baseline costs rise around you. Lifestyle creep means you choose a more expensive standard of living as income rises. Those are not the same problem, and treating them as the same problem leads to bad decisions.

A lot of affluent households excuse every increase in spending as “things just cost more now.” Sometimes that’s true. Sometimes it’s camouflage for a larger home, more premium travel habits, more convenience spending, and a household cost structure that keeps expanding.

Practical rule: If your quality of life standard moved up with your income, that’s lifestyle inflation. If the same standard simply costs more, that’s inflation.

For younger wealthy clients who care about values as much as returns, Purpose Over Money: What HNW Millennials and Gen Z Really Want is a useful reminder that wealth decisions increasingly reflect identity, not just utility. That matters because identity spending is where creep gets expensive fast.

Why high earners are especially exposed

Affluent people face different pressure points than mass-market households. Your peers normalize expensive decisions. Your children’s environment normalizes them too. If your income is variable, you may mistake a strong year for a permanently higher baseline.

That’s why broad budgeting advice is often useless. “Cut coffee” doesn’t apply when the issue is whether your household gradually added layers of recurring obligations over the last few years.

A better lens is strategic cash-flow design. If your income is strong but your balance sheet feels less flexible than it should, revisit your planning assumptions for high-income earners. The question isn’t whether you make enough. The question is whether your system converts income into durable wealth.

Diagnosing the Creep Your Financial X-Ray

Most high earners don’t need another lecture about discipline. They need a clean diagnostic.

The right starting point is a fixed cost audit. For affluent households, that means reviewing spending across four categories: housing, health, basic transportation, and savings, then identifying subscriptions and monthly habits that need modification (Springfield Business Journal industry insight). If you skip this step, you’ll keep making decisions based on vibes, not evidence.

Start with fixed costs, not discretionary guilt

High-net-worth clients often focus first on visible luxury spending because it feels easier to cut. That’s backward.

Your real problem is usually in the recurring commitments that reset your “normal” every month. Mortgage or rent. Insurance stack. Tuition-style obligations. Concierge health arrangements. Auto leases. Household payroll. Club memberships. Platform subscriptions. Service retainers.

Use a detailed household checklist like this Ultimate List of Household Expenses for 2026 to catch expenses you’ve normalized and stopped questioning.

Here’s the audit framework I’d use:

- Housing: Review core shelter costs separately from prestige features. A primary residence is one thing. Renovation drift, second-home carry costs, and service layers around the property are another.

- Health: Keep essential coverage and care. Scrutinize convenience upgrades and add-on programs that became habitual without a clear purpose.

- Basic transportation: Distinguish mobility from image. Reliable transport is a need. Constantly upgrading the vehicle mix is usually a status choice.

- Savings: Treat this as a fixed cost, not leftover behavior. If savings isn’t listed alongside bills, spending will take its place.

Separate inflation from your own upgrades

Many individuals become careless in this situation.

If groceries cost more for the same basket, that’s inflation. If you switched from premium groceries to a more curated, artisanal, delivery-heavy setup, that’s your choice. If airfare rose, that’s inflation. If you decided economy no longer fits your brand, that’s creep.

Use this simple comparison:

Track changes by asking one question: “Did the same life get more expensive, or did we buy a more expensive life?”

What affluent households miss

Micro-upgrades create the biggest blind spot. Nobody panics over one more meal out, one more streaming service, one more convenience app, one more travel add-on, one more assistant-supported purchase decision. But enough of those moves and you’ve built a private tax on your future.

Your audit should end with three labels on every recurring line item:

- Essential and intentional

- Useful but negotiable

- Pure lifestyle drift

That last category is where wealth leakage hides.

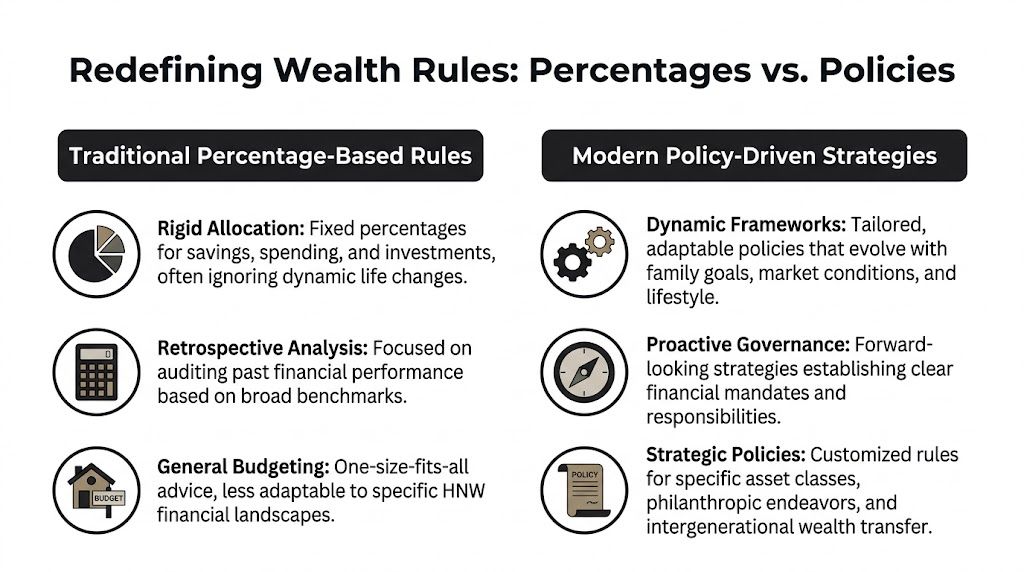

Redefining Your Wealth Rules From Percentages to Policies

The most overrated advice in personal finance is “save a fixed percentage.”

For high earners, that rule often preserves the problem instead of solving it. If you maintain a 25% savings rate, you automatically spend 75% of every income increase. That’s exactly why a fixed monthly spending limit is a stronger method. It stays constant when income rises and pushes surplus into savings by default (The Poor Swiss on avoiding lifestyle inflation).

Percentages feel disciplined. Policies are disciplined.

A percentage target sounds clever because it gives you a metric. But if your income rises sharply, a percentage system implicitly authorizes more spending every year.

That’s why affluent households need policies, not slogans.

A policy says:

- This household operates on a defined monthly lifestyle budget.

- Any income above that operating level gets routed elsewhere.

- Lifestyle upgrades require explicit review, not silent drift.

- Windfalls are handled under standing rules, not emotion.

That’s a governance system. It removes negotiation from every raise, bonus, distribution, or liquidity event.

What a spending policy actually looks like

A strong spending cap isn’t a punishment tool. It’s a decision filter.

For a household, the policy can cover:

You don’t need a perfect number on day one. You need a credible ceiling that reflects your actual values, not your latest impulse.

Here’s the key distinction. A budget asks, “How did we do?” A policy asks, “What are we allowed to become?”

Advisor view: Households that rely on willpower usually lose to convenience. Households that rely on policy usually keep more of what they earn.

Why this matters in combating lifestyle inflation 2026

In 2026, affluent households face two conflicting narratives. One says costs are high, so every spending increase is justified. The other says wealth solves the problem automatically. Both are lazy.

Ultimately, wealthy families need stricter rules precisely because they can afford to blur them. The larger your margin, the easier it is to miss the leak.

A fixed monthly spending policy also helps with money dysmorphia. When people feel vague financial pressure, they often react by either overspending for reassurance or under-enjoying wealth out of fear. A policy cuts through that confusion. It tells you what is safe to spend, what must be preserved, and what counts as excess.

Build rules your family can actually follow

If you’re married, have children, manage intergenerational assets, or support multiple households, informal agreements won’t hold. Put the rules in writing.

Use plain language such as:

- Operating lifestyle: Our family lives on a defined monthly amount.

- Windfalls: Bonuses, carried interest, business distributions, and signing payments follow a separate routing rule.

- Recurring upgrades: Any new monthly commitment gets reviewed before it becomes permanent.

- Annual reset: We review spending policy, not just investment performance.

That approach is far better than chasing a generic savings percentage and pretending that discipline will take care of the rest.

Tax and Investment-Aware Containment Strategies

Once you stop excess cash from leaking into lifestyle, you need to direct it somewhere useful. Otherwise the money will drift back into spending later.

Affluent planning should become mechanical. Not emotional. Not aspirational. Mechanical.

Build the path of least resistance

The smartest move is to route surplus cash automatically into vehicles that support your tax position, family goals, and investment plan. If the money hits your main spending account and sits there, you’ve already increased the odds it gets spent.

A clean implementation often includes:

- Retirement plan funding: Increase contributions through employer plans where available and appropriate.

- Brokerage automation: Set recurring transfers from operating cash to taxable investment accounts on a fixed schedule.

- Education and legacy structures: Direct funds to accounts or structures tied to family goals rather than ad hoc future promises.

- Reserve design: Keep a liquid buffer aligned with your spending obligations so you don’t turn every market downturn into a lifestyle problem.

The point isn’t complexity. The point is friction management. Your system should make investment easy and discretionary upgrading slightly annoying.

Match the destination to the source

Not all cash should go to the same place.

A salary increase might flow into retirement accounts, taxable investing, or cash reserves depending on your broader plan. A concentrated business distribution may require a different treatment because taxes, liquidity, and reinvestment risk are different. Deferred compensation, equity income, royalties, and licensing payments each create their own planning issues.

Generic financial content falls short. High earners need routing rules that fit the source of wealth, not one generic instruction to “save more.”

Here’s a practical framework:

Automate transfers as close to receipt as possible. Once money becomes visible lifestyle cash, it attracts uses.

Tax awareness matters because lifestyle inflation is tax-inefficient

Lifestyle upgrades are usually paid with after-tax dollars and then create recurring after-tax obligations. Investing, retirement funding, charitable planning, and entity-level coordination can produce a much better long-term outcome because they work with your financial structure instead of against it.

If your income is high and your tax picture is getting more layered, revisit a strategic framework for tax planning for high-income earners. The right tax strategy won’t fix spending drift by itself, but it gives your surplus somewhere smarter to go.

Keep liquidity from becoming an excuse

Affluent clients often say they want more flexibility, then keep too much discretionary cash floating in the wrong places. That usually leads to opportunistic spending, not better planning.

Liquidity should have a job. Investment accounts should have a job. Operating cash should have a job. Once every dollar has a role, lifestyle inflation loses one of its favorite hiding places.

Advanced Governance for Family Offices and Entertainers

Most advice on lifestyle creep assumes steady paychecks, private spending, and a simple household. That’s not how many affluent lives work.

For HNWIs, athletes, entertainers, and family offices, one of the biggest missed issues is the pressure of public image maintenance and irregular income streams, which generic middle-income advice doesn’t address (Good Day Extra on retirement pressure in 2026). If your earning pattern is uneven or your lifestyle is publicly observed, your spending decisions carry a different kind of pressure.

Family governance beats family tension

When wealth spans generations or supports multiple stakeholders, spending needs formal governance. Otherwise every cash-flow decision turns into a negotiation.

Good governance usually includes:

- Household operating policy: Define what the family pays for routinely and what sits outside that lane.

- Approval thresholds: Set rules for large commitments, ongoing support, and new recurring expenses.

- Windfall protocol: Decide in advance how business exits, major contracts, or one-time payments are treated.

- Meeting cadence: Review spending decisions with the same seriousness as investment policy.

If you manage significant family complexity, family office structures can help centralize these decisions more effectively than informal discussion ever will. At this juncture, family office services become less about prestige and more about control.

Entertainers and athletes need a different operating model

Variable earners should never build lifestyle around their best year.

A better model is to create two systems:

- A personal payroll system that transfers a stable amount to your lifestyle account.

- A surplus management system that holds, taxes, and allocates the rest according to standing rules.

That matters because career arcs can be short, nonlinear, and exposed to forces outside your control. If your spending grows around peak income, the comedown can be brutal even when total lifetime earnings were substantial.

Public success can create private spending obligations that were never economically necessary.

Managing money dysmorphia in wealth management

Money dysmorphia doesn’t mean someone is irrational. It means their perception of financial security is distorted by context.

Among affluent clients, it often shows up like this:

- You feel behind because your peer group spends more.

- You feel poor because your fixed costs are large, even though your net worth is strong.

- You resist enjoying wealth because you don’t trust what’s actually safe.

- You overspend to maintain an identity that no longer serves you.

The fix isn’t motivational talk. It’s clarity.

A useful family or personal review should answer four questions:

Once those answers are written down, the emotional noise drops. You stop treating wealth like a feeling and start treating it like a governed system.

Your Blueprint for Sustainable Wealth

Combating lifestyle inflation 2026 isn’t about acting smaller. It’s about acting sharper.

The households that preserve wealth over time don’t rely on income alone. They use structure. They audit fixed costs. They separate actual inflation from self-created lifestyle expansion. They replace generic savings percentages with hard spending policies. Then they automate the flow of surplus into investments, reserves, and long-term family priorities.

That’s the fundamental shift. Stop asking whether you’re earning enough. Start asking whether your financial system is converting success into resilience.

If your household, business, or family office has gotten more expensive without becoming more secure, fix the architecture. Not next year. Now.

Frequently Asked Questions

If you want help building a spending policy, tax-aware cash-flow system, or family governance structure that protects long-term wealth, Commons Capital works with high-net-worth individuals, families, entertainers, and family offices to bring discipline to complex financial lives.