Cash still feels safe. That’s why many high-net-worth investors are sitting in short Treasuries, money markets, CDs, and sweep accounts even as the rate backdrop changes. The problem isn’t credit risk. It’s reinvestment risk.

Locking in bond yields before 2026 rate cuts is really about one decision. Do you keep waiting in cash while policy rates move lower, or do you extend into high-quality fixed income while yields are still attractive enough to matter? For affluent families, business owners, and clients with irregular income, that decision affects not just portfolio income, but taxes, liquidity, and how much flexibility you preserve for the next twelve to eighteen months.

The Closing Window for High Yields in 2026

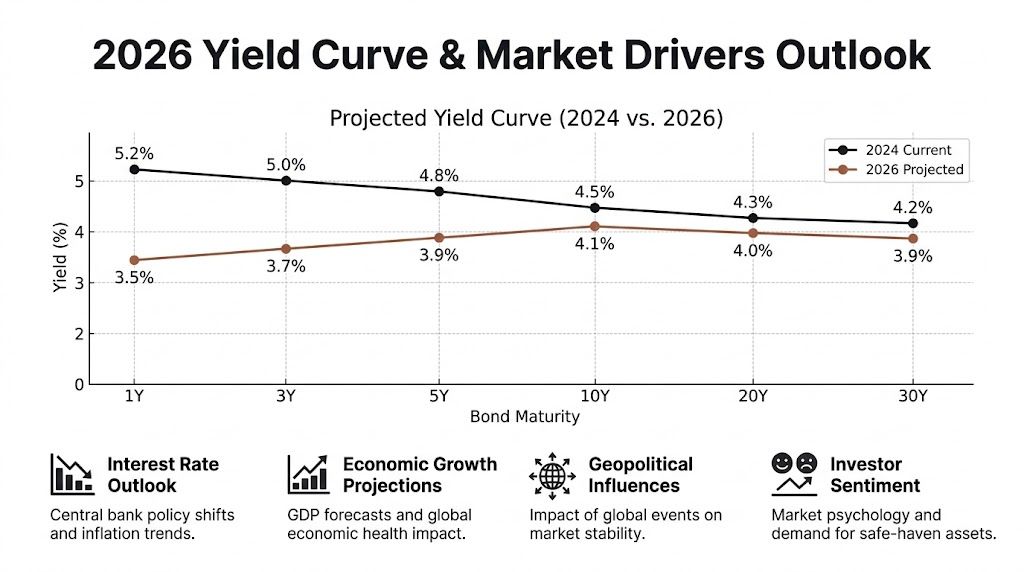

The easy part of the bond trade already happened. In 2025, the Federal Reserve made three rate cuts, which helped bond returns through a combination of high starting yields and price appreciation, while the 10-year Treasury moved down into roughly the 3.75% to 4% area entering 2026 and the Fed is projected to make only one or two additional cuts in 2026 with long-term yields stabilizing near 4%, according to Schwab’s 2026 bond market outlook.

That matters because today’s opportunity is narrower. You can still lock in yields that look attractive relative to the policy rate expected later in the cycle, but you shouldn’t expect a replay of the broad bond tailwind investors enjoyed when yields started from higher levels.

Clients usually come into this moment with one of two concerns. They either don’t want to lose the yield they’re earning on cash, or they don’t want to buy bonds just before inflation pushes rates back up. Both concerns are reasonable. Neither justifies doing nothing.

Why waiting can cost more than a modest extension

If the Fed keeps easing, cash yields reset quickly. Intermediate bonds don’t. That’s the core appeal of extending cash maturities in a falling rate environment. You’re not trying to make a heroic duration call. You’re trying to preserve income before the front end reprices lower.

A lot of investors learned the opposite lesson in the rising-rate phase and became conditioned to stay short. That instinct helped when yields were moving up. It can become expensive when they’re moving down.

Practical rule: When a rate-cut cycle is already underway, cash stops being a strategy and starts being a countdown.

The better frame is selective extension. Not maximum duration. Not aggressive credit. Just enough maturity to secure income without making the portfolio hostage to the long end of the curve.

That’s also why old advice built for rising rates doesn’t map cleanly onto today’s setup. If you want context on the prior regime, investment strategy for rising interest rates is useful as a contrast. The mechanics are different now. In early 2026, the question isn’t how to avoid duration. It’s how to own the right amount of it before rates settle lower.

Decoding the 2026 Yield Curve and Market Drivers

The yield curve is doing the talking. Short rates are under pressure from expected Fed easing, while longer rates aren’t following nearly as fast. That’s why broad “rates are falling, buy long bonds” advice misses the point.

Schwab’s fixed income outlook projects the Fed will cut two to three times from the current 3.50% to 3.75% federal funds range, aiming for a neutral rate near 3% by year-end 2026, while the 10-year Treasury is unlikely to fall below 3.75% and could rise to 4.5%, with longer yields expected to remain range-bound at 4.00% to 4.50% because of resilient growth, ongoing inflation pressure, and rising bond supply from fiscal deficits and other issuance, as outlined in Schwab’s fixed income outlook.

Why the curve is steepening

A steepening curve in this environment doesn’t mean the economy is collapsing. It means the market sees a difference between where overnight policy is heading and where longer-term inflation and funding pressures may settle.

Three forces matter most:

- Fed cuts hit the front end first. T-bills, short notes, and cash-like vehicles reprice quickly when policy rates move down.

- Inflation hasn’t fully disappeared. If inflation stays sticky, investors demand more compensation to lend longer.

- Treasury supply stays heavy. When the government needs to issue more debt, long-dated yields don’t always fall just because the Fed is easing.

That combination is why the long end can remain stubborn even in a cutting cycle.

What works better than a simple long-duration bet

This is the part many investors get wrong. They assume lower policy rates automatically justify loading up on long bonds. But if the 10-year holds in a range and supply remains heavy, extending too far can create volatility without enough extra compensation.

The more durable setup is usually in the intermediate part of the market. It gives you meaningful carry, some price upside if yields drift lower, and less exposure to long-end shocks.

A useful cross-market reminder comes from recent commentary on sovereign bonds. Even outside the U.S., bond markets are responding to the same basic tension: inflation risk may cool, but supply, fiscal policy, and investor demand still shape longer-term yields.

Long bonds can still work. They just need the market to cooperate more precisely than intermediate bonds do.

How to read this as a portfolio decision

Here’s the practical interpretation.

For most HNW portfolios, this isn’t a forecasting contest. It’s a structure problem. The portfolio should be built so that if cuts arrive as expected, income is preserved. If long yields stay sticky, volatility remains tolerable.

Executing Core Strategies to Secure Income

Most investors don’t need a complicated fixed-income playbook. They need a repeatable process. In this market, two approaches do most of the heavy lifting: bond laddering and duration extension.

Bond laddering for investors who want control

A ladder works well when liquidity matters and you don’t want to make a single-rate bet. The basic structure is straightforward. You spread capital across staggered maturities, often with equal weights, and keep rolling maturing proceeds forward.

According to Columbia Threadneedle’s fixed income outlook, investors can build a ladder across maturities such as 1 to 10 years, with an emphasis on the 3 to 7 year part of the curve. In prior cutting cycles such as 2019 to 2020, that approach outperformed cash by 100 to 200 basis points annualized, while over-extending duration beyond 7 years raised the risk of significant volatility, including the -16% drawdown for long bonds in 2022.

That framework is useful because it solves several problems at once.

- Income gets locked in across time. You avoid putting all the money into one maturity on one day.

- Liquidity remains scheduled. Bonds mature naturally, which is useful for taxes, spending needs, and opportunistic reallocation.

- Reinvestment becomes disciplined. Each maturity gives you a built-in decision point rather than forcing an all-or-nothing move.

A workable ladder design

For affluent households, I usually think of the ladder in buckets, not in perfectly even annual slices. The point is functionality, not elegance.

- Short bucket: Handles known spending, taxes, and near-term liquidity.

- Intermediate bucket: Effectively locks in yield.

- Outer bucket: Adds some duration, but only if the investor can tolerate interim price swings.

If you prefer to compare implementation trade-offs before deciding between separate CUSIPs and pooled vehicles, bond fund versus individual bonds is a helpful framework.

Desk rule: A ladder should reduce decision stress. If it creates more monitoring and second-guessing than your client can live with, it’s too complicated.

Duration extension for investors overloaded in cash

Duration extension is a different tool. Instead of spreading maturities broadly, you deliberately move part of the portfolio from very short instruments into intermediate Treasuries or investment-grade bonds. This is often the cleaner solution for investors who built large cash positions during the hiking cycle.

The case for it is simple. If rates move down, short-rate income falls quickly. Intermediate bonds keep paying the coupon you locked in, and they may also benefit from price appreciation if yields decline.

What doesn’t work is doing this all at once with no scenario planning. A measured shift is usually better than a dramatic one because it lowers regret risk if the market gets choppy.

Common mistakes that hurt results

The mistakes are usually behavioral, not mathematical.

- Chasing the longest yield on the screen. A slightly higher nominal yield can come with materially higher duration risk.

- Reaching for credit because cash looks less attractive. Lower policy rates don’t eliminate spread risk.

- Selling on normal volatility. A ladder or intermediate-duration allocation only works if you let the structure do its job.

- Ignoring taxes and account location. Taxable bonds in the wrong account can make a decent idea much less compelling after tax.

Municipal bonds often deserve a dedicated lane in this conversation. If you’re evaluating whether they belong in the quality-income sleeve, municipal bonds as an investment option is worth reviewing alongside Treasury and corporate choices.

Choosing Optimal Fixed-Income Instruments

A client sells a business in late 2025, moves proceeds into taxable accounts, and wants dependable income before policy rates fall. The wrong bond mix can leave that family with lower after-tax cash flow, more reinvestment risk, and fewer options for trusts or gifting strategies. The right mix does the opposite.

Treasuries, corporates, munis, and agency mortgages

Instrument selection shapes outcomes just as much as duration. Two portfolios can carry similar interest-rate sensitivity and produce very different results after taxes, fees, and liquidity frictions.

For high-net-worth investors, the practical menu usually comes down to four categories.

The label matters less than the job each bond is doing. Treasuries are the cleanest way to express a duration view and preserve liquidity. Investment-grade corporates can add carry, but only with disciplined issuer selection and position sizing. Agency mortgage-backed securities can help diversify rate exposure, though prepayment behavior makes them better suited to professionally managed sleeves than casual bond picking. Municipal bonds often stand out once the decision is framed in after-tax terms rather than nominal yield.

Why municipals deserve serious attention

For top-bracket investors, municipal analysis should begin with tax-equivalent yield and state tax exposure. A tax-exempt bond with a lower headline coupon can still produce more spendable income than a taxable Treasury or corporate bond. That is especially true for investors in high-tax states, families with uneven annual income, and households managing concentrated liquidity events.

This is not just a tax discussion. It is a cash-flow and balance-sheet discussion.

Athletes, founders, private equity partners, and executives with stock-based compensation often face irregular income and shifting marginal tax rates. A well-built municipal ladder can steady portfolio cash flow while reducing the drag from federal, and sometimes state, taxes. For families reviewing broader planning options, 10 Advanced Tax Strategies for High Net Worth Individuals in 2026 is a useful companion to bond allocation work.

Compare munis to taxable bonds on what you keep, not on the coupon printed on the screen.

A decision lens that works in practice

I use five filters when selecting fixed-income instruments for taxable wealth.

- After-tax income: Start with the cash the client retains, not the nominal yield.

- Structure risk: Call provisions, sinking funds, and premium pricing can change the return profile materially.

- Liquidity: Some bonds are easy to sell in size. Others are not, especially in stressed markets.

- Credit resilience: Higher yield is only useful if the issuer can carry the debt through a weaker economy.

- Portfolio role: A bond can be an income tool, a duration hedge, collateral for borrowing, or part of an estate-planning structure.

Implementation matters here. Investors who want defined maturities and known cash flows often prefer individual bonds, while those who prioritize broad diversification and daily liquidity may prefer pooled vehicles. This comparison of bond funds versus individual bonds is a useful framework for deciding which structure fits the mandate.

Estate planning angle

Bond selection also affects how wealth moves across generations. In larger family balance sheets, the fixed-income sleeve often sits inside revocable trusts, irrevocable trusts, donor-advised strategies, and entities with different tax treatment. That changes what "best bond" means.

Municipal bonds can fit well where the objective is tax-aware income for beneficiaries or cleaner cash-flow matching inside trust accounts. Treasuries may be better where liquidity, collateral quality, or simplicity matters more than after-tax yield. Corporate bonds can make sense in entities less sensitive to personal tax rates, but spread risk should be sized carefully if those assets support distributions or estate obligations.

Good bond selection is rarely a standalone trade. It is part of a broader plan that includes taxes, account location, trust design, and liquidity needs. That is the standard high-net-worth investors should expect.

Leveraging Advanced Tactics for Enhanced Returns

Some investors need more than spot bond purchases. Family offices, taxable institutions, and advanced HNW clients often want to adjust duration or hedge rate risk without disturbing the whole bond book. That’s where derivatives become useful.

Treasury futures for efficient duration changes

The bond math matters. As explained in Bankrate’s discussion of lower rates and bond investors, bond prices generally rise when yields fall, often summarized as ΔPrice ≈ -Duration × ΔYield. A 6-year duration bond could gain roughly 6% in price if yields fall by 100 basis points. The same source notes that investors can use Treasury futures to create that duration exposure with greater capital efficiency, while also using derivatives to hedge if yields rebound toward 4.5%.

In practice, that means a manager can increase rate sensitivity without immediately buying a large block of cash bonds. That can be valuable when the portfolio has embedded gains, tax constraints, or liquidity demands.

Swaps and overlays for targeted outcomes

Interest rate swaps can also help. A floating-rate exposure can be converted into a more fixed-like cash flow profile, which is one way to lock in income characteristics without rebuilding every underlying holding. For some investors, options overlays may also make sense as a hedge against a rate backup.

These tools are useful for three reasons:

- They isolate the rate view. You can alter duration without changing every security.

- They preserve flexibility. Futures and swaps can usually be adjusted faster than a fully restructured cash portfolio.

- They can hedge existing exposures. That matters if a portfolio already has concentrated bond or liability-matching positions.

What tends to go wrong

The biggest mistake is using derivatives as a substitute for asset allocation discipline. They’re tools, not a fix for a bad portfolio. Another common error is ignoring basis risk. A Treasury hedge may not perfectly offset a portfolio heavy in municipal or corporate spread products.

Advanced tactics should make the portfolio cleaner, not more fragile.

Tax coordination also matters. If broader wealth planning is part of the mandate, this overview of advanced tax strategies for high net worth individuals in 2026 is a useful complement because the best derivative decision is often the one that fits the investor’s tax and entity structure, and not solely the one with the cleanest market expression.

Building a Resilient Portfolio with Scenario Planning

Most bond plans fail because investors only prepare for the base case. They assume the Fed cuts, yields drift lower, and the portfolio behaves nicely. Real portfolios need to survive less convenient outcomes.

Three scenarios worth stress-testing

Start with the obvious one. The Fed cuts, cash yields decline, and intermediate bonds do what they’re supposed to do. In that case, the investor who extended thoughtfully is rewarded with steadier income and at least some price support.

Now test the less comfortable outcomes.

Inflation re-accelerates and the Fed pauses. In that environment, very long bonds can struggle, and investors who extended too aggressively may feel trapped. The defense is a moderate average duration, high-quality holdings, and enough scheduled liquidity that you’re not forced to sell.

Growth slows harder than expected and spreads widen. In such conditions, “high quality” stops being a slogan. Treasuries and stronger investment-grade holdings usually hold up better than lower-quality income trades. A client who reached for yield can discover quickly that extra spread income wasn’t worth the downside.

A risk-off shock pushes Treasury yields sharply lower. That’s the favorable surprise for duration, but it creates its own question. Do you harvest gains, or let the bonds run as insurance? The answer should be decided before the move, not during it.

Portfolio rules that improve decision-making

You don’t need dozens of triggers. A few clear rules go a long way.

- Set a liquidity floor: Keep enough near-term cash and short maturities for taxes, spending, and known commitments.

- Define your duration band: Don’t let short-term emotion push the portfolio from too short to too long.

- Separate income assets from tactical assets: Some holdings exist to fund cash flow. Others exist to express a rate view.

- Review after-tax results, not just pre-tax yield: Especially for large taxable accounts.

- Rebalance on process, not headlines: Markets move faster than investor psychology.

A disciplined framework belongs inside broader strategic financial planning, because the right bond allocation depends on retirement withdrawals, concentrated stock exposure, business liquidity, estate structures, and tax timing. Without that context, even a sound fixed-income idea can be implemented badly.

What resilience looks like for a HNW investor

Resilience isn’t owning the safest possible bond mix. It’s owning a mix you can hold through noise because it matches your cash needs, tax profile, and tolerance for mark-to-market movement.

That usually means:

- High-quality core holdings

- Intermediate rather than extreme duration

- Select use of municipal bonds where after-tax income matters

- Tactical tools only when they solve a real portfolio problem

- Written rules for what you’ll do if rates move the “wrong” way

The investor who wins this cycle probably won’t be the one who predicts every Fed move. It will be the one who locks in enough yield now, keeps credit standards high, and refuses to let short-term volatility derail a sensible plan.

If you’re evaluating how to lock in bond yields before 2026 rate cuts across taxable accounts, trusts, concentrated wealth, or family liquidity needs, Commons Capital can help you build a fixed-income strategy that balances yield, taxes, risk, and long-term planning.