When you start looking for a "fiduciary financial advisor near me," you’re taking what might be the single most important step in protecting your financial future. The word fiduciary isn't just jargon — it means your advisor is legally and ethically required to act in your best interest. For anyone with significant assets, this standard is non-negotiable. It's what separates real advice from a sales pitch.

Why Your Search for a Fiduciary Advisor Matters

Finding the right person is about much more than a quick Google search. This decision can genuinely shape your family's wealth for generations. The stakes are even higher for high-net-worth individuals and professionals in demanding fields like sports or entertainment. Your finances aren't just a portfolio; they're a complex web of tax strategies, estate planning, and legacy building.

A generic financial advisor might offer advice that is merely "suitable," but there's a world of difference between suitable and optimal. A true fiduciary, especially one who specializes in clients with $500k+ in investable assets, operates on another level entirely. Think of them as your financial quarterback, coordinating with your attorneys and accountants to execute a single, unified game plan.

The Fiduciary Standard Is Your Shield

That legal duty to put your interests first isn’t just a nice-to-have; it's a powerful shield against bad advice. Many so-called "advisors" are really just salespeople, paid commissions to push certain products. A fiduciary’s success, on the other hand, is tied directly to yours. Their advice is meant to grow your wealth, not their own pockets.

The Employee Retirement Income Security Act (ERISA) of 1974 was a landmark law that established this strict fiduciary duty, holding advisors personally liable for putting their clients' interests first. This ensures recommendations are based on what's best for you, not what pays the highest commission.

Moving Beyond a Basic Local Search

This guide is built to get you past that initial search query. We're going to give you a clear roadmap to properly vet potential advisors so you can find a real partner — someone who gets the unique challenges and opportunities that come with managing substantial wealth.

We’ll walk through the specific steps you need to take.

- Verify Credentials: Learn exactly how to check an advisor’s background and professional designations like CFP® or CFA.

- Interpret Key Documents: We’ll show you how to read a Form ADV to uncover an advisor’s fee structure, services, and any hidden disciplinary history.

- Ask Insightful Questions: Go into your first meeting ready with questions that cut through the sales pitch and reveal an advisor’s true philosophy.

It's also worth noting the difference between a fiduciary and a fee-only advisor, which can be subtle but critical. You can learn more in our guide on the distinctions between fiduciary financial advisors and fee-only models. Getting this process right ensures you end up with an expert who can confidently manage your complex financial world.

Mastering Your Local Advisor Search in 2026

Simply typing "fiduciary financial advisor near me" into Google is just the first step. You’ll get results, but they’re often dominated by firms with the biggest marketing budgets, not necessarily the ones with the right expertise for you.

Finding a true partner requires digging a bit deeper. With the Bureau of Labor Statistics projecting over 326,000 financial advisor roles by 2026, the options are overwhelming. For high-net-worth individuals, this means you have plenty of choices, but finding the right one demands a more strategic approach.

That sheer volume is exactly why a targeted search is so critical.

Smarter Search Queries for Better Results

You need to get specific. Think about what makes your financial life unique and weave those details into your search. This is how you cut through the marketing fluff and find specialists who are already solving problems just like yours.

Instead of a generic query, try something more pointed:

- "Fee-only RIA for business owners in [Your City]": This immediately filters for Registered Investment Advisors who are transparent with their fees and understand the unique headaches of owning a business.

- "Wealth management for concentrated stock positions near [Your Zip Code]": Perfect for tech executives or early employees, this finds advisors skilled in diversification and managing single-stock risk.

- "CFP fiduciary for athletes in [Your State]": This pinpoints Certified Financial Planners who are legally bound to act in your best interest and specialize in the unique career spans and income patterns of professional athletes.

These specific searches force Google’s algorithm to work for you, delivering more relevant, niche advisors who truly get it.

Leveraging Professional Directories

While Google is a powerful starting point, it shouldn't be your only tool. Industry directories are goldmines for finding pre-vetted fiduciaries. These organizations have strict membership rules, essentially doing the first round of screening for you.

A quick tip for your Google search: Pay attention to the sponsored ads at the top. While those firms aren't necessarily bad, the organic results below are earned through relevance and authority — often a better signal of a good match.

Two of the most trusted directories are:

- The National Association of Personal Financial Advisors (NAPFA): Every single advisor on NAPFA’s "Find an Advisor" platform is a fee-only fiduciary. It’s a non-negotiable requirement for membership, making it the gold standard.

- The CFP Board: The board’s "Find a CFP® Professional" tool lets you locate Certified Financial Planner™ professionals. You can filter by how they’re paid, so you can zero in on those who are fee-only and avoid conflicts of interest.

Using these sites gives you a high-quality list of candidates who have already demonstrated a commitment to a higher standard of care.

A Real-World Search Scenario

Let's put this into practice. Imagine a tech executive in Seattle who just had a liquidity event, leaving her with $10 million in cash and company stock. A generic search would be a firehose of information.

Here’s how a smarter approach works:

First, she starts with a highly specific search: "Fiduciary advisor for tech executive post-IPO Seattle."

She skips the paid ads and analyzes the organic results, looking for firm websites that specifically mention "concentrated stock," "tax planning for equity compensation," and "sudden wealth."

With a shortlist of three promising firms, she then heads to the NAPFA directory to cross-reference them, confirming they are all listed as fee-only members.

Finally, she notices one firm’s blog is full of case studies on managing stock options and Qualified Small Business Stock (QSBS). This is a clear signal of deep, relevant expertise. In just a few targeted steps, she’s narrowed a field of hundreds down to one or two truly qualified candidates.

This thorough process isn't just for finance. The principles of a disciplined local search apply to finding any top-tier specialist, as shown in this guide to finding local professionals.

Alright, you’ve pulled together a shortlist of potential financial advisors. The marketing materials look great, and they all sounded promising on the phone. Now for the most important part: the background check.

This is where you cut through the sales pitch. You need to verify, with objective proof, that an advisor is who they claim to be. It’s not about being cynical; it’s about being smart. You're looking for concrete evidence of their qualifications, their legal obligations, and any skeletons that might be hiding in their closet.

Your Go-To Tool: The SEC's IAPD Database

Your first and most crucial stop is the Investment Adviser Public Disclosure (IAPD) website. This database is run by the U.S. Securities and Exchange Commission (SEC), and it's a goldmine of information. Every Registered Investment Advisor (RIA) and their individual reps are required to file public documents here.

Simply search for an advisor or their firm by name. The IAPD portal grants you access to their full regulatory history, from past jobs and certifications to, most critically, any disciplinary actions or customer complaints. It’s all there in black and white.

Don't be intimidated by the government-website look. This simple search box is your best friend for due diligence.

Decoding the Form ADV: Where the Secrets Live

Once you're on the IAPD site, the document you want is the Form ADV. This is a mandatory filing for all RIAs, and it's packed with the details you need to know. If an advisor seems reluctant to share their Form ADV or point you to it, that’s a massive red flag. Run, don't walk.

The form is long, but you can zero in on Form ADV Part 2, often called the "brochure." It's written in plain English for a reason — so clients like you can understand it.

Here’s what to look for:

- The Fiduciary Statement: Is there a clear, unambiguous sentence stating they have a fiduciary duty to their clients? It should be right there. Vague or watered-down language is a bad sign.

- Fees and Compensation: This section is non-negotiable. The form must spell out exactly how they make money. Are they strictly fee-only, or do they also earn commissions by selling you specific products? This is where potential conflicts of interest come to light.

- Disciplinary History: Pay close attention to Item 9. It requires the firm to disclose any regulatory, civil, or criminal events. You absolutely want to know if there's anything listed here.

- Services and Expertise: The firm outlines the services it provides. This is a great way to confirm they actually have experience helping people in your specific financial situation.

Keep in mind, the term "fiduciary" has real teeth. The legal standard, rooted in The Employee Retirement Income Security Act of 1974 (ERISA), establishes that fiduciaries can be held personally liable for losses if they breach their duties. That’s a powerful layer of accountability you want on your side.

Verifying Professional Designations

After the Form ADV, it’s time to check those fancy letters after the advisor's name. An alphabet soup of credentials can look impressive, but only a few signify a high level of expertise and a strict code of ethics.

Don't just take their word for it — verify them independently.

- Certified Financial Planner (CFP®): This is one of the most recognized and respected credentials in financial planning. You can easily confirm someone's CFP® status and check their public disciplinary record using the CFP Board's verification tool.

- Chartered Financial Analyst (CFA®): A globally prestigious designation, the CFA charter indicates deep expertise in investment management and portfolio analysis. Use the CFA Institute member directory to confirm an individual is a charterholder in good standing.

Confirming these credentials ensures the advisor didn't just attend a weekend seminar but has met rigorous educational, ethical, and experience requirements. This isn't just busywork; it's a critical step in the selection process, which we cover more in our guide on what to look for in a financial advisor. Taking a few minutes to verify these details gives you the confidence that you’re partnering with a true professional.

The Advisor Interview Questions You Must Ask

That first meeting with a potential advisor isn't a sales pitch. It's an interview — and you're the one conducting it.

For high-net-worth clients, this conversation has little to do with stock market predictions. It’s about digging into an advisor’s core philosophy, their operational integrity, and whether they can truly handle financial complexity. You're trying to move past the surface and see how they actually think.

A good set of questions turns a gut feeling into a data-driven choice, letting you compare candidates objectively. This is just as critical as the verification process itself.

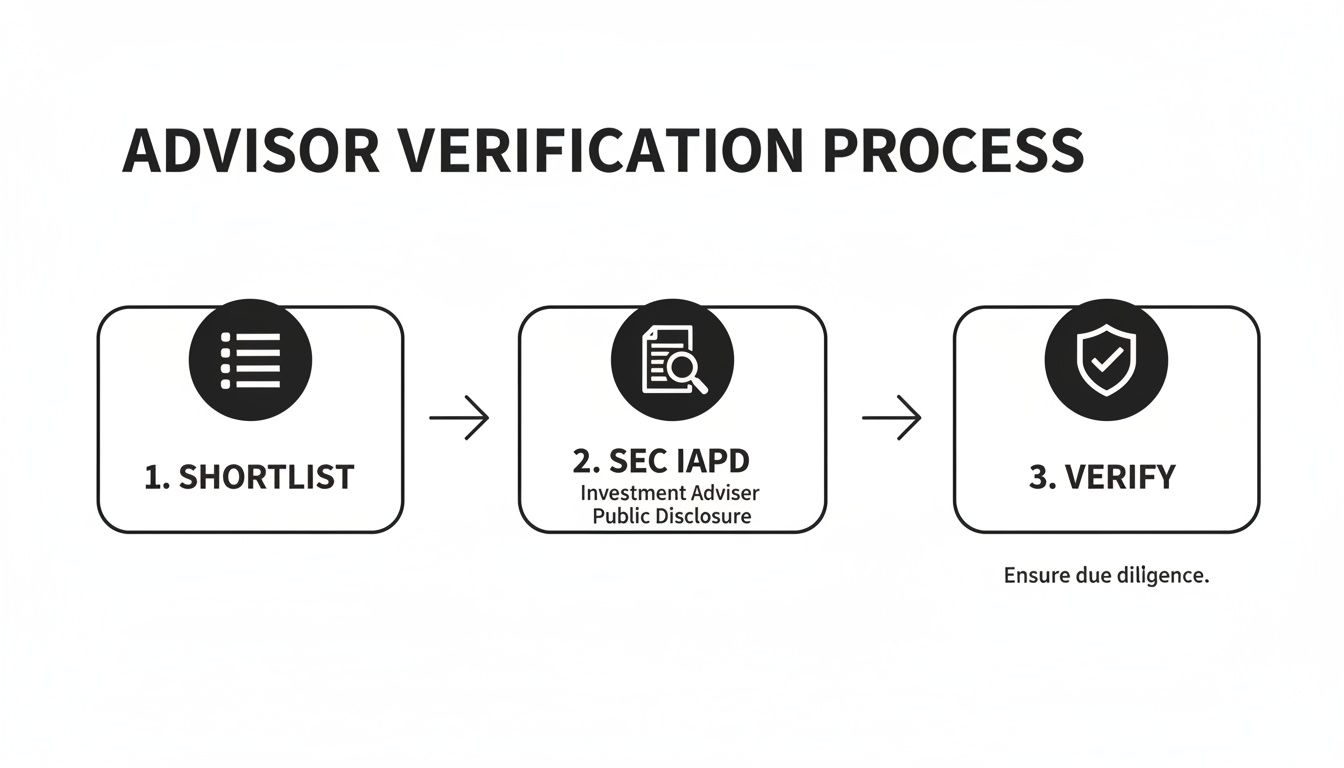

Before you even schedule a meeting, your vetting process should look something like this.

This simple flow — shortlist, investigate on the SEC’s IAPD database, then verify credentials — makes sure you’re only spending time with pre-qualified fiduciaries.

How They Think: Philosophy and Experience

Start by getting to the "why" behind their practice. These questions reveal their investment beliefs and whether their background lines up with your specific, often complicated, needs.

- “Describe your ideal client. What kinds of financial situations are you best at handling?” This is a great way to find out if you fit their specialty or if you'd be an outlier in their book of business.

- “How have you helped a client through a sudden wealth event, like a business sale or large inheritance?” Their answer will show you their process for managing large, complex capital inflows and the tax and planning headaches that come with them.

- “Walk me through your investment philosophy. Do you use active management, passive strategies, or a mix? And why?” There isn’t one right answer here. What you’re listening for is the reasoning to see if it matches your own risk tolerance and long-term goals.

An advisor's philosophy is their strategic compass. A clear, consistent philosophy is a strong indicator of a disciplined professional who won't be swayed by market noise or the latest investment fads.

How They Operate: Client Service and Coordination

For anyone with significant assets, an advisor needs to be more than an investment manager; they need to be a financial quarterback. They must work smoothly with the other professionals you trust.

- “What’s your process for coordinating with my existing legal and tax team?” A top-tier advisor will have a clear, defined process for this. A vague promise to “work with them” isn’t good enough.

- “Who will be my main point of contact, and what’s your firm’s typical response time?” This sets clear expectations from day one about communication and service.

- “How many clients does each advisor here serve?” A lower client-to-advisor ratio often means more personal attention, which is critical when your financial life has a lot of moving parts.

How They Get Paid: Fees, Conflicts, and Fiduciary Duty

Full transparency around compensation is the absolute bedrock of a fiduciary relationship. These questions leave zero room for ambiguity and help you spot potential conflicts of interest before they become a problem.

The table below breaks down the common fee structures you'll encounter and what they really mean for you.

Advisor Fee Structure Comparison

As you can see, the differences are stark. A fee-only structure is almost always the cleanest, most transparent model for a fiduciary relationship. Here are the direct questions to get the answers you need:

- “Are you a full-time fiduciary, legally obligated to act in my best interest on all matters?” The only acceptable answer is a direct and simple "yes."

- “Can you show me in your Form ADV Part 2 where you disclose your fiduciary duty and all your sources of compensation?” Don't just take their word for it. Make them prove it in writing.

- “How, exactly, are you compensated? Is it AUM fees, flat retainers, hourly rates, or commissions?” A true fiduciary advisor near you will have no problem clearly explaining their fee structure and its value.

- “Besides your main advisory fee, are there any other costs I should know about? Think trading fees, administrative costs, or expense ratios on the funds you use.” This helps you uncover the true "all-in" cost of working with them.

For a more exhaustive list to help you vet potential advisors, check out our guide covering more questions to ask a wealth manager. Asking these tough questions upfront is the only way to build a partnership based on complete trust and transparency.

Advanced Services High-Net-Worth Clients Need

When your financial life gets complicated, "off-the-shelf" investment advice just won't cut it. High-net-worth individuals and families need a caliber of service that goes well beyond basic portfolio management. This is where an elite fiduciary financial advisor proves their worth, stepping in to act as a personal CFO for your entire financial world.

It’s not just about growing your assets. It’s about protecting them, making them tax-efficient, and making sure they’re set up to support your family for generations. A top-tier advisor brings together services that tackle challenges you haven't even considered yet.

Integrated Wealth and Tax Strategy

For wealthy clients, taxes aren't a once-a-year headache; they're a constant drag on your wealth if you’re not planning ahead. A premier fiduciary advisor doesn’t just ask for your tax return in April. They build a forward-looking strategy designed to minimize what you owe.

This isn’t basic tax prep. It involves a number of sophisticated techniques:

- Tax-Loss Harvesting: This is the practice of systematically selling investments at a loss to offset gains you’ve realized elsewhere in your portfolio. It’s a simple concept that can add significant value over time.

- Asset Location: It’s not just what you own, but where you own it. A good advisor will strategically place different investments in the most tax-friendly accounts — think high-growth assets in a Roth IRA and income-producing bonds in tax-deferred accounts.

- Charitable Giving Structures: You can achieve your philanthropic goals and get a substantial tax deduction at the same time. This is done using tools like Donor-Advised Funds (DAFs) or Charitable Remainder Trusts (CRTs).

The goal is to ensure every financial decision is viewed through a tax-aware lens. This proactive coordination between investment management and tax planning is a hallmark of true wealth management.

Multi-Generational Estate and Legacy Planning

An experienced fiduciary gets that your wealth is about more than just you. It's about securing your family’s future and leaving a lasting legacy. While standard estate planning might end with a simple will, high-net-worth planning is a much more complex field.

This process means working hand-in-hand with estate planning attorneys to structure your wealth in a way that reflects your values and protects your heirs from future headaches.

- Trust Services: Advisors can help establish various trusts, like Revocable Living Trusts or Irrevocable Life Insurance Trusts. These tools control how your assets are passed on, protect them from creditors, and can seriously minimize estate taxes.

- Succession Planning: If you're a business owner, this is critical. It involves creating a clear roadmap for passing the company to the next generation or setting it up for a strategic sale.

- Family Governance: A good advisor can help your family create a mission statement and a framework for making financial decisions together. The aim is to make sure wealth brings the family together, instead of tearing it apart.

Specialized Scenarios for Unique Clients

No two financial stories are the same, particularly when you reach the highest levels of success. A versatile fiduciary has seen it all and knows how to handle the unique hurdles faced by clients with unconventional careers or complex finances.

Real-World Scenarios:

- The Professional Athlete: An advisor’s job here is to manage a massive, but short-lived, income stream. They have to plan for a 40-plus-year "retirement" that starts long before the traditional age, which means looking at disability insurance, disciplined budgeting, and long-term investment plans.

- The Family Office: In this case, a fiduciary often acts as an outsourced Chief Investment Officer (CIO). They help the family structure its charity, vet private equity deals, and manage a complicated mix of public and private assets.

- The Tech Founder: After a successful exit, an advisor steps in to help the founder preserve their newfound wealth. This involves strategies for dealing with a large amount of company stock, planning around Qualified Small Business Stock (QSBS), and building a diversified portfolio to fund their life and next big idea.

Understanding the principles behind various investment vehicles, such as mutual funds, can provide valuable context for the financial strategies a fiduciary advisor employs. You can explore the history of mutual fund management to appreciate how these concepts have evolved. This deep knowledge is what allows an advisor to build a truly robust financial plan.

Common Questions on Finding a Fiduciary Advisor

Even after you've mapped out your search, a few key questions always seem to pop up. The financial world is murky, filled with jargon and fine print. Let's clear the air and tackle the most common questions we hear from high-net-worth individuals looking for a truly trustworthy advisor.

What's the Real Difference Between a Fiduciary and a Financial Advisor?

This is the most critical distinction you need to understand. A fiduciary financial advisor has a legal and ethical duty to put your best interests first, period. The advice they give has to be the absolute best option for you, not just something that’s “suitable.”

Many other financial professionals operate under a lower "suitability" standard. This allows them to recommend a product that might be appropriate, but could also earn them a fat commission when a better, lower-cost option exists. For anyone with significant assets, the fiduciary standard isn't just a preference — it's the only standard that makes sense.

How Much Does a Top Fiduciary Financial Advisor Cost?

Any true fiduciary will be an open book about their fees. Most use a fee structure based on a percentage of Assets Under Management (AUM), which you'll see clearly disclosed in their Form ADV. This typically starts around 1% per year and often gets lower as your portfolio grows larger.

You might also run into a couple of other fee models:

- Flat Annual Retainers: A set fee you pay each year for all-inclusive planning and investment management.

- Hourly Fees: This is more common for one-off projects, like building a foundational financial plan.

The model doesn't matter as much as the transparency. There should never be any hidden fees or surprises.

It’s easy to get hung up on cost, but value is what you should really be focused on. An expert who steers you clear of one expensive mistake or uncovers a sophisticated tax strategy can provide a return that dwarfs their annual fee.

Is a Local Advisor Really Better Than a National Firm?

When people search for a "fiduciary financial advisor near me," they often wonder if a local pro is better than a big national brand. While video calls have made the world smaller, a local advisor can offer some real, tangible benefits, especially when your financial picture is complex.

A local expert gives you face-to-face accountability. More importantly, they’re plugged into the community, with a network of other top-tier local professionals like the best estate planning attorneys or CPAs in your city. While the advisor’s specific skills and your personal chemistry are what matter most, many clients feel the high-touch service from a dedicated local firm is simply unmatched.

What Are the Biggest Red Flags When Hiring an Advisor?

Catching red flags early can save you a world of financial pain and stress. Keep your eyes peeled for these warning signs as you interview potential advisors:

- Refusal to Share Their Form ADV: This is a non-starter. If they won't provide it immediately, end the conversation and walk away.

- A History of Disciplinary Actions: A clean record isn't too much to ask. Always check their background on the SEC's IAPD website and FINRA's BrokerCheck.

- Pressure to Buy Specific Products: Fiduciaries advise; salespeople sell. If you feel a hard pitch for high-commission products like annuities or niche insurance policies, it’s a huge red flag.

- Vague or Confusing Fee Explanations: If they can't explain exactly how they get paid in simple terms, it's because they don't want you to know. There's a conflict of interest hiding in the complexity.

- Promises of Guaranteed High Returns: This is the oldest trick in the book. It's also impossible and unethical. No one can predict the markets, and any advisor who claims they can't be trusted.

A great advisory relationship is built on a foundation of absolute transparency and trust. You should feel like you have a true partner focused entirely on your long-term success.

At Commons Capital, upholding the highest fiduciary standard isn't just a legal requirement — it's the core of how we operate. If you're looking for a wealth management firm that puts your interests first, visit us at https://www.commonsllc.com to see how we can help you reach your goals.